Recent Trends in State Audits of Local Governments: Key Insights from the 2013 Conference

This document outlines the recent trends in state audits of local governments as discussed during the Washington Association of County Officials Annual Conference held on October 2, 2013. It highlights key issues identified in audits, including cash receipting and federal compliance, the importance of internal controls, and the implications of timely audits for bond ratings. The report emphasizes the necessity of online annual report filings and the associated advantages, including increased accuracy and timeliness. Training initiatives for local governments are also detailed to enhance compliance and reporting standards.

Recent Trends in State Audits of Local Governments: Key Insights from the 2013 Conference

E N D

Presentation Transcript

Recent Trends in State Audits of Local GovernmentsWashington Association of County OfficialsAnnual ConferenceOctober 2, 2013

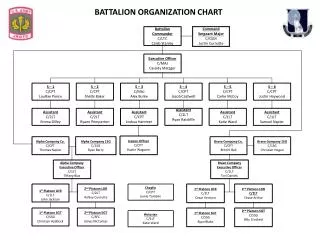

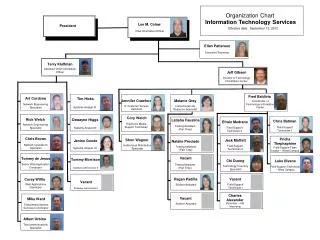

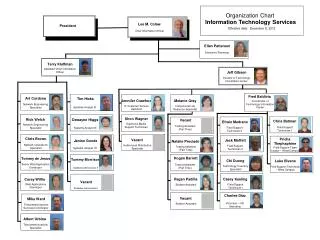

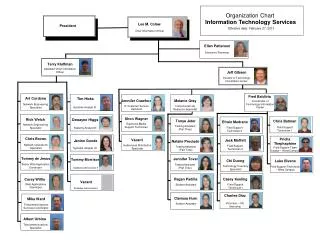

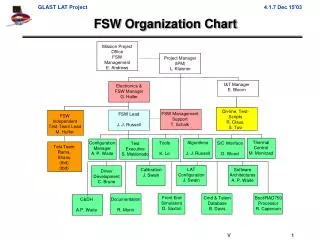

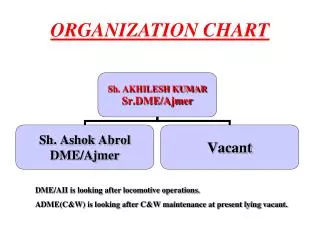

Organization chart Troy KelleyState Auditor Doug CochranChief of Staff VacantDirector of Local Audit Chuck PfeilDirector of Performance Audit Jan Jutte Deputy Director of Local Audit Kelly Collins Deputy Director of Local Audit Sadie Armijo Deputy Director of Local Audit Vacant Deputy Director of State Audit David Dean Deputy Director of Performance Audit

Audit issues 2011 2012 • Accountability – 23 • Financial – 2 • Single - 0 • Accountability – 32 • Financial – 6 • Single - 1 25 Management Letters 39 Management Letters 51 Findings 44 Findings • Accountability – 13 • Financial – 8 • Single - 30 • Accountability – 8 • Financial – 11 • Single - 25 Total Exit Items – 226 Total Issues Reported – 309 Total Exit Items – 165 Total Issues Reported - 241

Audit issues What are the current issues? • Cash Receipting • Federal Compliance • Financial Reporting What causes these audit issues? • Lack of Internal Controls • Ineffective or Inadequate Internal Controls

Change in reporting National audit standards requires two opinions • Opinion non-GAAP basis • Opinion on GAAP basis Outreach • Mailing to management and elected officials • Conversations with bond raters • Newsletters

Potential for municipal bond downgrades • Early 2013, Moody’s Investor Service placed the ratings of 40 U.S Public Finance Local Government obligors under review, affecting approximately $354 million of outstanding debt. • The lack of sufficient, current financial information prompted the review. • A total of nine Washington State municipalities were impacted by this review.

Audit requirements • When local governments issue bonds there are commitments made for timely audited financial statements. • Bond issuers who fail to have timely audits risk a withdrawal or downgrade of their bond rating which can have: • Severe implications to the value of bonds for bondholders. • Significant ramifications to municipalities as they seek to obtain cost effective capital in the markets in the future.

Research your bond covenants • Local governments that currently have bond obligations should research their audit requirements for meeting bond covenants. • Most issuers of debt must file their audits within nine months of year-end for municipal bonds. • If a more frequent financial statement audit is required, contact your local SAO audit team to schedule an audit to meet the requirement.

