Download

1 / 27

270 likes | 361 Vues

Learn about the average-cost, FIFO, and LIFO methods to compute inventory value. Understand the implications of having too much or too little stock. Practice calculating inventory values with practical examples.

E N D

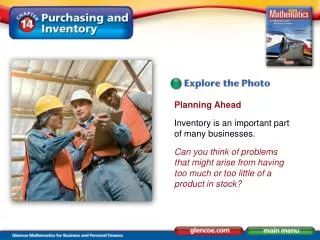

Planning Ahead Inventory is an important part of many businesses. Can you think of problems that might arise from having too much or too little of a product in stock?

Lesson Objective Us the average-cost, FIFO, and LIFO methods to compute inventory value. Content Vocabulary average-cost method A way of valuing inventory based on the average cost of goods received by a business. first in, first out (FIFO) A method for managing physical flow of inventory that assumes that the oldest inventory is sold first. last in, first out (LIFO) A method for managing physical flow of inventory that assumes that the most recently purchased merchandise is the first to be sold. • average-cost method • first in, first out (FIFO) • last in, first out (LIFO)

Example 1 Wholesale Paint Supply is valuing its inventory of white latex paint. On March 1, Wholesale Paint Supply had 88 gallons of white latex paint on hand. What is the value of the inventory on March 1?

Example 1 Answer: Step 1 Find the average cost per unit. Total Cost of Units ÷ Number Received $542 ÷ 240 = $2.2583 or $2.26

Example 1 Answer: Step 2 Find the inventory value. Average Cost per Unit ×Number on Hand $2.26 ×88 = $198.88

Key Words to Know first in, first out (p. 590) A method of valuing inventory that assumes the first items received are the first items shipped out. Called FIFO for short.

Example 2 For Wholesale Point Supply in Example 1, find the cost of goods and the value of inventory using the FIFO method. Find the cost of goods sold using the FIFO method.

Example 2 Answer: Step 1 Find the items purchased. (Note: This assumes the first items purchased are the items sold first.) a. Read the table in Example 1. You’ll see that 240 units were received. Refer to Step 2 in Example 1. There were 88 items on hand. 240 – 88 = 152 units sold

Example 2 Answer: Step 1(cont.) b. Under the FIFO method, the 152 units sold were assumed as follows: *152 (units sold) – 80 – 40 = 32

Example 2 Answer: Step 1(cont.) c. Add the total cost of the units received. $172.00 + $90.00 + $73.60 = $335.60 (Note: You do not include in this step the units received on Feb. 22, because those units will help you calculate the value of the inventory, as you’ll see in Step 2.)

Example 2 Answer: Step 2 Find the value of the inventory using FIFO. (Note: There are 88 units on hand—refer to Step 2 in Example 1.) a. The items remaining were:

Example 2 Answer: Step 2 (cont.) **If you go back to Example 1, Step 2, you’ll notice that on Feb. 15, 80 units were received. Out of that 80, only 32 were purchased. Therefore, 88 – 32 = 48 items remaining in inventory.

Example 2 Answer: Step 2 b. Find the value of the ending inventory. (Note: The cost of the ending inventory is computed by using the cost of the most recent units received.) $110.40 + $96.00 = $206.40

Key Words to Know last in, first out (LIFO) (p. 591) A method of valuing inventory that assumes the last items received are the first items shipped out. Called LIFO for short.

Example 3 For Wholesale Point Supply in Example 1, find the cost of goods and the value of inventory using the LIFO method.

Example 3 Answer: Step 1 Find the items purchased. a. Read the table in Example 1. You’ll see that 240 units were received. Refer to Step 2 in Example 1. There were 88 items on hand. 240 – 88 = 152 units sold

Example 3 Answer: Step 1(cont.) b. Under the LIFO method, the 152 units sold were assumed as follows: *152 units sold – 80 – 40 = 32 units received

Example 3 Answer: Step 1(cont.) c. Add the total cost of the units received. $96.00 + $184.00 + $72.00 = $352.00

Example 3 Answer: Step 2 Find the value of the inventory using LIFO. (Note: There are 88 units on hand—refer to Step 2 in Example 1.) a. The items remaining were:

Example 3 Answer: Step 2 (cont.) **If you go back to Example 1, Step 2, you’ll notice that 88 units were on hand. Of that 88 on hand, on Feb. 1, 80 units were sold. Therefore, 88 – 80 = 8 units received.

Example 3 Answer: Step 2 b. Find the value of the ending inventory. $172.00 + $18.00 = $190.00

Practice 1 Find the average cost per unit and the inventory value. Total cost of units: $509.78 Number received: 142 Number on hand: 86

Practice 1 Answer Average cost per unit: $3.59 Inventory value: $308.74

Practice 2 Find the average cost per unit and the inventory value. Total cost of units: $1,316.79 Number received: 187 Number on hand: 123

Practice 2 Answer Average cost per unit: $7.04 Inventory value: $865.92