CHAPTER 2 FINANCIAL INSTITUTIONS

CHAPTER 2 FINANCIAL INSTITUTIONS. Meaning: Financial Institutions: an Institution which collects funds from the public and places them in financial assets, such as deposits, loans, bonds other than tangible property are called financial institutions.

CHAPTER 2 FINANCIAL INSTITUTIONS

E N D

Presentation Transcript

CHAPTER 2 FINANCIAL INSTITUTIONS

Meaning:Financial Institutions: an Institution which collects funds from the public and places them in financial assets, such as deposits, loans, bonds other than tangible property are called financial institutions. • Definition:It is an establishment that focus on dealing with financial transactions such as Investments, loans and deposits. Features of Financial Institution • It is an Institution as well as Intermediary. • It channelizes savings fund into investment fund. • It creates financial assets such as deposits, loans, securities etc. • It includes banking and non banking institutions. • And also includes both organized and unorganized institutions. • Established with a clear operating function. • Regulated by the government and regulating authority.

Classification of financial institutions: 1. Banking Institutions: These are the type of financial institutions which involve in accepting public deposits and lending the same to the needy customers. These are fundamentally established to earn profit, secondarily to safe guard the interest of the members. Its types are: • Commercial Banks: also called as Business banks • Public sector: Refer to a type of commercial banks that are nationalized by the government of a country. Public sector banks operate under the guidelines of Reserve Bank of India (RBI), which is the central bank • Private sector: Refer to a kind of commercial banks in which major part of share capital is held by private businesses and individuals. These banks are registered as companies with limited liability. • Regional Rural Banks (RRBs): Credit for Agriculture and other rural sectors. • Foreign banks: Refer to commercial banks that are headquartered in a foreign country, but operate branches in different countries. Citibank, American Express Bank, Standard & Chartered Bank

Cooperative banks: These are established to safeguard the interest of its members. These are organized on a cooperative basis, accept deposit and lend money to the required money to the required members. Co-Operative Banks are small financial institutions that offer the lending facility to the small businesses in both urban and non-urban regions. These are monitored and regulated by the Reserve Bank of India (RBI) and come under the Banking Regulations Act, 1949 as well as the banking laws act, 1965. Limited funds Do not operate mutual funds Objective to provide loans to farmers and small businessmen. Do not operate in national level and international level TYPES: Primary Credit Society: Village level and Town level (watch everyone avoid frauds) Central Co operative bank: A District level (same district) State Co operative bank: These are at the apex(highest level) co operative banks in all the states of the country.

Unorganized Financial Institutions: These are comprised with private money lenders, pawn brokers, indigenous bankers, traders etc. they lend money to the public from their own fund.(Operations and activities are not regulated by RBI). 2. Non Banking Financial Institutions: These are institutions which do not have full license or is not supervised by a National or International Banking Regulatory Agency. They facilitate bank related financial services such as • Provident and Pension Fund • Small Saving Organization • Life Insurance Corporation(LIC) • General Insurance Corporation(GIC) • Unit Trust of India(UTI) • Mutual Funds • Investment Trust etc.

Importance of Financial Institutions: • Provide funds:Financial institutions provide funds for the investment and industrial activities. Active sources which offer appropriate source of funds to the requirement of institutions and individuals. • Infrastructural facilities:Financial institutions also offer basic infrastructural facilities needed for the development and promotion of lucrative ventures. Infrastructural facilities involve development of industrial estates, tech parks, road and water etc. • Promotional activities:To mobilize the funds, reduce the risk of selling financial securities, arrangement of working and long term capital of the business. • Development of Backward areas:Financial institutions also take social responsibilities of developing the backward areas at free cost by offering credit facilities, free education, employment creation etc. • Planned development: Financial institutions initiate all planned developments in the view of economic growth of the state and are coordinated with the government plan and social welfare. • Accelerating industrialization: as the financial institutions are established to earn the profit and safeguard interest of its members, they accelerate the industrialization to contribute industrial growth. They support the industries by granting finance, project development and consultancy. • Employment generation:Channelizing the funds for investment, building of industrial facilities and acceleration of industries generates the employment to the educated and qualified people of the state.

