Download

1 / 79

790 likes | 939 Vues

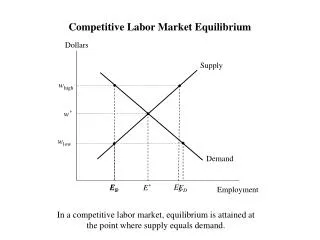

The purpose of this simulation is to create a competitive market and to observe the market as it achieves equilibrium. In this experiment, you will experience real market forces. The same human traits and behaviors that govern real markets exist in the simulation.

E N D

The purpose of this simulation is to create a competitive market and to observe the market as it achieves equilibrium. In this experiment, you will experience real market forces. The same human traits and behaviors that govern real markets exist in the simulation. What are artificial are your surroundings. The market forces are real.

The Players and the Goals In this experiment, there are CONSUMERS and INSURERS. INSURERS sell INSURANCE. CONSUMERS buy FOOD and INSURANCE.

Consumers Each consumer has $20 to spend. A unit of food costs $1. $20 The more food the consumer eats, the happier the consumer becomes.

Consumers: The Catch Each consumer faces some risk of badness. If badness befalls the consumer, the consumer loses all of the purchased food. vs.

Consumers: The Insurance But, consumers can purchase insurance contracts from the insurance companies. Each contract pays the consumer $1 if badness befalls that consumer. The consumer automatically buys food with the $1.

15 food 10 insurance contracts Consumers: Example Suppose a consumer can purchase insurance contracts at a price of $0.50 each (the price of food is always $1 each). Suppose that the consumer spends $5 on insurance contracts. The remaining $15 is automatically spent on food. $20 $15 $5 (Consumers may buy fractions of a unit of food.)

Consumers: Example If badness does not befall the consumer, the consumer eats 15 units of food and is very happy. Very Happy !!

Consumers: Example If badness does befall the consumer, the 15 units of food disappear, each insurance contract pays $1. The consumer automatically buys food and the consumer is somewhat happy. Somewhat Happy

Consumers • Each consumer’s goal: Maximize happiness • More insurance means • More food when badness befalls. • Less food when badness does not befall. • Too little insurance is bad. Too much insurance is also bad.

Insurers Each insurer can write as many insurance contracts as liked and charge any price.

Insurers If badness does not befall the consumer, the insurer walks away with the money the consumer paid for the contracts. $ $ $ $ $ $

Insurers If badness does befall the consumer, the insurer pays the consumer $1 for each contract the insurer sold the consumer.

Insurers: Example Suppose an insurer sells Consumer A six contracts for $0.60 each, and sells Consumer B five contracts for $0.30 each. The insurer collects $3.60 from Consumer A and $1.50 from Consumer B. Revenue = $5.10 $3.60 $1.50

$5.00 Insurers: Example Suppose badness befalls Consumer B but not Consumer A. The insurer owes Consumer B $1 for each contract Consumer B purchased. Revenue = Cost = Profit = $5.10 $5.00 $0.10

$6.00 Insurers: Example Suppose badness befalls Consumer A but not Consumer B. The insurer owes Consumer A$1 for each contract Consumer A purchased. Revenue = Cost = Loss = $5.10 $6.00 $0.90 (Insurers do not need cash reserves to cover policies.)

Insurers • Each insurer’s goal: Maximize expected profit • Insurers can ask whatever prices they like for contracts • Too low a price is bad. Too high a price is also bad.

Badness There are five types of consumer. Each faces a different probability of badness. Type 1 Type 2 Type 3 Type 4 Type 5 10% 20% 30% 40% 50%

The Objects = insurance contract(s) = sales register

Contracts Customer 6 purchases 12 contracts from insurer for $0.40 each. 12 6 $4.80 The total cost is the number of contracts multiplied by the agreed price per contract.

$4.80 $6.00 -$1.20 Register $4.80 6 12 $3.60 $1.20 0.3 6 12 0.5 The register is for your own use in tracking your expected costs. Feel free to cross out and re-enter information when your suspected risk for a consumer changes. Only give your agent one contract form at a time. Otherwise, you’ll likely miss recording sales.

$0.50 The Mechanics Insurers Consumers Agent Head Office Prices are per contract. You may buy multiple contracts.

The Mechanics Insurers Consumers Agent Head Office

The Mechanics Insurers Consumers Agent Head Office Head Office: Keep track of your expected profits. Judge risk based on offer prices. Consumers: Keep track of how much you have spent. You need to save cash to buy food and you only have $20.

Consumers: Buy some insurance. All remaining money goes to food. Insurers: Sell insurance to maximize expected profit. Agent Head Office Head Office: Keep track of your expected profits. Consumers: Keep track of your spending. You only have $20!

Accounting Phase • Consumers report: • Contracts purchased, cost, and from which insurer(s)

Mandated Insurance Concerned that some consumers do not have enough insurance coverage, the law stipulates that an insurer may not sell fewer than 50 contracts to a buyer unless the buyer has already purchased at least 50 contracts (from any insurer) this round.

Consumers: Buy some insurance. All remaining money goes to food. Insurers: Sell insurance to maximize profit. You may not sell a buyer fewer than 50 contracts. Agent Head Office Head Office: Keep track of your expected profits. Consumers: Keep track of your spending. You only have $20!

Accounting Phase • Consumers report: • Contracts purchased, cost, and from which insurer(s)

Mandatory Insurance Concerned that some consumers do not have any insurance, the law requires that all consumers buy not less than 50 contracts this round.

Consumers: Buy some insurance. All remaining money goes to food. You must buy at least 50 contracts. Insurers: Sell insurance to maximize profit. Agent Head Office Consumers: Keep track of your spending. You only have $20! Head Office: Keep track of your expected profits.

Accounting Phase • Consumers report: • Contracts purchased, cost, and from which insurer(s)