IAB PwC ONLINE ADSPEND STUDY 2010

320 likes | 479 Vues

IAB PwC ONLINE ADSPEND STUDY 2010. Suzanne McElligott Chief Executive, IAB Ireland April 13th, 2010. In association with PwC. Agenda. Introduction Study Methodology Market Background Online Adspend Results Looking ahead… Questions. 1. INTRODUCTION. Introduction.

IAB PwC ONLINE ADSPEND STUDY 2010

E N D

Presentation Transcript

IAB PwC ONLINE ADSPEND STUDY 2010 Suzanne McElligott Chief Executive, IAB Ireland April 13th, 2010 In association with PwC

Agenda Introduction Study Methodology Market Background Online Adspend Results Looking ahead… Questions

Introduction • Census of all major Irish online media owners • Information collected each half year • Analysis available by • Format • Industry category

IAB Ireland Prove Promote Protect

2. STUDY METHODOLOGY • Internationally, IAB has been working with PwC since 1997 to survey the value of online adspend in Europe and North America. • In our study, 26 participated, representing multiple websites. • Sales houses and advertising networks also participated • All data was provided to PwC on a confidential basis

Survey Participants *estimates prepared, not participants

STUDY CONTENT • Total advertising revenue is reported on a gross actual basis (including agency commission) • The figures are drawn up on the basis of actual revenues submitted by the study participants • Google or Facebook do not break out their earnings from Irish advertisers. PwC created an independent estimate by extrapolating from spend data provided directly by a representative sample of their clients.

3. MARKET BACKGROUND GDP FELL 1% IN 2010 COMPARED TO 2009 GNP FELL 2.1% IN 2010 COMPARED TO 2009 Source: CSO: Quarterly National Accounts Quarter 4 2010

INCREASED BROADBAND CONNECTION Broadband • Fixed Broadband connections increased from 1,411,450 in 2009 to 1,591,803 in 2010 • (+ 12.8%) • Mobile Broadband increased from 449,792 in 2009 to 571,839 in 2010 (+27.2%) • Total Broadband connections increased from 1,861,242 in 2009 to 2,163,642 in 2010 (+16.2%) Source: ComReg’s Trend Unit, Comstat.ie, Broadband

MORE TIME ONLINE 2009:13.2 Average Hours per week 2010:19.1 Average Hours per week Source: ComReg 2009 : Red C Digital Trends Study

4. IAB IRELAND PwC ONLINE ADSPEND 2010 GROSS ONLINE ADSPEND: € 110 M

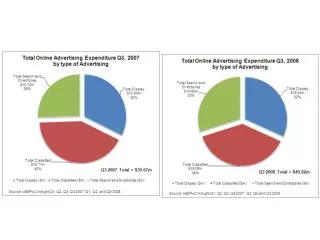

Online Revenue: 2010 vs. 2009 +13.5% 2010: €110 M 2009: €97 M Million €

PwC Irish E&M Industry Outlook 2010: $4.59 billion (+.3%) 12.2% - 5.9% - 11.1% - 8.9% - 4.1% - 5.4% 11.2% 3.1% - 7.5% 0.7% 9.0% - 5.8% - 0.7% - 2.6% Slide 19

Digital Media Mix 2010 Breakdown by advertising format based on figures* provided *Based on 95.9% of the market

Digital Media Mix 2009 Breakdown by advertising format based on figures* provided *Based on 94.2% of the market

INDUSTRY CATEGORIES 2010 Top performers : • Automobile (22%) • Recruitment/Property (19%) Top performers : • Automobile (21%) • Recruitment/Property (17%)

INDUSTRY CATEGORIES 2009 Top performers : • Recruitment/Property (25%) • Automobile (20%) Top performers : • Automobile (22%) • Recruitment/Property (19%)

2010 Breakdown by Industry Category – incl. Auto and Recruitment/Property Based on 74.6% of the market

2010 Breakdown by Industry Category – excl. Auto and Recruitment/Property Based on 74.6% of the market

LOOKING AHEAD Irish online adspend is predicted to grow by 11% in 2011 (Carat ) Smart phone penetration to grow to 55% of online users in 2012 (Red C Digital Trends Study) 78% of respondents predict growth or strong growth in the next 6 months

Awareness of respondents of the forthcoming ePrivacy regulations

Next IAB PwC Study: H1 2011 October 2011

OUR THANKS TO • All our participants • Bartley O’Connor, Nuala Nic Ghearailt, Sally O’Brien • Johanna Dehaene and Claire Carson, PwC

6. QUESTIONS • For Further information: • info@iabireland.ie