Download

1 / 25

250 likes | 274 Vues

Explore the comprehensive overview of the US tax system, key reforms in 2018, and implications for taxpayers, real estate professionals, homeowners, and investors. Unveil insights on types of taxpayers, taxes, rates, deductions, and credits in the updated tax framework.

E N D

The Tax Cuts and Jobs ActPresented to Birmingham Association of Realtors James W. Moody, CPA April 8, 2019

The Goals • Overview of the US tax system • What are the main areas of reform in 2018 • What does tax reform mean for: • Individual and Business taxpayers • Real Estate Professionals • Homeowners (and renters) • Investors in real estate • Rental Real Estate

Overview of U.S. Tax System • Types of Taxpayers • Individuals • Pass Through Entities • S Corporation • Partnership (LLC, LLP, LP, etc.) • Corporations • Trusts and Estates

Overview of U.S. Tax System • Types of Taxes • Income tax • Payroll tax (SS, Medicare, Self Employment) • Property tax - ad valorem • Estate and gift • Excise tax • Sales and Use tax • Franchise Tax • Permits and licenses • But wait, there’s more…

Overview of U.S. Tax System • Rate Terminology • Marginal Rate • the rate your next dollar of income will be taxed at • Average Rate – Or Blended Rate • Total tax divided by total income • A Credit is Better than a Deduction! • A deduction reduces your taxable income. A $1,000 deduction reduces tax by $150 if the marginal tax rate is 15% • A credit reduces your tax. A $1,000 credit reduces your tax by $1,000.

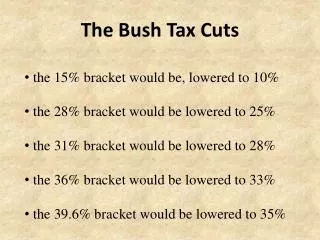

2018 Tax Reform • Individual Income Tax Provisions • Adjusted Tax Rates and Brackets • Generally lower than 2017 • 7 Tax Brackets ranging from 10% to 37% • 2017 – 10 – 15 – 25 – 28 – 33 – 35 – 39.6 • 2018 – 10 – 12 – 22 – 24 – 32 – 35 – 37 • Top 37% bracket applies to taxable income over $600,000 (Married) and $500,000 (single) • Favorable tax rate for capital gains retained • 0%, 15%, 20%

2018 Tax Reform • Individual Income Tax Provisions - Continued • Itemized Deductions • State and local income and property taxes limited to $10,000 • Mortgage Interest limited to $750,000 principal – new loans • Home Equity loans may still be deductible (it depends) • Medical Expenses allowed limited to 7.5% of AGI • Charitable Donations allowed up to 60% of AGI • Employee unreimbursed job expenses eliminated • certain investment expenses eliminated • Phaseout of itemized deductions eliminated

2018 Tax Reform • Individual Income Tax Provisions - Continued • Standard Deduction Increased – essentially doubled • Single - $6,350 to $12,000 • Married filing joint - $12,700 to $24,000 • Personal Exemptions eliminated • Previously +/- $4,000 extra deduction per family member • Child Tax Credit doubled and expanded • Increases from $1,000 to $2,000 per child (under 16) • Income phaseout increased significantly so more taxpayers will benefit from the credit ($200,000/$400,000) • Up to $1,400 is refundable for some filers • A new $500 Credit for dependents over 16

2018 Tax Reform • Individual Income Tax Provisions - Continued • Other Retained Provisions: • Exclusion of Gain on Sale of Residence • Self Employment Tax • Alternative Minimum Tax, but fewer will pay • Student Loan Interest deduction • Other Repealed Provisions: • Individual health insurance mandate • Moving expense deduction • Casualty loss deduction (except federally declared disasters) • Alimony deduction (for divorces after 1/1/2019)

2018 Tax Reform • Individual Estate and Gift Provisions • Lifetime Exemption Amount Doubled • From $5.49 Million in 2017 to 11.2 Million in 2018 • This is $22.4 Million per couple • Tax rate is 40% on gifts/estate transfers over limits • Limits apply to gift, estate, and GST. • These increased limits expire after 2025 • This will significantly reduce the number of taxable estates for the next 7 years • The annual gift exclusion is $15,000 in 2018 and 2019 • Gift and estate tax returns should still be filed if required

2018 Tax Reform • Business Tax Provisions – All Businesses • Accelerated Depreciation Expanded • 100% Bonus Depreciation for eligible purchases • 100% First Year Expensing under Section 179 also increased and expanded • Entertainment Expenses not deductible • Business Interest expense limited based on income • Net Operating Losses • Carry forward only, no expiration. • NOL deduction limited to 80% of taxable income.

