Forester Value Fund February 2012 Report

10 likes | 94 Vues

Gain insights into the Forester Value fund's February performance compared to S&P 500 & Russell Large Cap Value index. Understand the attribution for underperformance, top & bottom stock contributors, impact of central banks' actions, rationale for hedge reduction, and portfolio composition details. Get essential information about the fund's strategies and positioning.

Forester Value Fund February 2012 Report

E N D

Presentation Transcript

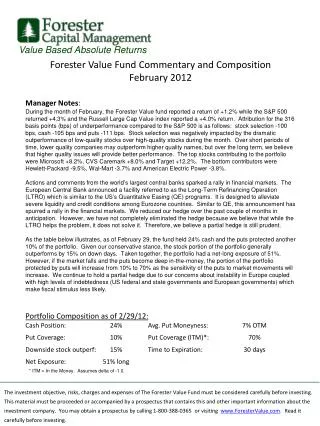

Value Based Absolute Returns Manager Notes: During the month of February, the Forester Value fund reported a return of +1.2% while the S&P 500 returned +4.3% and the Russell Large Cap Value index reported a +4.0% return. Attribution for the 316 basis points (bps) of underperformance compared to the S&P 500 is as follows: stock selection -100 bps, cash -105 bps and puts -111 bps. Stock selection was negatively impacted by the dramatic outperformance of low-quality stocks over high-quality stocks during the month. Over short periods of time, lower quality companies may outperform higher quality names, but over the long term, we believe that higher quality issues will provide better performance. The top stocks contributing to the portfolio were Microsoft +8.2%, CVS Caremark +8.0% and Target +12.2%. The bottom contributors were Hewlett-Packard -9.5%, Wal-Mart -3.7% and American Electric Power -3.8%. Actions and comments from the world’s largest central banks sparked a rally in financial markets. The European Central Bank announced a facility referred to as the Long-Term Refinancing Operation (LTRO) which is similar to the US’s Quantitative Easing (QE) programs. It is designed to alleviate severe liquidity and credit conditions among Eurozone countries. Similar to QE, this announcement has spurred a rally in the financial markets. We reduced our hedge over the past couple of months in anticipation. However, we have not completely eliminated the hedge because we believe that while the LTRO helps the problem, it does not solve it. Therefore, we believe a partial hedge is still prudent. As the table below illustrates, as of February 29, the fund held 24% cash and the puts protected another 10% of the portfolio. Given our conservative stance, the stock portion of the portfolio generally outperforms by 15% on down days. Taken together, the portfolio had a net-long exposure of 51%. However, if the market falls and the puts become deep in-the-money, the portion of the portfolio protected by puts will increase from 10% to 70% as the sensitivity of the puts to market movements will increase. We continue to hold a partial hedge due to our concerns about instability in Europe coupled with high levels of indebtedness (US federal and state governments and European governments) which make fiscal stimulus less likely. Forester Value Fund Commentary and CompositionFebruary 2012 Portfolio Composition as of 2/29/12: Cash Position: 24% Avg. Put Moneyness: 7% OTM Put Coverage: 10% Put Coverage (ITM)*: 70% Downside stock outperf: 15% Time to Expiration: 30 days Net Exposure: 51% long * ITM = In the Money. Assumes delta of -1.0. The investment objective, risks, charges and expenses of The Forester Value Fund must be considered carefully before investing. This material must be proceeded or accompanied by a prospectus that contains this and other important information about the investment company. You may obtain a prospectus by calling 1-800-388-0365 or visiting www.ForesterValue.com. Read it carefully before investing.