Wealth Tax

Wealth Tax. Theory, tax planning and Sum. Steps. Chargeability. Individual, HUF and Company at 1% of the amount by which net wealth exceeds Rs 15 lacs. No wealth tax is chargeable to Co.’s Registered u/s 25 of Companies Act,1956 (Promoting commerce, art, science etc.

Wealth Tax

E N D

Presentation Transcript

Wealth Tax Theory, tax planning and Sum

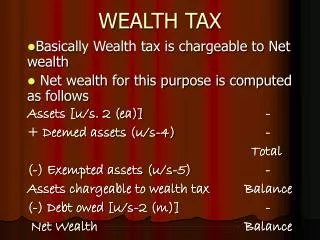

Chargeability • Individual, HUF and Company at 1% of the amount by which net wealth exceeds Rs 15 lacs. • No wealth tax is chargeable to • Co.’s Registered u/s 25 of Companies Act,1956 (Promoting commerce, art, science etc. • Co-operative society, social club, political party • Mutual fund specified u/s 10(23D) of The IT Act.

Terminologies • Assessment Year: 12 months immediately after the valuation date. • Net wealth It is access of assets over debts. Assets include deemed assets but not exempt assets.

Incidence of tax x= all assets located in india, including deemed assets. y= debts in relation to x p= All assets located out of india including deemed assets, q= debts in relation to p

Assets (sec 2 (ea)) • Guests House, residential house or commercial building (i) • Any building or land whether used for commercial or residential purpose or for the purpose of guest house. • A farm house situated within 25 Kms from local limits of any municipality or a cantonment board. When a house/residential house/ farm house is not treated as “Assets” • Exceptions • Exception 1 • Residential purpose. • Alloted to employee or officer or a director who is whole time employment and his gross dalary is less than 5 lacs • Exception 2 • House as stock in trade

Exception 3 • A house used for own business or profession. • Exception 4 • A let out property for a period of atleast 300 days • Exception 5 • A commercial complex. • Motor cars (ii) Except the following two, any other motor car is an asset. • Motor car used by the assessee in the business of running them on hire or • Motor cars treated as stock in trade

Jewellery, bullion, utensils of gold, silver etc (iii) • Meaning • Ornaments made of gold, silver, platinum or any other precious metal or any alloy containing one or more of such precious metals, whether sewn into wearing apparel or not. • Precious or semi precious stones whether or not set in any furniture, utensils or other or worked or… • Exceptions • Stock in trade • Gold deposit bonds • Yachts, boats and aircrafts (vi) Other than those used by the assessee for commercial purpose are treated as “assets”

Urban land (v). Land means land situated in the following area. a) Within the jurisdiction of municipality, and which has a population of not less than 10000 according to the preceding census of which relevant figures have been published before the valuation date. Or b) In any area within such a distance ( not being more than 8 kms) from the local limits of any municipality

Cash in hand (vi) • The following is treated as “assets”

DEEMED ASSETS Sec. 4) • Assets transferred by one spouse to another (Sec 4(I)(a)(1)) • Conditions. • Asset is transferred by an individual after 31-3-1956 • The assets transferred to his or her spouse. • The transfer may be direct or indirect. • The asset is transferred other than adequate consideration or in connection with an agreement to live apart. • The asset may be with the transferee in the same form as it was transferred as on valuation date. • Other points • Not applicable to HUF, if the transfer is in favour of one of its members. • Adequate consideration cannot be equated to sufficient or good or valid consideration. • Spouse means lawfully wedded person only.

Assets held by minor child (Sec 4(I)(a)(ii)) • Conditions • The net wealth should be clubbed with that parent whose net wealth is greater. • Those assets which are acquired by the minor either on account of any manual work done by him or by his skill, talent or specialised knowledge are not clubbed. • Such clubbing is not applicable if the child is no longer minor. • When the asset is clubbed with one parent’s wealth of the minor ,such asset shall not be included in other parent’s health in any succeeding years, untill and unless the Assessing officer is satisfied that it is necessary to do so.