2018 Tax Reform • Business Tax Provisions – All Businesses • Special Small Business Provisions • Businesses under $25 million benefit from a few special provisions • Interest expense not limited • Cash basis tax reporting • Uniform Capitalization Rules

2018 Tax Reform • Business Tax Provisions – C Corporations • C Corporation Tax Rates reduced to a flat 21% • Previous a graduated rate ranging from 15% to 39% • C Corporations are still subject to “double taxation” • Dividends are taxable to owner when received • Effective Tax Rate for C Corporations to earn a profit and distribute to the owners will still likely exceed 40% and in some cases, exceed 50%, depending on state tax rates. • Corporate AMT Repealed

2018 Tax Reform • Business Tax Provisions – Pass Through Entities • Proprietorships, Partnerships, and S Corporations • Income still “passes through” to their owners • New 20% deduction for “Qualified Business Income” or “QBI” • This is potentially the largest area of tax savings for many small business owners or self-employed individuals, but the most complicated to understand and apply.

2018 Tax Reform • 20% QBI Deduction • Applies to Proprietors, Partnership, and S Corp owners • What is QBI? • taxable income of the partnership, S corp, or proprietorship. • Wages or guaranteed payments are not eligible for deduction • If taxable income is less than $315,000 (MFJ) or $157,500 (single), eligible for 20% deduction. • If taxable income exceeds $315,000 (MFJ) or $157,500 (single) the 20% deduction may be limited or eliminated based on: • The nature of the business (professional service) • The amount of W2 wages • The amount of fixed assets • The amount of taxable income

2018 Tax Reform • 20% QBI Deduction - Continued • Certain professionals are completely excluded from this deduction, unless taxable income is below thresholds • Accountants, attorneys, doctors, consultants, financial services, and others where the main asset of the business is the skill or reputation of one or more of its employees or owners • Maximum deduction is 20% of QBI. • The deduction may be phased out if AGI is between $315,000 and $415,000 (MFJ) or $157,500 and $207,500 (single). See factors on previous slide.

2018 Tax Reform • 20% QBI Deduction - Continued • A 20% deduction for business income is like reducing the tax rate on that income by 20% (or more) • The 37% tax rate would be reduced to 29.6%. • Compare to the 39.6% highest bracket in 2017 • If QBI is $100,000, the QBI deduction would be $20,000, making only $80,000 subject to tax. • QBI deduction could be reduced if taxable income is smaller than the QBI amount of $100,000

2018 Tax Reform • Real Estate Professionals • Are Realtors considered “personal service businesses”? Like lawyers,doctors and stock brokers? • Recently finalized Regulations clarify “No” • This is a huge win for Realtors • Self-Employed Realtors filing Schedule C (proprietor) • If taxable income below thresholds ($315,000/$157,500), Schedule C income eligible for 20% deduction • If taxable income exceeds thresholds ($315,000/$157,500), may still be eligible for the 20% deduction, but other factors apply • Deduction applies to income tax only (not SE Tax)

2018 Tax Reform • Real Estate Professionals • Partners or S Corp Shareholders also eligible for QBI deduction – same as proprietors • Salaries not eligible for 20% deduction • W-2 Employees • No special QBI deduction or special provisions • Unreimbursed expenses or mileage are no longer deductible as an itemized deduction • See Examples 1 to 5 on pages 12 -18 of NAR Publication

2018 Tax Reform • Homeowners • The standard deduction was increased significantly, so many taxpayers will no longer itemize (Federal). • Property taxes and interest are still itemized deductions, but those deductions provide no tax savings for taxpayers claiming a standard deduction. • There is no tax savings between renting and buying if the taxpayer claims a standard deduction. • Reminder: Reform is for Federal Tax only. Alabama standard deduction is still very low, so there may still be tax savings in Alabama.

2018 Tax Reform • Homeowners • If state income taxes exceed $10,000, the property taxes will not be counted toward itemized deductions due to the $10,000 limitation. • Taxpayers with AL taxable income over $200,000 • If itemized deductions exceed $24,000 (MFJ) or $12,000 single, the benefits of home ownership and mortgages will still exist. • State income and property taxes (no more than $10,000) • Mortgage interest ($750,000 principal) • Charitable Donations

2018 Tax Reform • Homeowners • While there may be less tax incentives to purchase a home, especially for lower or median-income taxpayers, reduced tax rates and increased child tax credits may put more money in the pockets of taxpayers. • Exclusion of gain on sale of residence still applies • See Appendix 2 of NAR Publication

2018 Tax Reform • Investors • 1031 Like-Kind Exchanges • Still allowed, but for real property only • Not allowed for personal property, such as equipment, automobiles, etc.

2018 Tax Reform • Rental Real Estate • Income from owning and renting real estate to others may (or may not) be eligible for the 20% QBI deduction • The facts and circumstances will determine whether the activity is considered trade or business income • A triple net lease, for example, may be considered an investment, rather than a trade or business • The time commitment of the owner, or their employees or agents, is another factor

James W. Moody, CPAjmoody@dentmoses.com(205) 380-19122204 Lakeshore Drive, Suite 300Birmingham, Alabama 35209