Download

1 / 44

440 likes | 554 Vues

Essential Risk-Based Capital Concepts and the (Not So New) Basel II Accord. FCA FAST rack Capital Workshop June 15, 2006 Bruce J. Sherrick Section C2. ● iFAR ● integrated F inancial A nalytics and R esearch, LLP. Some Quotes….

E N D

Essential Risk-Based Capital Concepts and the (Not So New) Basel II Accord FCA FASTrack Capital Workshop June 15, 2006 Bruce J. Sherrick Section C2 ●iFAR ● integrated Financial Analytics and Research, LLP

Some Quotes….. • “The proposed new Basel II Accord is now described and amended on over 750 pages of text, and the word ‘agriculture’ does not appear once.” (Peter Barry’s observation at the Capitalizing for Risk in AgricultureSymposium, subsequently revised upward) • “The impact and consequences of Basel II will be immense for financial institutions. New processes and procedures need to be implemented, and there is a tremendous need for new data management…. data issues are enormously complex requiring (long histories) and external validation” (Susan Andre)

Some More Quotes….. • “Basel I aged quickly and not gracefully” John Hawke, Comptroller of the Currency, 2002 • “… these proposals on Basel II and the amended Basel I represent substantial revisions to the regulatory risk-based capital rules applied to U.S. banking institutions, from the very largest to the smallest” Governor Susan Schmidt Bies, 2006 • “Far better an approximate answer to the right question than an exact answer to the wrong one – the latter of which may be made arbitrarily precise via a redefinition of the question”(various attributions including Sherlock Holmes)

Does Basel II ask the right questions? • Introduction to Economic Capital • Basel-II’s Role in encouraging the “right amount” of economic (rather than regulatory minimum) capital • Basel II and the FCS • Some Strategic Implications

Views of “Capital” differ: • Owners see as synonymous to wealth: • Growth in value • Current Return (income) • Riskiness of growth and return stream • Financial Officers (CFO, Treasurer…): • Funding source and capacity for growth • Constraint • Regulators: • Safety and soundness: Historic View that Too Much is Never Enough • Basel II – Economic Capital Aligned for Efficiency …Economic Capital

Risk Emphasis: Hold Economic Capital to Cover • Future losses • Expected: loss allowance • Unexpected: equity • Arising from • Credit risk: borrower’s default • Market risk: effects of interest rate changes on asset and liability values • Operational risk: failed human, performance, processes and technology …Economic Capital

Economic Capital Needs Credit Risk MarketRisk Operational Risk Economic Capital …Economic Capital

Loss Attributes • Frequency: Probability of default (PD) • Severity: Loss given default (LGD) • Amount: Exposure at default (EAD) N.B.: Separation of PD from LGD is a KEY distinction from typical risk-rating practices in current practice. …Economic Capital

What is Economic Capital ? Various views including: • Amount needed to “insure” against undesirable outcome with given tolerance • Guided by actuarial principles and market pricing of ROE risk • Backstop for risk and growth • Includes equity capital and loss reserves …Economic Capital

Who is this “Basel” anyhow.. • Basel Committee on Bank Supervision • Committee of central banks and regulators from major industrialized countries • Headquartered in Basel, Switzerland • Hosted by the Bank for International Settlements (www.bis.org)

What Does Basel Do? • Provides broad policy guidelines for each country’s regulators to adopt or modify • Forum for Industry interaction • Extensive staff and research program • Fosters international monetary and financial cooperation and serves as a bank for central banks.

1988 Basel Accord (Basel I) • Targeted at large, international banks • Adopted by over 100 countries; applied to all U.S. banks and other financial institutions, including the FCS • Slots loans and securities into four risk classes (e.g. all commercial and agricultural loans treated the same) • The de facto standard. Period.

Advantages Simplicity Uniformity Capital refinement New measures and models Disadvantages Simplicity Crude risk classes Not responsive to innovation Ignores diversification Largely ignores passage of time and risk mitigation Basel I (1988 cited as 1st adoption)

Background – Basel I to present • Basel Accord of 1988 aimed to homogenize (capital and other) practices of internationally active banks, beginning with those in the G-10 countries. • Formally in place now in >100 countries, de facto standard for nearly all. • Represents a Minimum Hurdle view of capital • e.g., 8% with standard weights, non-responsive to changes in non-categoric risks • “The purpose of requiring banks to hold capital is to prevent 1-sided bets.” – K. Rogoff, Journal of Economic Perspectives, 1999 special issue on international bank regulation. • Viewed as deductible applied against implied public backstop for financial institutions.