Functions of Financial Institution: Primary functions • Accepting deposits:Financial institutions accept deposits from the public. They offer different schemes to mop up public deposits from the customers.(Give in return in the form of interest on deposit tenure basis). • Providing commercial loans:Accepted deposits are used for commercial lending operations in the form of loans, advances, cash credits, bills discounting etc. (Fetch good returns). • Providing real estate loans: The financial institutions also provide loans and advances for real estate industries to purchase site, build premises, construction industrial and residential parks. • Providing mortgage loans:The financial institutions also provide loans to the needy group on mortgage of properties and collateral securities.( Gold loans, property loan etc.). • Issuing share certificates:Financial institutions also constitutes accepting shares investment money from the investors and issuing them certificates on behalf of the companies.

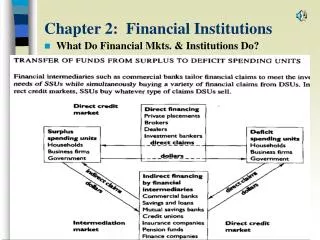

Secondary Functions: • Act as an intermediary:Between the savings community and industrialists. Receives the deposits at a lower rate of interest and lend the same fund to the needy group at a higher interest.(Difference amount is profit for their intermediary work). • Facilitate the flow of money:They also facilitate the flow/channelize the money to the investment activities. Financial institutions are the interlinked path stones to make smooth flow of fund from small savers to giant business ventures. • Managing Risk and Uncertainty: Efficient system helps us to control risk and increase the return. • Provide ways to transfer economic resources through time and across distance. • Clearing and settling payments: Clearing is the process of updating the accounts of the trading parties and arranging for the transfer of money and securities. Settlement is the actual exchange of money, or some other value, for the securities.

INDUSTRIAL FINANCE CORPORATION OF INDIA (IFCI) • IFCI was established as a statutory corporation on 1st July 1948 by special Act of Parliament, IFCI Act, 1948. • It was converted into a public limited company on July 1, 1993. • Its main object is to provide medium and long term credit to eligible industrial concerns in corporate sectors of the economy, particularly to those industries to which banking facilities are not available. OBJECTIVES: • To provide long and medium-term credit to industrial concerns engaged in manufacturing, mining, shipping and electricity generation and distribution. • The period of credit can be as long as 25 years and should not exceed that period. • To grant credit to a single concern up to a maximum amount of rupees one crore. This limit can be exceeded with the permission of the government under certain circumstances. • Underwrite and directly subscribe to shares and debentures issued by companies. • Assist in setting up new projects as well as in modernization of existing industrial concerns in medium and large scale sector. • To deal, transact buy and sell foreign currencies. • Act’s as trustee, executor, administrator, treasurer and trust.

Functions Of IFCI • It provides direct assistance to industries in the form of Term Loans. • It provides Rupees and Foreign currency loans to the corporate to encourage foreign trade. • It provides leasing and Hire-Purchase financing to industrial establishments. • It conducts Entrepreneurial Development Programmes. • IFCI finance the projects of self-employed , handicapped and blind people. • Seed capital assistance will be provided by IFCI through the State Financial Corporation (capital required at initial stages of a business concern) • To encourage the high-tech project or to encourage young scientist, venture capital is being provided. • It provides financial assistance to sick units. • It undertakes the activity of syndication of loans. SUBSIDARIES AND ASSOCIATES OF IFCI • IFCI Infrastructure Development Ltd. • IFCI Factors limited, financial services Ltd. • IFCI Venture Capital Funds ltd • Technical Consultancy organisations

