Download

1 / 8

80 likes | 93 Vues

If your business needs money fast, and you're not able to get an advance from your bank, you may be considering factoring. If that's the case, this article will help you understand what accounts receivable (or factoring) is, how it works and why it can be a valuable tool for your business.<br>

E N D

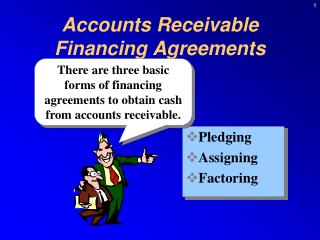

Accounts Receivable Financing: A Way to Boost Your Cash Flow

Introduction If your business needs money fast, and you're not able to get an advance from your bank, you may be considering factoring. If that's the case, this article will help you understand what accounts receivable (or factoring) is, how it works and why it can be a valuable tool for your business.

When to Use Accounts Receivable Financing If you are over-trading, if your cash flow has become an issue, or if customers are slow to pay their invoices then accounts receivable financing is an ideal solution. Accounts receivable financing can be used to provide short term working capital for any business.

How Accounts Receivable Financing Works Accounts receivable financing is a way to get cash for your business by selling your accounts receivable to a third-party lender. Essentially, the lender pays you immediately and then collects the money from your customers later. For example, let's say that you're an e-commerce merchant who sells $10 million worth of products per year. You've already collected half of this amount in advance through credit cards and PayPal, but now it's time to collect on the other half—but there's no way you can do that without some help. You're stuck with too many outstanding invoices at any given moment and not enough cash flow in hand!

What Are the Costs of Factoring? The cost of factoring depends on a number of variables, including the size of your business and the amount of time you need to pay off your debt. If you're looking for an account receivable financing provider that will provide you with more than one option, there are plenty out there. Here's how it works: • The factoring company pays for all or part of your invoices in return for receiving payment from those invoices from customers within a certain period, usually 30 days or less. This allows businesses to get cash quickly while still being able to make a profit by collecting interest on their accounts receivable as well as fees charged by the factoring company itself. For example: You sell $100 worth of widgets at $10 each; let’s say that half-a-year later (60 days), one customer paid off all his purchases ($40) plus interest ($2). That means his total purchase price was $42 but he only paid $40 because he bought these items 60 days ago! * What does this mean? It means that companies who use this financing method can actually receive money from customers before they even know they have made any sales—and then pay back those same customers over time so that everyone wins!

Learn about accounts receivable (or factoring) as a tool for spanning a cash crunch. Accounts receivable financing is a tool for businesses that are in need of cash flow. A business uses this type of financing by selling its accounts receivable to a third-party company—that is, it sells its invoices to the factor. The factor buys these invoices and then collects them from the customer on behalf of your business. In exchange for doing so, the factor charges you interest on those invoices until they are paid off (or until you settle up with them). Here's how it works: • The first step is to find out if factoring is right for your company. Some businesses don't qualify because they operate in industries that don't generate enough receivables or have too many bad debts (uncollectible bills). You can determine if this type of financing makes sense by asking yourself three questions: Are my customers paying on time? Do I have a consistent amount each month? Is there an industry trend toward faster payment processing? If yes to these questions, then accounts receivable financing may work well for your business.

Conclusion If you’re in the process of finding a factoring company, we hope that this post has helped you better understand the process. If you are looking for more information on accounts receivable financing or need help with your cash flow crunch, contact us today!