Download

1 / 5

50 likes | 102 Vues

What is SIP? Systematic investment plan (SIP) is a disciplined way of investing in mutual funds, allows you to invest a certain amount at regular intervals. Get the aspects of SIP with HDFC Securities.

E N D

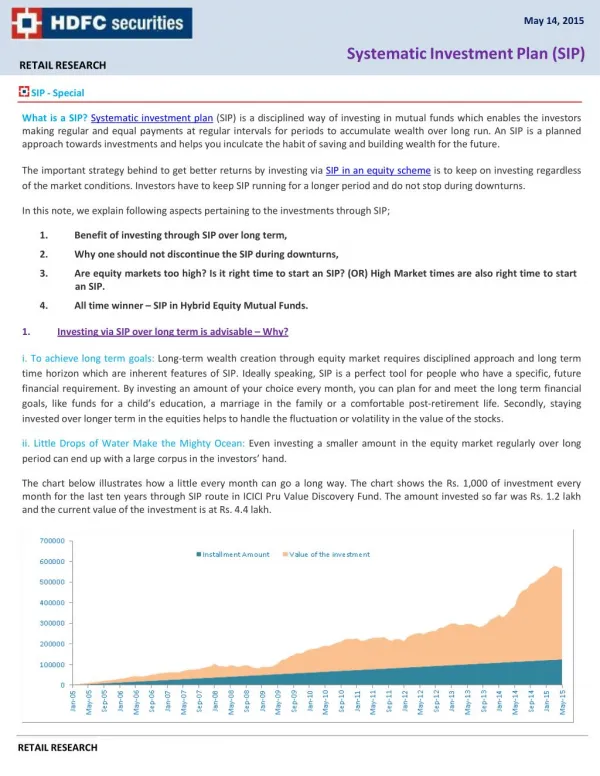

May 14, 2015 Systematic Investment Plan (SIP) RETAIL RESEARCH SIP - Special What is a SIP? Systematic investment plan (SIP) is a disciplined way of investing in mutual funds which enables the investors making regular and equal payments at regular intervals for periods to accumulate wealth over long run. An SIP is a planned approach towards investments and helps you inculcate the habit of saving and building wealth for the future. The important strategy behind to get better returns by investing via SIP in an equity scheme is to keep on investing regardless of the market conditions. Investors have to keep SIP running for a longer period and do not stop during downturns. In this note, we explain following aspects pertaining to the investments through SIP; 1. Benefit of investing through SIP over long term, 2. Why one should not discontinue the SIP during downturns, 3. Are equity markets too high? Is it right time to start an SIP? (OR) High Market times are also right time to start an SIP. 4. All time winner – SIP in Hybrid Equity Mutual Funds. 1. Investing via SIP over long term is advisable – Why? i. To achieve long term goals: Long-term wealth creation through equity market requires disciplined approach and long term time horizon which are inherent features of SIP. Ideally speaking, SIP is a perfect tool for people who have a specific, future financial requirement. By investing an amount of your choice every month, you can plan for and meet the long term financial goals, like funds for a child’s education, a marriage in the family or a comfortable post-retirement life. Secondly, staying invested over longer term in the equities helps to handle the fluctuation or volatility in the value of the stocks. ii. Little Drops of Water Make the Mighty Ocean: Even investing a smaller amount in the equity market regularly over long period can end up with a large corpus in the investors’ hand. The chart below illustrates how a little every month can go a long way. The chart shows the Rs. 1,000 of investment every month for the last ten years through SIP route in ICICI Pru Value Discovery Fund. The amount invested so far was Rs. 1.2 lakh and the current value of the investment is at Rs. 4.4 lakh. RETAIL RESEARCH