Background – continued Asymmetry…. • Cost of excess capital not borne by public regulator • Cost of too little capital is borne by taxpayer Leads to….. • Rational intent to set capital requirements with high likelihood for adequacy = low tolerance for insolvency risk

Basel II – the main idea • Basel II consultative (early warning) document in 1999 with indications that new proposal would represent a move toward “economic” capital and more market pricing of risk. • January 2001 “package” reflecting comments on proposals and indicating additional details on risk classes, rating and so forth. First attempt at timeline for implementation – since delayed formally at least 5 times. • Outlines 3-pillar approach • minimum capital calculations • explicit and more homogenized role of supervisory review • reliance on increased market discipline through increased disclosure requirements.

Basel II - continued • Early 2002 began development and distribution of QIS materials – intent to assess the implications for aggregate and specific capital under new guidelines. Current version is QIS5 template. • Some important information about use of QIS results: • calibration during phase-in • same total capital in system (more later about this point…) • incentive to use more risk-sensitive internal ratings systems • working example: loan asset with .7% probability of default and 50% LGD and 3 year maturity would require 8% capital.

Basel II - continued • Interest rate risk moved toward “operational risk” and treated in pillar 2. • Sophistication in funding can transform interest rate risk to counter party credit risk (W. Staats). • Increased granularity – more finely disaggregated risk categories in principle leads to better risk-pricing opportunities – has been bane to FCS Banks – conflict with existing bond rating categories and Rating Agency tables. • Requires formal evaluation of PD, EAD, LGD, and some measures of “relatedness” (correlation).

Basel II – Major issues for Ag involve credit and operational risk adapted from PWC and BIS

Credit Risk Options – the pecking order • Standardized approach • Similar in concept to BASEL I with a few additional risk ranges and weights. • Foundation IRB • Broad categorizations required (no choice); institution assigns ratings linked to PD calculations. Other inputs set by supervisor/regulator • Advanced IRB • In addition to PD calculations, institution uses model-based estimates of LGD and EAD, subject to regulatory approval. • FCS Institutions are planning to be FIRB and AIRB – some are getting pretty good infrastructure…..

The Basel II Proposed Accord • Basel’s Role: To Standardize Economic Capital and encourage Efficient Deployment of Capital. • Allow Market Price of Risk to be determined • Respond to changes in risk through time • Simplify and Homogenize Safety and Soundness practices Basel-II’s Role..

Basel II • Basel II is both following and leading • Following “best practices” of the top tier of banks world wide • Major developments in management, measurement, and modeling • Leading/stimulating wider adoption and tailoring to institutional size and complexity

Basel II Process • First draft - 1999 • 35 pages • Too simple • Second draft - 2001 • 500 + pages • Too complicated; trades off complexity and refinement • First “Final” version - 2003 • Scaled back with calibration for phase in • Implementation: end of 2006 or later • 2nd through 5th Final Versions include QIS studies and templates for “parallel” calculations and “calibration” factors.

Basel II – Current Timeline QIS 3 Calibration Begin Parallel running Phase in and begin enforcement voluntarily Prep for Basel III…. G-10 approvals Begin phase in (e.o.y) 2003 2004 2005 2007 Beyond 2009 – 95% floor 2006 2009 2005 - prelim 2010 – 90% floor 2007 2011 2011 – 85% floor 2006 - final 2008

Three Pillars • Minimum capital requirements (our focus) • Supervisory review • More intense as an institution uses its internal systems to measure risk • Goal attainment and management quality • Market discipline • Increased disclosure and market discipline

General Characteristics • Accord contains a spectrum of approaches • Institutions can choose the appropriate approach, subject to documentation and approval • Incentives (lower capital) are provided for better risk management

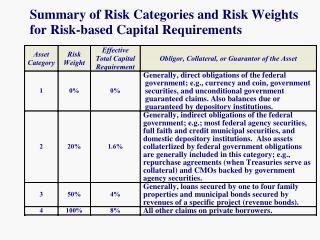

Minimum Capital Requirements for Credit Risk – 3 approaches 1. Standardized Approach • Similar to existing capital regulations • More risk weighting categories for commercial loans (0%, 50%, 100%, 125%, 150%) • Mapped to external credit ratings or not rated • Applicable to “community banks” or those approved by regulator

2. Internal-Ratings Based Foundation Approach: • Commercial loans • Institution estimates the probability of default (PD) for at least eight risk classes and five years of data • Retail loans: Estimate PD by customer segment • Regulator provides severity of default (LGD) • Regulator approves institutions methodology • Applicable to “regional banks” or those approved by regulator

3. Advanced IRB Approach • Commercial loans: Institution estimates PD, LGD, and EAD • Retail loans: Same as Foundation approach • Adjustments for loan maturity, concentration, and risk enhancements • More rigorous documentation • Applicable to “Large, Internationally active banks”, or those approved by regulator

Operational Risks • Failed human practices, processes, and technology: Enron, WorldCom, Tyco • Fraud • Employment practice and work place safety • Clients, products and business practices • Damage to physical assets • Execution, delivery and process management • Alternative approaches • Percent allocation: 20% - 12% • Build a database for adverse events (type, frequency, severity)

Market Risk • Risk in trading book • Addressed in several amendments to Basel I, using VaR approaches • Interest rate risk not yet included in minimum capital requirement, yet explicit in FAMC, OFHEO regulations • Much Left to supervisory review

Dual Ratings • Rating the Customer • Risk classes • Probability of default by class • Rating the loan facility • Loan attributes • Collateral quality • Seniority of claim • 3rd party guarantees • Loss-given default by attribute

Loan Related LossGivenDefault ExposureatDefault x x The Dual Rating Idea CustomerRelatedProbabilityofDefault ExpectedLoss = x PD LGD EAD EL = Economic Capital includes UEL or the Unexpected Loss as well.