Big picture cost savings • The better the bond rating, the lower the potential interest rate on bonds or debt. • A half-a-point of interest can mean hundreds of thousands of dollars in property tax savings over the long haul. • Studies have indicated that audited entities enjoy a lower interest rate of on average 25 to 64 basis points, compared to unaudited entities, confirming that financial statement verification influences lenders’ pricing decisions.

Online annual report filing strategy State Auditor’s Office Online Filing Goal • 2016- All local governments file online (2015 annual reports) Actual Results Annual Reports Filed Online • 2011-46% • 2012-62% (total 1544) Projected Goal • 2013-75% • 2014-85% • 2015-100%

Advantages of online filing • Local governments assured using current requirements • Local governments filing only necessary schedules • Local auditors easy access to annual reports • Increases accuracy of annual reports (built-in edits) • Instantly creates financial statements for cash basis local governments • Increases timeliness of annual report filings

How will SAO reach goal? • Increase SAO staff support • Training • Free training for local governments with annual revenues less than $300,000 • Continue WFOA training • Enhance online filing system • Additional tools (video tutorials) • Open navigation (no longer sequential steps required) • Continue to Monitor Feedback

Training objectives and format Objectives of four hour free training • Local governments will obtain skills to file online • Local governments less reliant on counties • Local governments will have SAO contacts for future assistance What is format of training? • Formal training combined with hands-on assistance • SAO will travel to all counties in February /March 2014 • Local governments will bring old or current annual reports • Access issues to system will be taken care of prior to training

How can counties help SAO meet goal? • Host the four hour free trainings • Encourage participation (SAO will provide each county with list of eligible local governments) • Register participants • Help make the training successful by: • Provide example county reports at training • Provide space and other logistics for training

Training plan • SAO will email all County Auditors next week to provide a training coordinator to SAO by November 1, 2013. • Coordinator Responsibilities • Work with SAO to schedule training (during November) • Register local governments for training (during December) • Host the training • SAO will notify all eligible local governments to register for training by December 31, 2013. • SAO will post in December on SAO website training dates and registration information. • February and March 2014: SAO delivers training!!!

New online filing requirements • Applicable to 2013 fiscal year reporting. • Local governments will be required to update incorrect financial data already submitted to the SAO. • Correction of errors found prior and during audit.

Cyber Security Do a self-assessment • Identify sensitive data • Identify users and processes with access • Identify location and protection of data Article in Summer Audit Connection

Current Issue Third party cash receipting • Identifying 3rd party receipting activities and vendors • Review vendor contracts and controls • Confirming timeliness of deposit • Educating entities on the risk • PDPC/banking issue

Lodging tax July 1, 2013 changes include: • Cannot pay for capital expenditures for tourism-related facilities owned by a nonprofit. • If over 5000 population: • Applications must be submitted to advisory committee • Advisory committee submits a list of acceptable projects and amounts to governing body • Governing body can only select from that list The Joint Legislative Audit & Review Committee (JLARC) has developed draft guidance for reporting use of lodging tax revenue. This guidance can be found on JLARC’s website: http://www.leg.wa.gov/JLARC/LodgingTax/default.htm

Local Government Performance Center Improved government performance: A shared goal The Local Government Performance Center within the State Auditor’s Office offers tools and training to help local leaders who want their governments to work better, cost less, and improve the value of their services to citizens. • An online resource center with tools and examples. • Training on how to improve government services. • Customized on-site training sessions (on request and within available resources). Our goal: better results for citizens and customers at lower cost to government and taxpayers

Why the State Auditor’s Office? • As performance auditors, we conduct research and use tools that, if shared more broadly, could help many local governments reduce their costs and improve performance. • Sometimes an independent perspective and expertise from outside the organization can help you see and do things differently. • We believe that by sharing what we know through this project, we can reach more governments faster and cheaper than by doing one local government audit at a time.

Where to find us on the website www.sao.wa.gov/performancecenter

Five examples of what we’re doing 1) Turning a completed audit into a management tool • Sharing lessons learned from a recent state audit in a checklist format helps governments save money on cell phone costs. 2) Citizen engagement tools and resources • Citizen survey project with Walla Walla, creating a model. • Training on how to engage citizens and increase transparency. 3) Performance measure training and assessments • Training on performance measures plus auditor assessments of how local governments use performance data and ways they can improve. 4) Use information from local financial audits • Assess financial condition of local governments state-wide. • Create tools from common audit and findings management letters. 5) Demystifying tools like “Lean Management” • Training plus creating a peer-support network to help governments learn and use process improvement methods to develop faster, cheaper delivery systems. • “Lean Academy” with Clark, Island, Whatcom, and Douglas Counties.

