Download

1 / 14

140 likes | 276 Vues

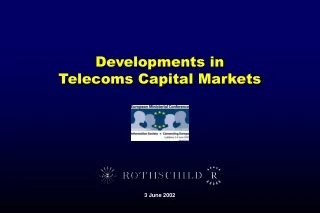

Developments in Telecoms Capital Markets. 3 June 2002. Contents. What happened? What was the role of Government and regulator? What are investor attitudes to telecom stocks now? How should Government and regulators react?. 260. 240. 220. 200. 180. 160. 140. 120. 100. 80. 60. 40.

E N D

Developments in Telecoms Capital Markets 3 June 2002

Contents • What happened? • What was the role of Government and regulator? • What are investor attitudes to telecom stocks now? • How should Government and regulators react?

260 240 220 200 180 160 140 120 100 80 60 40 1999 2000 2001 2002 Europe-DS Telecom, Media, IT - Price index Europe-DS market - price index Europe-DS Telecom,Wireless - price index What happened? 1.1 European TMT sector 1999-2002 ytd European performance Source: Datastream

1.2 TMT Incumbents in CEE 1999-2002 ytd CEE operators

1.3 Equity and equity linked issuance 1999 – 2002 ytd European telco sector equity issuance European telco sector equity linked issuance

1.3 Capital markets highlights • European DS Telecoms, Media and IT Index is • >70% lower than June 2000 • >50% lower than 2001 high • >25% lower than 2002 high • CEE Values are lower…

Capital markets highlights • Fixed: 4.5x EBITDA nowvs nearly 4x Revenues then • Mobile: 6-7x EBITDA now(– fixed line valuations at peak) • Issues by BT and KPN account for 70% (€15bn) of European equities issuance in the last 12 months • Convertible/exchangeable issuance rose in 2001 in response to low prices and interest rates and high volatility Valuations are lower… ˆ New issuance is down…

Capital markets highlights • Further growth possible towards European levels BUT • Cannibalisation of fixed revenues in voice • Ceiling of 2.5% mobile spend/GDP • Concerns about 3G • Disappointing volumes Mobile exceeded expect-ations… until 2001 Data, broadband…

350 300 250 200 150 100 50 1997 1998 1999 2000 2001 2002 BT GROUP In a Nutshell - 1 Source: Bloomberg

BT Group Vodafone Group In a Nutshell - 2 800 700 600 500 400 300 200 100 0 1997 1998 1999 2000 2001 2002 Source: Bloomberg

6000 5000 4000 3000 2000 1000 0 1997 1998 1999 2000 2001 2002 BT Group Vodafone Group Colt Telecom In a Nutshell - 3 Source: Bloomberg

What was the role of Government and the regulator? Faster liberalisation Slower liberalisation • Consumer choice/business needs • New entrant push • EU accession • FCC pressure on settlement rates • Network development obligations • Digitalisation/broadband vision • Tariff rebalancing/price control • Labour issues • Privatisation proceeds Most CEE Governments/regulators favoured infrastructure based competition model

What are investor attitudes to telecoms stocks now? Institutional investors Strategic investors Private equity • Wary, especially of 3G cost/benefits • Visibility/momentum of earnings… • Driving dividend • High liquidity/free float requirements • Where are they now? • Highly geared • 3G write offs • Strategies under attack • Beginning to play • But still relatively few in CEE • High rates of return • Stability of cashflow The telco reinvented as a utility?

How should Governments / regulators react? • Infrastructure as a utility • Services based competition over incumbent network • Interconnection • Carrier (pre) selection • Local loop unbundling • Number portability • “Second National Operators” rarely succeed • MVNO for 3G? • Regulatory (transparent) bite • Temper price / other ambitions