iii. Investing through SIP for longer time frame achieved better results compared to short term periods: The below chart shows the growth of investments which were made in Sensex in various time frames through SIP mode. No doubt, investing through SIP for longer time frame achieved better results compared to short term periods. Benefits of staying invested long term: iv. The longer the time-frame, the larger are the benefits of averaging: Equity markets are volatile and move in a cycle. They go up, peak, go down and then bottom. When one cycle is finished, the next begins. SIPs make the market volatility and cycles work in favour of an investor and help in averaging out the cost. The concept is commonly referred to as “rupee cost averaging”. More units are purchased when a scheme’s NAV is low (during market low) and fewer units when the NAV is high (during market up). Hence, when the two cases are taken together, the cost is averaged out. The longer the time frame, the larger are the benefits of averaging. The below table also describes the benefit of investing through SIP over long run. XIRR Returns (%) Benchmark 1 Yr SIP 4.24 2.29 5 Yrs SIP 13.59 13.25 10 Yrs SIP 11.74 11.51 15 Yrs SIP 15.02 15.37 CNX Nifty Index S&P BSE Sensex 2. Don’t discontinue SIP during market corrections: Many investors make the mistake of discontinuing their SIP investments when market falls. This exit could impact the portfolio returns significantly as it fails to get the opportunity to average costs. As discussed above, more units can be purchased when a scheme’s NAV is low (during market low) and fewer units can be bought when the NAV is high (during market up), hence the investor can achieve averaging the cost out. Investments through an SIP can ensure steady returns. Ideally speaking, it is difficult to time the market. Whereas, with an SIP, investors can ride safely during market downturns and manage better returns if they stay invested through an entire market cycle. We have conducted a study to justify the fact that the investor who stops the SIP during the market bottom tend to lose out and end up with lower returns as compared to the SIP that are redeemed in the next peak of the bottom. RETAIL RESEARCH

We have chosen 5 different periods wherein the domestic equity market witnessed their bottoms (from the Sensex movement) in the last 10 years period. Also, the peaks successive to these bottoms are considered for the study. We have calculated the SIP returns for the different time frames from the Sensex (assuming investing in Sensex through SIP) that all were redeemed during the bottoms and their successive peaks. The comparison results shows that the SIPs that were redeemed during market bottoms showed lower and poor returns than the SIPs that were redeemed in the next peak of the respective bottoms. Interestingly, in most of the scenarios that chosen, the time gap between the bottom and its successive peaks are at 6 months to one year. The below tables illustrate the SIP returns (XIRR) (%) with different time frames done in the Sensex. In scenario I, we have considered the period 14 June 2006 as bottom and 20 Feb 2007 as the successive peak. We have assumed those two dates as redemption dates and calculated SIP returns for one, three, five, seven, ten, twelve and fifteen years for both periods. The results clearly show that the SIPs that were redeemed during bottom ended with lower returns compared with that of the SIPs which were redeemed in the successive peak. That means, the SIPs that were redeemed on 14 June 2006 posted lower returns compared to the SIPs that were redeemed on 20 Feb 2007. We can see the same results in the remaining scenarios as well. To conclude, SIP investors need not to worry about the fluctuations or ups and down that are seen in the equity market. You could grab better returns in the next 6 to 12 months period if you stay invested during market falls. Scenario I: Redemption details XIRR Returns (%) Redemption during market Bottom Next Peak How to read the table: The figure ‘-3.84’shown in the second row and fourth column is the XIRR returns (%) from the one year SIP that was redeemed on 14th Jun 2006. Since it was a one year SIP, the first installment was made on 1st July 2005 with Rs. 1,000 each for the 12 months. Redemption date 14-Jun-06 20-Feb-07 Sensex value 8,929 14,253 1 Yr SIP -3.84 45.40 3 Yrs SIP 26.21 47.56 5 Yrs SIP 28.39 42.33 7 Yrs SIP 19.78 31.72 10 Yrs SIP 14.96 22.55 12 Yrs SIP 12.68 19.20 15 Yrs SIP 11.31 15.82 The chart below also explains the same. RETAIL RESEARCH