Example 1: Translating auditor insights into “plain talk” Can your jurisdiction save money on cell phones? Start by asking these questions: How many phones are we paying for? How much are we paying for these phones? Why do we need the phones? Do the phones justify the cost? Do employees need a land line and a cell? How many different phones or plans can our employees choose from? What are the key differences between the available plans? Do we need them all? How many minutes are we actually using? Would other plans better fit our current use patterns? Are there any phones we aren’t using very much? Why? Should these phones be turned in? Are there any suspiciously high use patterns? Can our employees use their personal phones for their work? Are stipends an option? Is our demand changing? Has the number or type of devices or their use increased or decreased over time?How can we explain the change? Do we need a new plan to better fit our needs? “Every dollar saved now is a dollar that can be used for more important priorities.” The November 2011 State Auditor’s Office report.

Example 2: Helping governments engage citizens • We provide tools and training that help cities and other organizations communicate with their residents. • Training on citizen engagement strategies: • Citizen-driven prioritization of resource allocation and process improvement efforts help governments focus on “what matters most.” • Citizen surveys: • Helping the Cities of Walla Walla and Covington develop and analyze a citizen survey. • Developing a survey template other governments can use. • Guidance using the results to inform decisions.

Example 2: Engaging citizens in setting priorities City of Walla Walla services: Importance by performance Source: Elway Research, Inc.

Example 3: Performance measure assessments • Cities and counties have asked the Local Government Performance Center to review how they use performance measures and offer guidance. • We provide on-site training to help managers and analysts improve performance-based strategies. • Recently completed assessments for the City of DuPont, the Thurston County Sheriff’s Office, Pierce County, and Cowlitz County Sheriff’s Office are available on our website. • Currently assessing measures for the SCORE facility – report to be complete in October.

Example 4: Use information from financial audits Indicators of declining financial condition Reported by type since 2006 .

Example 4: Use information from financial audits Indicators of declining financial condition Reported by type since 2006 Most governments with declining condition have more than one area of concern; the average government having 3 indicators. 42% had indicators reported in multiple years. 24% had just one indicator. Source: State Auditor’s Office local government audits 2006-2011.

Example 4: Use information from financial audits Number of governments with declining financial condition by type Source: State Auditor’s Office local government audits 2006-2011.

Example 4: Use information from financial audits Source: State Auditor’s Office local government audits 2006-2011.

Example 4: Use information from local audits What’s next: • Update report • New resources • Tools & templates • Technical assistance

Example 5: Using Lean Principles “Lean Thinking” was a term coined by James Womack to describe the Toyota Production System MIT researchers “discovered” in the 1980’s. Lean is a set of concepts, principles, and tools used to create and deliver the most value from the customer’s perspective while consuming the fewest resources, by engaging employees in continuous problem solving.

Example 5: Using Lean Principles Inspiration from Kitsap County Before

Example 5: Using Lean Principles Inspiration from Kitsap County After

Example 5: Using Lean Principles • Clark, Douglas, Island, and Whatcom Counties have now completed our “Lean Academy” to help streamline their permitting offices. • Examples of successes: • Whatcom County; Residential permit; went from and average of 31 days to an average of 9 days; 70% improvement. • Island County; Shoreline exemption permit; 90 days to 45 days; 50% improvement. • Clark County: Single Family Residential permit, went from 45 days to 13 days; 70% improvement. • Case studies, videos, and “how-to” tools are posted on our website. More training will be offered this year.

Example 5: Using Lean Principles Find the application at: www.sao.wa.gov/performancecenter “Lean Academy” tab

New roles bring new challenges • Maintaining our independence: We have developed an extensive intake procedure that evaluates any potential compromise of our independence. • We are scrupulously clear with local governments that we don’t do the work for them – we provide tools, training and technical assistance. • Auditors who work on assistance engagements do not audit those entities; but we do share information with the audit teams and they share information with us.

What does it cost? • The Center is funded through the state performance audit program, which was established in the Auditor’s Office following voters’ approval of Initiative 900 in 2005. • A small fraction of the performance audit budget is dedicated to this effort. • There is no charge to governments.

Auditor’s Office Contacts Troy Kelley State Auditor (360) 902-0360 Auditor@sao.wa.gov Sadie Armijo Deputy Director (360) 676-2165, Ext. 108 Sadie.Armijo@sao.wa.gov Sheri Sawyer Assistant Director (360) 725-9745 Sheri.Sawyer@sao.wa.gov Jan Jutte, CPA, CGFM Deputy Director (360) 902-0363 Jan.Jutte@sao.wa.gov Kelly Collins, CPA Deputy Director (360) 725-5359 Kelly.Collins@sao.wa.gov