Download

1 / 29

290 likes | 994 Vues

Uncovered interest parity and deviations from uncovered interest parity. The Academy of Economic Studies, Doctoral School of Finance and Banking. MSc student, Costescu Silvia Mihaela. Dissertation paper outline.

E N D

Uncovered interest parity and deviations from uncovered interest parity The Academy of Economic Studies,Doctoral School of Finance and Banking MSc student, Costescu Silvia Mihaela

Dissertation paper outline • The importance of uncovered interest parity • The aims of the paper • Literature review • The model • The data • Empirical analysis • Concluding remarks • References

The importance of the uncovered interest parity • UIP has an analytical importance and appears as a key behavioral relationship in virtually all of the prominent models of exchange rate determination. • UIP is a key feature of linearized open-economy models, it reflects the market’s expectations of exchange rate changes and represents the starting point for any analysis which depends on future exchange rate values. • Because there are reasons to believe that UIP will not hold precisely, an investor must be able to identify the source of deviation and respond accordingly.

The aims of the paper • I propose to test the UIP hypothesis for Czech Republic, Cyprus, Poland, Romania and in Panel over the sample period March 1999 – November 2007. • If this hypothesis does not hold, I identify and calculate the deviations from uncovered interest parity. • I identify which is the main component of UIP deviations for every country. • I will try to explain why the deviations occur.

Literature review • A lot of paper, back to Fama(1984)test for uncovered interest parity at distant horizons and evidence that interest rate differentials tends to be negatively, rather than positively, correlated with future currency movements, thereby wrongly predicting their direction. • Flood and Rose(2001) find considerably heterogeneity across countries and detect signs that uncovered interest parity at the short horizon holds better in crisis countries, where both exchange and interest rates display high volatility. • Cochrane(1999), Alexius(2001), Chinn and Meredith(2005), Chinn(2006) and Zhang(2006) suggest that uncovered interest parity tends to hold for financial instruments of longer maturities. • For several industrialized countries, Gokey(1994) finds that movements in the real exchange rate are more important than those in the risk premium to explain the deviations from UIP.

The model In the condition of risk free arbitrage, the ratio of the forward to the spot exchange rate is equal the interest differential between two countries. Covered Interest Parity (CIP) can be expressed as: (1) All variables are expressed in logarithms, where – nominal spot exchange rate at time t expressed as the price, in “home-country” monetary units, of foreign exchange (EUR) ; – forward rate of s for a contract expiring k periods in the future; – k period nominal interest rate in home country; – k period nominal interest rate in foreign country (EA);

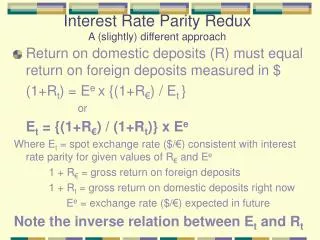

The model If the investors are risk averse, the forward rate can differ from the expected future spot rate by a risk premium. Uncovered interest parity says that changes in the expected exchange rate equals the current interest differential, if the investors are risk-neutral: (2) Where, is expected nominal spot exchange rate from period t to period t+k, expressed in logarithm

The data The source of data is Eurostat, The National Bank of Czech Republic, The National Bank of Cyprus, The National Bank of Poland and The National Bank of Romania database. The periods covered are: March1999- November 2007.Empirical analysis has been made using monthly data for: • The average nominal exchange rate, of four European Union currencies against the euro, namely the Czech koruna (CZK), the Cyprus pound (CYP), the Polish zloty (PLN) and the Romanian new leu (RON). Each exchange rate is quoted as number of national currency units per euro. • The average active money market interest rate used by banks for the Czech koruna (CZK), the Cyprus pound (CYP),the Polish zloty (PLN), the Romanian new leu (RON) and EUR operations using maturities of 3 and 6 month.

Empirical analysis I tested UIP equation, which is known as standard Fama(1984) regression: for Czech Republic, Cyprus, Poland, Romania and in Panel, in the assumption of rational expectations I test the properties of the regression variable and perform unit root tests (ADF and PP).

Unit-root test for exchange rate change (in log) Czech Republic Cyprus

Unit-root test for exchange rate change (in log) Poland Romania

Unit-root test for nominal interest rate differential (in log) - 3 monthmaturities Czech Republic Cyprus

Unit-root test for nominal interest rate differential (in log) - 3 monthmaturities Poland Romania

In line with Chinn and Meredith (2005) and Chinn (2006) I use GMM to correct the standard errors of the parameter estimates for MA serial correlation. Estimates of β The coefficient is negative and the hypothesis that β equal unity is strongly rejected. A negative β coefficient suggests that interest rates differentials explain future currency movements systematically in the “wrong” direction. This is a standard result in empirical literature of international finance and constitutes the “forward discount puzzle”.

Mean, variance and t-ratio for ex-post deviations from UIP3 month I test the deviations from UIP to see if it works. The ex-post deviations from UIP are: I perform unit root tests (ADF and PP) for UIP deviation to see whether it fluctuates around the mean or drifts boundlessly.