IDBI: Industrial Development bank of India • IDBI: Industrial Development bank of India (IDBI) was constituted under Industrial Development bank of India Act, 1964 as a Development Financial Institution (DFI) and came into being as on July 01, 1964 wide government of India notification dated June 22, 1964.Its headquarters in Mumbai, India. RBI categorized IDBI as on “other public sector bank”. • Objectives The main objectives of IDBI is to serve as the apex institution (second tier or wholesale organisations that channels funding to multiple micro finance institutions) for term finance for industry in India. • Co-ordination, regulation and supervision of the working of other financial institutions such as IFCI , ICICI, UTI, LIC, Commercial Banks and SFCs. • Supplementing the resources of other financial institutions and there by widening the scope of their assistance. • Planning, promotion and development of key industries and diversification of industrial growth. • Devising and enforcing a system of industrial growth that conforms to national priorities.

Functions • To grant loans and advances to IFCI, SFCs or any other financial institution by way of refinancing of loans granted by such institutions which are repayable within 25 year. • To grant loans and advances to scheduled banks or state co-operative banks by way of refinancing of loans granted by such institutions which are repayable in 15 years. • To discount or re-discount bills of industrial concerns. • To underwrite or to subscribe to shares or debentures of industrial concerns. • To subscribe to or purchase stock, shares, bonds and debentures of other financial institutions. • To grant line of credit or loans and advances to other financial institutions such as IFCI, SFCs, etc. • To grant loans to any industrial concern. • To provide consultancy and merchant banking services in or outside India. • To provide technical, legal, marketing and administrative assistance to any industrial concern or person for promotion, management or expansion of any industry. • Planning, promoting and developing industries to fill up gaps in the industrial structure in India. • To act as trustee for the holders of debentures or other securities.

Subsidiaries of IDBI • Small Industrial Development Bank of India(SIDBI) • IDBI bank ltd • IDBI Capital market services • IDBI Investment Management Company

INDUSTRIAL CREDIT AND INVESTMENT CORPORATION OF INDIA (ICICI) • The Industrial Credit and Investment Corporation of India or ICICI was established on 5th January, 1955 to assist industrial units in the private sector. It was sponsored by the World Bank. Objectives: • To assist in the creation, expansion and modernization at industrial units in the private sector. • To encourage the inflow and participation of foreign capital in the private sector industrial units. • To expand the investment market in India. • To provide equipment finance. • To provide finance for rehabilitation of industrial units. Functions: The main functions of ICICI are as follows: • To sponsor and underwrite new issues. • To provide medium and long-term loans to industrial units in the private sector. • To guarantee loans taken from other private sources. • To furnish managerial, technical and administrative advice to industrial units by the private sector. • To make funds available for reinvestment. • To advance loans in foreign currency towards the cost of imported capital equipment. • To extend guarantee for deferred payments. • To purchase the shares and debentures of new companies.

The important features of the functioning of the ICICI arc as given below: • (i) The financial assistance as provided by the ICICI includes rupee loans, foreign currency loans, guarantees, underwriting of shares and debentures, and direct subscription to shares and debentures. • (ii) Originally, the ICICI was established to provide financial assistance to industrial concerns in the private sector. But, recently, its scope has been widened by including industrial concerns in the public, joint and cooperative sectors. • (iii) ICICI has been providing special attention to financing riskier and non-traditional industries, such as chemicals, petrochemicals, heavy engineering and metal products. • (iv) Of late, the ICICI has also been providing assistance to the small scale industries and the projects in backward areas. • (v) Along with other financial institutions, the ICICI has actively participated in conducting surveys to examine industrial potential in various states. • (vi) In 1977, the ICICI promoted the Housing Development Finance Corporation Ltd. to grant term loans for the construction and purchase of residential houses. • (vii) Since 1983, the ICICI has been providing leasing assistance for computerisation, modernisation and replacement schemes; for energy conservation; for export orientation; for pollution controller balancing and expansion: etc.