We can see the same trend in the following scenarios as well. Scenario II: Redemption details XIRR Returns (%) Redemption during market Bottom Next Peak Redemption date 9-Mar-09 12-Jun-09 Sensex value 8,160 15,238 1 Yr SIP -58.38 93.25 3 Yrs SIP -29.97 10.13 5 Yrs SIP -6.00 17.68 7 Yrs SIP 6.52 23.01 10 Yrs SIP 7.80 19.26 12 Yrs SIP 7.84 17.22 15 Yrs SIP 7.21 14.54 Scenario III: Redemption details XIRR Returns (%) Redemption during market Bottom Next Peak Redemption date 25-May-10 5-Nov-10 Sensex value 16,022 21,005 1 Yr SIP -5.35 31.13 3 Yrs SIP 8.79 24.48 5 Yrs SIP 10.46 16.07 7 Yrs SIP 16.79 19.85 10 Yrs SIP 18.89 22.11 12 Yrs SIP 16.87 19.30 15 Yrs SIP 14.50 16.62 Scenario IV: Redemption details XIRR Returns (%) Redemption during market Bottom Next Peak Redemption date 1-Jun-12 13-Feb-13 Sensex value 15,965 19,608 1 Yr SIP -13.52 19.85 3 Yrs SIP -5.95 5.95 5 Yrs SIP 0.99 9.19 7 Yrs SIP 4.30 7.67 10 Yrs SIP 12.67 13.50 12 Yrs SIP 13.48 15.48 15 Yrs SIP 12.37 14.05 Scenario V: Redemption details XIRR Returns (%) Redemption during market Bottom Next Peak Redemption date 27-Aug-13 23-Sep-14 Sensex value 17,968 26,776 1 Yr SIP -12.60 38.09 3 Yrs SIP -0.91 23.29 5 Yrs SIP 4.92 14.59 7 Yrs SIP 3.90 13.38 10 Yrs SIP 9.28 13.23 12 Yrs SIP 13.01 15.91 15 Yrs SIP 12.48 15.79 3. Are the equity markets at highs? Is it right time to start an SIP? The below table portrays the 3 Years SIP returns (XIRR) (%) of the different equity oriented categories that were started in the different periods of market cycles seen in the last 8 years periods (redeemed after respective 3 years) . From the table one can understand that the SIP that was started during market peak (on 01-Jan-2008) posted better or similar returns to that of the SIP investment made on 01-Jan-2012. The 01-Jan-2008 was the period wherein the domestic equity market saw its peak (Sensex value crossed 20,000 mark). Since, it is a 3 years SIP, it was redeemed on 31-Dec-2010 (wherein the Sensex touched again the 20,000 mark after a significant correction). On the other hand, the SIP investment that was started on 01-Jan-2012, posted better returns as it is redeemed during rising markets. The rest of the periods’ SIP that started on Jan-07, Jan-09, Jan-10 and Jan-11 delivered lower or negative returns. Category 01-Jan-07 01-Jan-08 25.00 29.48 26.65 20.48 9.11 01-Jan-09 01-Jan-10 01-Jan-11 01-Jan-12 27.18 44.24 30.87 26.21 13.64 Large-cap Mid & Small cap Multi-cap Hybrid - Equity MIP Benchmark S&P BSE SENSEX Value S&P BSE SENSEX Returns (%) How to read the table: For example, returns shown in the “Jan 07” column are for the SIP that started on 01-Jan-2007 and redeemed on 31-Dec-2009. 18.56 19.89 19.58 15.32 9.50 -0.44 1.81 0.01 1.91 5.05 7.36 11.04 7.79 8.76 8.44 8.98 12.31 8.56 9.95 7.59 13,942 15.67 20,301 23.52 9,903 -1.21 17,559 5.66 20,561 9.55 15,518 21.74 RETAIL RESEARCH