Unit-root test for ex-post UIP deviation- 3 month maturities Czech Republic Cyprus

Unit-root test for ex-post UIP deviation- 3 month maturities Poland Romania

Ex-post deviations from UIP I can conclude that UIP works only for Czech Republic, because is the only one who has the mean of the UIP deviation not statistically different from zero, the t-ratio very low and less than unity and both ADF and PP tests suggest that ω is stationary. Similar results for 6 month horizon

Deviations from UIP Fama(1984) suggest that deviations from UIP represent either a risk premium ( as measured by the real interest differentials) or an unexpected change in the real exchange rate: The exchange rate growth can be written as: Where, is the matrix of variables known at or before time t, including inflation rate differential, nominal exchange rate changes and nominal interest rate differential and is vector of corresponding coefficients. I first estimate the equation with all the predictable variable, then I eliminate the variable that are not statistically significant (nominal interest rate differential for all the countries and nominal exchange rate changes for Cyprus), and I obtained:

The exchange rate growth equation Dependent Variable: DQT_CZECH Method: Least Squares Date: 07/07/08 Time: 22:18 Sample: 1999M03 2007M11 Included observations: 105

The exchange rate growth equation Dependent Variable: DQT_CYPRUS Method: Least Squares Date: 07/07/08 Time: 13:11 Sample: 1999M03 2007M11 Included observations: 105

The exchange rate growth equation Dependent Variable: DQT_POLAND Method: Least Squares Date: 07/07/08 Time: 22:23 Sample: 1999M03 2007M11 Included observations: 105

The exchange rate growth equation Dependent Variable: DQT_ROMANIA Method: Least SquaresDate: 07/07/08 Time: 22:24 Sample: 1999M03 2007M11 Included observations: 105

Deviations from UIP Tanner(1998) decomposes ex-post deviations from UIP into unanticipated and anticipated component of real exchange rate growth: (resid series for every above equations), (the difference between real exchange rate growth and resid series) The deviation from UIP can be written: ω = ρ + ε + θ Nothing that cov(ε,θ)=0, I can write the variance equation of ω as: var(ω)= var(ρ)+ var (ε) + var (θ) +2[ cov(ρ,ε)+ cov(ρ,θ)] This equation tell us how much of the variance in ω is due to changes in the real interest rate differential, anticipated changes in the real exchange rate and unanticipated real exchange rate growth, or the covariance between interest rate differential and every component of exchange rate growth.

Variance of deviations Variance and covariance for 3 months Variance and covariance as a fraction of var(ω) for 3 months

Variance of deviations Variance and covariance for 6 months Variance and covariance as a fraction of var(ω) for 6 months

Concluding remarks • In the covered period the results confirm the rejection of uncovered interest parity, for Czech Republic, Cyprus, Poland and Romania. • I calculate UIP deviations and found that for analyzed countries real interest differential is the main component of UIP deviations. The interest rate differential accounts for nearly 64%(Czech Republic), 77%(Cyprus), 85%(Poland), 91%(Romania) of deviations from UIP. • These results are in line with developing countries, and one explanation can be the variability of inflation in these countries, and the fact that the prices rise rapidly. • For Czech Republic and Cyprus I obtain the negative covariance between interest rate differential and unanticipated real exchange rate growth, implying that changes in the real interest differential will be offset to some degree by movements in real exchange rate growth, thus reducing the deviations from UIP.

Selected References • Alexius A(2001), “Uncovered Interest Parity Revised”, Review of International Economics”,9(3). • Cochrane, J (1999),”New Facts in Finance”, Economic Perspectives, Federal Reserve Bank of Chicago, XXIII(3). • Chaboud, A and J Wright(2005), : Uncovered Interest Parity: It works, but not for Long”, Journal of International Economics, 66 • Edison H. J. and Pauls B.D(1993) “A Re-Assessment of the Relationship Between Real Exchange Rates and Retal Interest Rates: 1974-1990”, Journal of Monetary Economics 31,165-187 • Engel, Charles (2000), „Comments on Obstfeld and Rogoff’s “The Six MajorPuzzles in International Macroeconomics: Is There a Common Cause?””, NBER working paper 7818 • Fama E. (1984), “Forward and Spot Exchange RateS”, Journal of Monetary Economics, 14. • Flood R. and A. Rose(2001)-“Uncovered Interest Parity in Crisis:The interest Rate Defense in the 1990s”, IMF Working Paper. No 01/207

Selected References • Froot K. And R. Thaler(1990), “Foreign exchange “, Journal of Economic Perspectives, 4 • Gorkey T. C.(1994), “What explains the risk premium in foreign exchange returns?” Journal of International Money and Finance13,6 • McCallum, Bennett T. (1992), „A Reconsideration of the Uncovered Interest ParityRelationship”, NBER working paper 4113 • MacDonald R.(1997)“What Determines Real Exchange Rates: The Long and Short of It, “ IMF Working Paper 97/21(Washington: International Monetary Fund) • Marston R(1997),” Tests of three parity conditions: distinguishing risk premia and systematic forecast errors”, Journal of International Money and Finance,16,2. • Menzie D. Chinn, Guy Meredith(2005),“ Testing uncovered interest parity at short and long horizons during the post-breton woods era” –NBER working paper 11077. • Meese R and Rogoff K (1988) “ What IS Real? The Exchange Rate-Interest Differential Relation Over the Modern Floating- Rate Period” Journal of Finance, Vol XLIII, No. 4, pp 933-948 • Tanner, Evan (1998), „Deviations From Uncovered Interest Parity: A Global Guide to Where the Action Is”, IMF working paper wp/98/117.