Assets transferred to a person or an association of person (sec 4(1)(a)(iii)) • Assets transferred under revocable transfers (sec 4(1)(a)(iv)) • Assets transferred to son’s wife (sec 4(1)(a)(v))

Assets exempt from tax (sec 5) • Property held under a trust. • Coparceners interest in a HUF. • Residential building of a former ruler. • Former ruler’s jewellery. (recognized as heir loom by central govt before 1-4-1957 or by the board after that.) • One house or a part of house for an individual or huf

Debt owned From the aggregrate of all assets including deemed assets but not exempt assets, the debts owned by assesse are to be subtracted, subjec tto following conditions • Only debt owned by the assessee on the valuation date are deductible. • Debt should have been incurred in relation to those

Valuation of assets • Valuation of building [part B of schedule III] with effect from the assessement year 1989-1990. • Step I • Find out gross maintainable rent • Step II • Find out net maintainable rent(gross – municipal taxes and 15% of gross maintainable rent)

Step III • Capitalise net maintainable rent It can be done by * the net maintainable rent with 12.5 if property is constructed on leasehold land, * by 10, subject to unexpired lease term is 50 years or more. (* by 8 in case it is less than 50 years) • Properties acquired/ constructed after 31-3-1974 • Find out the value of house property as above. • Find out the original cost plus cost of improvement of the house property • Decision: the higher of above is taken as capitalised.

Exceptions The rule is not applicable if the following conditions are satisfied. • Only one house property is exempted. • The HP is used for residential purpose throughout the year and acquired/constructed after March 31, 1974. • The cost of acquisition/construction plus cost of improvement does not exceeds Rs 50 lakhs, if it is situated at metros and 25 lakhs at any other place.

Fourth Step Add premium Fourth step is to add a premium to the capitalised value determined under the third step if the un built area of the land on which the property is built exceeds the specified area. Aggregate area: it refers to the aggregate area on which the property is built as well as the unbuilt area. Unbuilt area: refers to that part of aggregate area on which no building has been erected.

Specified area. • When the property is situated at metros, 60 % of the aggregate area. • When property is situated at selected areas like Agra, Ahmedabad, Surat, Vadodara etc (total 26 cities), 65 % • Any other place 70 %.

Fifth step: Deduct unearned increment The fifth step is to deduct the amount of unearned increment payable. If the case of property built on leasehold land any part of the unearned increase in value is payable to the government or any authority at the time of transfer of the property, the value of such property, as determined above will be reduced by the amount liable to be so paid if the property had been trransferred on the valuation date or 50 % of the value of the property so determined, whichever is less.

Sum no.1 • For the assessment yr. 2008-09, X shows valuation date is 31-3-2008 submits the following particulars of the assets and liabilities. Determine his wealth tax liability on the assumption that a) X is an Indian national and resident and ordinarily resident in India. b) X is an Indian national but not ordinarily resident in India. c) X is a foreign national and non resident in India.

2. X furnishes the following particulars for the compilation of his wealth tax return for the assessment year2008-09 a) Gifts of jewellery made to wife from time to time aggregrating Rs 60,000 market value on valuation date 2,00,000. b) Flat purchased under installment payment scheme in 1972 for Rs 7,50,000 used for purposes of his residence and market value as on 31-3-2008 (installment unpaid 50000) 10,00,000 c) Urban land transferred to minor handicapped child valued on 31-3-2008 5,00,000 Explain how you will deal with these items.

3. X ltd is a company on business in the construction and sale of residential flats. It furnishes the following data and requests you to compile wealth tax returns ad determine the tax payable for assessement year 2008-09

The company has taken a loan of Rs 6,00,000, Rs. 7,00,000, Rs 50,000 and Rs 90,000 for acquiring property numbers 5,6,12 and 13 respectively. Find out the wealth tax liability of the company for the assessement year 2008-09.

![get [PDF] Download Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your](https://cdn7.slideserve.com/12480556/slide1-dt.jpg)