LESSON 9-1

90 likes | 124 Vues

LESSON 9-1. Journalizing Purchases Using a Purchases Journal. MERCHANDISING BUSINESS. Def. – a business that purchases and sells goods - merchandise 2 types: Retail – a business that purchases and sells goods to consumers.

LESSON 9-1

E N D

Presentation Transcript

LESSON 9-1 Journalizing Purchases Using a Purchases Journal

MERCHANDISING BUSINESS • Def. – a business that purchases and sells goods - merchandise • 2 types: • Retail – a business that purchases and sells goods to consumers. • Wholesale – a business that buys and resells merchandise to retail businesses. • Recorded in a “special journal” – purchases journal • Has additional accts. on the financial statement for the purchase and sale of merchandise. 9-1

SPECIAL JOURNALS 5 Types: • Purchases - for all purchases of merchandise on acct. • Cash Payments – for all cash payments • Sales – for all sales of merchandise on acct. • Cash Receipts – for all cash receipts (received) • General Journal – for all OTHER transactions 9-1

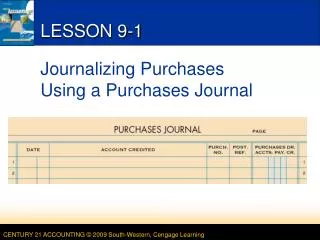

PURCHASING MERCHANDISE page 236 • Purchases account – Used to ONLY record the cost of merchandise. • Temporary cost account • Located in the merchandise division in the chart of accts. • Purchases are made from a vendor. • Markup – the amount added to the cost of merchandise to establish the selling price. 9-1

PURCHASES ON ACCOUNT page 236 • Purchase on Account – merchandise purchased to be paid for a later date. • AP is used to summarize amounts owed to all vendors. • Historical Cost – applied when the actual amount paid for merchandise or other items bought is recorded. 9-1

2 PURCHASE INVOICE page 238 1 4 3 1. Stamp the date received andpurchase invoice number. 3. Initials of the person whochecked the invoice. 2. Place a check mark by each amount. 4. Review the vendor’s terms. 9-1

PURCHASING MERCHANDISE ON ACCOUNT page 239 November 2. Purchased merchandise on account from Crown Distributing, $2,039.00. Purchase Invoice No. 83. 2 1 3 4 1. Write the date. 2. Write the vendor name. 3. Write the purchase invoice number. 4. Write the amount of the invoice. 9-1

1 6 TOTALING AND RULING A PURCHASES JOURNAL page 240 4 5 3 2 1. Rule a single line across the amount column. 4. Add the amount column. 5. Write the total. 2. Write the date. 6. Rule double lines across the amount column. 3. Write the word Total. 9-1

merchandise merchandising business retail merchandising business wholesale merchandising business special journal cost of merchandise markup vendor purchase on account purchases journal special amount column purchase invoice terms of sale TERMS REVIEW page 241 9-1