EXPORT AND IMPORT BANK (EXIM BANK) • EXIM Bank is the premier finance institution of the country, established in 1982 under the export-import bank of India Act,1981.The head quarters of the bank is located in Mumbai. It is established to finance and support export and import activities. Objectives • To provide financial assistance to exporters and importers. • To ensure and integrated and co-ordinated approach in solving the allied problems encountered by exporters in India. • To function as the principal financial institution for coordinating the working institutions engaged in financing export and import of goods and services with a view to promoting the country’s international trade. • Ensure an integrated and coordinated approach to solving the problems of exporters • Provide special attention to capital goods export and export of technical services • Tap domestic and overseas markets for resources, undertake development and finance activities in the areas of exports. • Provide refinance facilities to commercial banks and financial institutions against their export-import financing activities.

Functions of EXIM Bank • Corporate Banking Group: which handles a variety of financing programs for Export Oriented Units (EOUs), Importers, overseas investment by Indian companies. • Project Finance/Trade Finance Group: handles the entire range of export credit services such as supplier’s credit, pre-shipment Agri Business group etc. The project also handles project and export transactions in the agricultural sector for financing. • Export Services Group: Offers variety of advisory and value added information services aimed at investment promotion. • Export marketing services: Bank offers assistance to Indian companies, to enable them establish their products in overseas market. • Support services group which include research and planning, corporate finance, loan recovery, internal audit, HRM, legal, IT etc. • It provides direct financial assistance to exporters of plant, machinery and related service in the form of medium-term credit. • Underwriting the issue of shares, stocks, bonds, debentures of any company engaged in exports. • It provides rediscount of export bills for a period not exceeding 90 days against short-term usage export bills discounted by commercial banks. • The bank gives overseas buyers credit to foreign importers for import of Indian capital goods and related services. • Developing and financing export oriented industries.

Life Insurance Corporation of India (LIC) LIC came into existence on July 1, 1956 and the LIC began to function on September 1, 1956. LIC formed by an Act of Parliament, viz. LIC Act, 1956, with a capital contribution of Rs. 5 crore from the Government of India. Objectives: • To act as trustees of the insured public in their individual and collective capacities. • To mobilize maximum savings of the people by making insured savings more attractive. • To extend the sphere of life insurance and to cover every person eligible for insurance under insurance umbrella. • Promote all employees and agents of the LIC, in the sense of participation and job satisfaction through discharge of their duties with dedication towards achievement of LIC objectives. • To ensure economic use of resources collected from policy holders. (help to provide services) • To conduct business with utmost economy and with the full realization that the money belong to the policy holders. • Meet the various life insurance needs of the community that would arise in the changing social and economic environment.

Role and Functions of LIC • It collects the savings of the people through life policies and invests the fund in a variety of investments. • It invests the funds in profitable investments so as to get good return. Hence the policy holders get benefits in the form of lower rates of premium and increased bonus. • It subscribes to the shares of companies and corporations. It is a major shareholder in a large number of blue chip companies. • It provides direct loans to industries at a lower rate of interest. It is giving loans to industrial enterprises to the extent of 12% of its total commitment. • It provides refinancing activities through SFCs in different states and other industrial loan giving institutions. • It has provided indirect support to industry through subscriptions to shares and bonds of financial institutions such as IDBI, IFCI, ICICI, SFCs etc. at the time when they required initial capital. It also directly subscribed to the shares of Agricultural Refinance Corporation and SBI. • It gives loans to those projects which are important for national economic welfare. The socially oriented projects such as electrification, sewage and water channelizing are given priority by the LIC. • It gives housing loans at reasonable rates of interest. • It acts as a link between the saving and the investing process. It generates the savings of the small savers, middle income group and the rich through several schemes.

SFC (State Financial Corporation): It was setup under industrial financial corporation Act 1948, in order to provide small and medium term credit to industries of the states. Besides, SFCs are helpful in ensuring balanced regional development, higher investment, more employment generation and broaden the ownership of industries. Objectives • To provide incentives to new industries. • To bring efficiency in regional industrial units. • To provide finance to small scale, medium sized and cottage industries in the state. • To develop regional financial resources. • Provide term loans for the acquisition of land, building, plant and machinery. • Promotion of self-employment. • Encourage women entrepreneurs. • Expansion of industry. • Provide seed capital assistance.

