Taxable Income

Taxable Income. Here we study some details about how to calculate the income tax we actually owe. With passage of the Tax Reform Act of 1986 income was given classification names. We have 3 types – active income, portfolio income and passive income. Active income is income earned on the job.

Taxable Income

E N D

Presentation Transcript

Taxable Income Here we study some details about how to calculate the income tax we actually owe.

With passage of the Tax Reform Act of 1986 income was given classification names. We have 3 types – active income, portfolio income and passive income. Active income is income earned on the job. Portfolio income is income earned from investments. Passive income is income earned from tax shelters such as real estate and limited partnerships - a special form of business organization. On the portfolio income we have interest and dividends and capital gains. Capital gains have been treated differently in the past and still are, to a certain extent, today.

On an asset, if price we sell asset minus price we bought asset > 0, then we have experienced a capital gain. The current tax code says if the assets was held for less than 12 months, then capital gains will be taxed like other income. If the asset was held for more than 12 months, then the rate is lower than the marginal rate of the individual involved – exhibit 3.3 page 97 shows the rates.

Digress - FICA, Federal Insurance Contributions Act, is the technical term for the taxes we pay for social security and medicare. Let’s look at this from the point of view of the employer. When the employer pays the employee $1 in wages the employer must also pay .062 cents in social security and .0145 cents in medicare. The social security part ends after the employer pays out $76,200(this value is indexed to inflation) to an employee in a year, while the medicare part continues to be paid on all $’s. Now, when we look at the point of view of the employee, on each $1 earned the employee pays .0625 cents in social security and .0145 cents in medicare. If an individual is self employed, the individual pays both the employee part and the employer part as described above. Plus, the employer part is tax deductible.

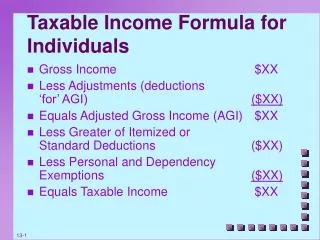

Gross income = active income + portfolio income + passive income. Adjusted gross income = gross income - general deductions like the ones listed on page 98 toward the top. The adjusted gross income is the initial basis for taxation. But before calculating the tax, personal deductions and exemptions may also be subtracted out. Deductions may either be itemized (when a specific tax-deductible personal expense has taken place) or standard ( a blanket fixed amount). Note that itemized deductions are often tied to the adjusted gross income figure. For example, medical and dental expenses in excess of 7.5% of AGI may be deducted.

Exemptions are subtractions from AGI based on the number of people supported by the taxpayer’s income. In the year 2003, the exemption was worth $3,050 per person (the value is indexed to the inflation rate). Taxable income = AGI - deductions - exemptions. To find the tax, we saw before you would take the taxable income and work it through the brackets. The government actually has bigger tables that do a lot of the calculating for you. Remember that you take the part of your income in each bracket and multiply by the rate in each bracket and then add across brackets. This would give you the tax liability. BUT, there is one more way to have the tax liability reduced - the tax credit.

A tax credit is a deduction from the tax liability. Page 104 has a list of some common credits. Which would you rather have, a dollar in exemptions or credits? To see the answer let’s use a simple example designed to help us see the answer although we will abstract from reality a little. Say taxable income is $100. The tax is then $10 (10% bracket). Now say an additional exemption of $1 occurs. The tax is then 99(.10) = 9.90. Notice the $1 exemption only reduced the tax owed by 10 cents. Instead of an exemption, say a $1 tax credit was obtained. The tax is then reduced to $9 (100(.1) – 1)). Credits reduce the tax owed dollar for dollar, while exemptions and deductions only reduce taxes by the marginal tax rate. Go with the credits.