To conclude, the better performance of the SIP that started on 01-Jan-2008 was attributable to the Rupee Cost Averaging as it accumulated more units when the equity market was falling. That means that the SIP was started at market peak and the rest of every installments were made during market falls which helped to accumulate more units. This SIP ended with greater returns even the redemption NAV (on 31-Dec-2010) was as equal to starting day NAV (on 01-Jan-2008). Investors can start an SIP at any point, keep on accumulating units during market fall and fluctuations and can consider redeeming when the NAV comes back closer to the same value of the starting day NAV or higher. Since the market moves in a cycle it may take close to two to three years to bounce back the expected level. On the other hand, starting the SIP at the bottoms does not guarantee better SIP returns as is evident from returns generated by SIPs starting from Jan 01, 2009. 4. SIP in Hybrid - Equity Mutual Funds The above table further portrays the consistent and balanced performance of the Hybrid – Equity Oriented schemes in all set of periods irrespective of market cycles such as bull, bear, volatile periods. Though the Hybrid – Equity Oriented category showed moderate or underperforming returns during market upturns compared to other equity diversified categories, the category posted outperforming returns during market corrections. Hence, the ultra-conservative investors can consider investing in these schemes. Interestingly top performing schemes from the Hybrid – Equity Oriented category managed to post better outperforming returns during market fall and similar returns that of equity diversified schemes during market rallies. 3 Years SIP performance of the top performing schemes from Hybrid – Equity Oriented category: Category 1-Jan-07 1-Jan-08 1-Jan-09 1-Jan-10 1-Jan-11 1-Jan-12 HDFC Balanced Fund(G) HDFC Prudence Fund(G) Tata Balanced Fund(G) Birla SL '95 Fund(G) Benchmark Average of Large-cap Category Average of Mid & Small cap Category 22.02 25.20 21.27 21.91 29.64 33.36 23.98 26.75 9.84 8.12 6.08 5.56 10.82 10.57 11.96 9.20 11.70 8.67 12.31 9.61 32.58 30.64 31.85 30.28 18.56 19.89 25.00 29.48 -0.44 1.81 7.36 11.04 8.98 12.31 27.18 44.24 Average of Multi-cap Category Average of Hybrid - Equity Category Average of MIP Category Note: Shown dates are SIP started dates. 19.58 15.32 9.50 26.65 20.48 9.11 0.01 1.91 5.05 7.79 8.76 8.44 8.56 9.95 7.59 30.87 26.21 13.64 Analyst: Dhuraivel Gunasekaran (Email: Dhuraivel.gunasekaran@hdfcsec.com) Source: NAVIndia & ACEMF. RETAIL RESEARCH Fax: (022) 3075 3435 Corporate Office: HDFC Securities Limited, I Think Techno Campus, Building –B, ”Alpha”, Office Floor 8, Near Kanjurmarg Station, Opp. Crompton Greaves, Kanjurmarg (East), Mumbai 400 042 Fax: (022) 30753435 Website: www.hdfcsec.com RBI & AMC Sites Disclaimer: Mutual Funds investments are subject to risk. Past performance is no guarantee for future performance. This document has been prepared by HDFC Securities Limited and is meant for sole use by the recipient and not for circulation. This document is not to be reported or copied or made available to others. It should not be considered to be taken as an offer to sell or a solicitation to buy any security. The information contained herein is from sources believed reliable. We do not represent that it is accurate or complete and it should not be relied upon as such. We may have from time to time positions or options on, and buy and sell securities referred to herein. We may from time to time solicit from, or perform investment banking, or other services for, any company mentioned in this document. This report is intended for non-Institutional Clients. This report has been prepared by the Retail Research team of HDFC Securities Ltd. The views, opinions, estimates, ratings, target price, entry prices and/or other parameters mentioned in this document may or may not match or may be contrary with those of the other Research teams (Institutional, PCG) of HDFC Securities Ltd. RETAIL RESEARCH