Risk Tolerance • ___% capital should be adequate ___% of the time • How Safe – How many vote for: • 50% of the time • 95% of the time • 99% of the time • 99.97% of the time • 100% of the time (don’t lend) • Now answer as a borrower… • Greater safety = more conservative = more expensive

Basel’s Risk Rating Factors • At a minimum, methods and data should account for: • Historical and projected cash flow repayment ability • Capital structure • Quality of earnings • Quality of information • Operating leverage • Financial efficiency • Financial flexibility: Liquidity • Management quality • Position in industry: Peer group standing • Country risk

Correlations and Concentrations • Very real effects • Correlations: How returns and losses move together; lower the better • Concentrations: Dominating portfolio positions by commodities and loan sizes • Measurement challenges • Basel adjusts for concentration and assumes an average correlation • Ag Losses unlikely to satisfy best principles for low correlation, low concentration, and easy diversification

Basel II in Pricing… • Loan pricing • Expected loss: provision and allowance • Unexpected loss: risk premium covers the cost of holding equity capital (see C8.xls) • Explicit cost of capital in loan pricing against actual RBC requirement for that loan exposure

Stress Testing • Shocking the model with significant downgrades of credit quality (increases in PD and LGD) and assessing capital adequacy • Could be linked to changes in borrower conditions, or macro conditions • Stress testing is an inherent part of enterprise-wide risk management • Economic capital models and measures should be designed to include stress testing

To Qualify an IRB system… • Portfolio broken into 9 or more groups: Corp, Retail, Bank, Sovereign, Equity, Project, etc., – not clear where ag fits • Must demonstrate ability to estimate PD and backfit (out of sample validation) – very tough for small community banks, small commercial banks with limited ag loans • Collect, store, and update key borrower/loan characteristics – very tough for ag loans, esp. mortgages • Board and Management Qualifications • Distinctions for credit risk that are “meaningful” • (i.e., cannot use scale where all loans get same score)

Possible Translations… • Development of IRB Risk Rating systems involves tradeoff between high fixed development cost and (potentially) lower flow costs. Favors large lenders with good data (FCS, a few large banks). • Increase pressure to consolidate. • Data becomes increasingly valuable. • Pay to play? Some may opt out, or contract for coordinated services • Successful == more accurate risk pricing as well. • RBCST parallels (tries to reflect Basel II ideas)

Possible Translations… • Markets are brutally efficient in long run – capital will seek its highest return. • Operational risk – much larger issue than in past. • Regulator are more “on the hook” in any case. • Basel and FFSC documents have some similar intent to “promote the standardization in capitalizing, reporting, and accounting…” (BIS). • Less data availability makes those that are available more valuable, and increases potential for more “overfitting”. • Disclosure pillar reduces distance (insulation) between management and boards. • Market discipline – embarrassment of non-compliance will be critical. • Regulated vs. unregulated lenders (i.e., how will Deere react?).

Top Ten Discussion Points • Regulators much more involved. • Incentive to avoid interest rate risk or convert to credit risk. • Pro-cyclicality (not good news for ag-lenders). • Flow advantages to IRB methods. • Fixed cost advantages of non-compliance and standard approaches. • Ostrich strategies will fail.

Top Ten Discussion Points – cont’d • Different effects on different types of lenders (coops vs. mutual, vs. stock vs. vendors) New opportunities for packaging/partnering with different firms if easier to lend to vendor than to customer. • Calibration to current “total on average, but not individual lenders” strongly favors IRB approaches, very scary for standard approaches. Current QIS4 and QIS5 Calibration examples seem extreme for ag loans with good collateral. • Catch-22 of establishing new compliant data systems with length of history requirements. • Extremely data dependent/model driven – strong likelihood for overfitting with existing ag data sets. Good potential for increased risk delineation. • “Lead or Follow” a meaningful strategic decision – especially for FCA

FCA Issues … • Huge benefits to standardized reporting, updating financials on current loans, and development of data warehousing. • Chance for System to manifest “demand for regulation” (ala Stigler, ADM,….) to suit comparative advantages • Additional pressures for historic data consolidation. • New more complicated incentives and payoffs to capital arbitrage – and new forms (e.g., w/FAMC). • BIS studies of effects of Basel I found few cases of credit rationing, likely to be worse with Basel II.