FUNCTIONS: • The SFCs grant loans mainly for acquisition of fixed assets like land, building, plant and machinery. • The SFCs provide financial assistance to industrial units whose paid-up capital and reserves do not exceed Rs. 3 crore • Grant of loans and advances to or subscribe to debentures of industrial concerns repayable within a period not exceeding 20 years. • Underwriting of the issue of stock, shares, bonds or debentures by industrial concerns. • To make payment of capital goods purchased in India by these industrial units. • Planning and assisting in the promotion and development of industries. • Guarantees the deferred payments for the purchase of plants, machinery etc within the country.

Prohibited Functions: • Not to accept public deposits for a period exceeding 5 years. • Not to accept deposits exceeding the paid-up capital. • Not to give loans on the security of its shares. • Not to declare dividend on its shares without sanction of the Central Government. • Not to purchase shares and stocks directly of an industrial unit or limited public company.

NABARD: NATIONAL BANK FOR AGRICULTURE AND RURAL DEVELOPMENT. It is the apex banking institution to provide finance for Agriculture and rural development. National Bank for Agriculture and Rural Development (NABARD) was established on July 12, 1982 with the paid up capital of Rs. 100 cr, by 50: 50 contribution of government of India and Reserve bank of India. It is an apex institution in rural credit structure for providing credit for promotion of agriculture, small scale industries, cottage and village industries, handicrafts etc. Objectives of NABARD: • NABARD provides refinance assistance for agriculture, promoting rural development activities. It also provides all necessary finance and assistance to small scale industries. • It improves small and minor irrigation by way of promoting agricultural activities. • It maintains a research and development fund to promote research in agriculture and rural development. • NABARD promotes various organizations involved in agricultural production by contributing to their capital. • It co-ordinates all agricultural and rural development activities with the objective of tying them up with planned development activities in the rural sector. • NABARD is responsible for regulating and supervising the functions of Co-operative banks and RRBs.

FUNCTIONS: • NABARD provides refinancing facilities to Commercial banks, State co-operative banks, Central Co-operative banks, Regional rural banks and Land Development banks. • It provides refinancing to agriculture, small scale industries and other village and cottage industries by lending to commercial banks. • The bills of commercial and co-operative banks are discounted to enable them to finance for agricultural operations. • During natural calamities, such as droughts, crop failure and floods, the bank helps by refinancing commercial and cooperative banks so that the farmers tide over their difficult period. • Provide financial support for the training institutes of cooperative banks, commercial banks and Regional Rural Banks. • Provide financial assistance to cooperative banks for building improved management information system, computerization of operations and development of human resources. • It also runs programs for agriculture and rural development. • It also supports Vikas volunteer Vahini programs which offer credit and development activities to poor farmers. • It provides long-term assistance (not exceeding 20 years) to State Governments.

Definition: A mutual fund is a common pool of money into which investors place their contributions that are to be invested in different types of securities such as stocks, bonds, money market instruments and similar assets in accordance with the stated objective. FLOW CHART OF MUTUAL FUNDS

Classification based on structure • Open-ended Fund/ Scheme: An open-ended Mutual fund is one that is available for subscription and repurchase on a continuous basis. These Funds do not have a fixed maturity period.( UK Bonds, US Bonds) • Close-ended Fund/ Scheme: A close-ended Mutual fund has a stipulated maturity period e.g. 5-7 years. The fund is open for subscription only during a specified period at the time of launch of the scheme. (UTI MNC Fund, Reliance Money Manager Fund, HDFC Cash Management Fund). • Interval Schemes : Interval Schemes are that scheme, which combines the features of open-ended and close-ended schemes. Open-end funds may represent a safer choice than closed-end funds, but the closed-end products might produce a better return, combining both dividend payments and capital appreciation

Classification based on Investment objectives 1) Growth Schemes are also known as equity schemes. The aim of these schemes is to provide capital appreciation over medium to long term. These schemes normally invest a major part of their fund in equities and are willing to bear short-term decline in value for possible future appreciation. 2) Income Schemes are also known as debt schemes. The aim of these schemes is to provide regular and steady income to investors. These schemes generally invest in fixed income securities such as bonds and corporate debentures. Capital appreciation in such schemes may be limited. 3) Balanced Schemes aim to provide both growth and income by periodically distributing a part of the income and capital gains they earn. These schemes invest in both shares and fixed income securities, in the proportion indicated in their offer documents (normally 50:50). 4) Money Market Schemes aim to provide easy liquidity, preservation of capital and moderate income. These schemes generally invest in safer, short-term instruments, such as treasury bills, certificates of deposit, commercial paper and inter-bank call money.

Classification based on other schemes • Tax-saving schemes offer tax rebates to the investors under tax laws prescribed from time to time. Under Sec.88 of the Income Tax Act, contributions made to any Equity Linked Savings Scheme (ELSS) and pension scheme are eligible for rebate. • Special schemes are classified into industry specific schemes, index schemes and sectoral schemes Index schemes This schemes invest in the securities in the same weightage comprising of an index. This schemes would rise or fall in accordance with the rise or fall in the index such as the BSE Sensex or the CNX S&P Nifty. Sectoral schemes Such fund invest in specific sectors of the economy. The specialized sectors may include real estate infrastructure, oil and gas etc, offshore investments, commodities like gold and silver. IndustrySpecific schemesSector funds/schemes which invest in the securities of only those sectors or industries as specified in the offer documents. e.g. Pharmaceuticals, Software, Fast Moving Consumer Goods (FMCG), Petroleum stocks, etc.

Various Mutual funds in India • State Bank of India mutual fund • ICICI prudential mutual fund • TATA mutual fund • HDFC mutual fund • Birla sun life mutual fund • Reliance mutual fund • Kotak Mahindra mutual fund etc.. Advantages of Mutual Funds • Liquidity: Investors may be unable to sell shares directly, easily and quickly. When they invest in mutual funds, they can cash their investment any time by selling the units to the fund if it is open-ended. • Convenience and Flexibility: Investors can easily transfer their holdings from one scheme to other, get updated market information and so on. Funds also offer additional benefits like regular investment and regular withdrawal options.

Transparency: Fund gives regular information to its investors on the value of the investments in addition to disclosure of portfolio held by their scheme, the proportion invested in each class of assets and the fund manager's investment strategy and outlook • Portfolio diversification: It enables him to hold a diversified investment portfolio even with a small amount of investment like Rs. 2000/-.( Balance Risk and Return) • Professional management: The investment management skills, along with the needed research into available investment options, ensure a much better return as compared to what an investor can manage on his own. • Reduction/Diversification of Risks: The potential losses are also shared with other investors. • Reduction of transaction costs: The investor has the benefit of economies of scale; the funds pay lesser costs because of larger volumes and it is passed on to the investors. • Wide Choice to suit risk-return profile: Investors can chose the fund based on their risk tolerance and expected returns.

Disadvantages of Mutual funds • No guarantees: No investment is risk free. If entire declines in the value, the value of mutual fund shares will go down as well, no matter how balanced the portfolio. • Fees and commissions: all funds charge administrative fees to cover their day to day expenses. • Taxes: If the fund makes a profit then investor has to pay taxes on the profit, even if investor reinvests the money trade. • Management risk: when the investor invests in mutual fund, then investor has to depend on the fund’s manager to make the right decision regarding the fund’s portfolio. • Fluctuating returns: Mutual funds are like many other investments without a guaranteed return; there is always the possibility that the value of your mutual fund will depreciate. 6. Misleading advertisements: The misleading advertisements of different funds can guide investors down the wrong path. 7. Diversification: the diversification is dangerous to the investors when the diversifying is relatively same.