Download

1 / 11

110 likes | 242 Vues

http://www.infracapmlp.com - AMZA is the first actively-managed C-corporation MLP ETF and was issued in October 2014.

E N D

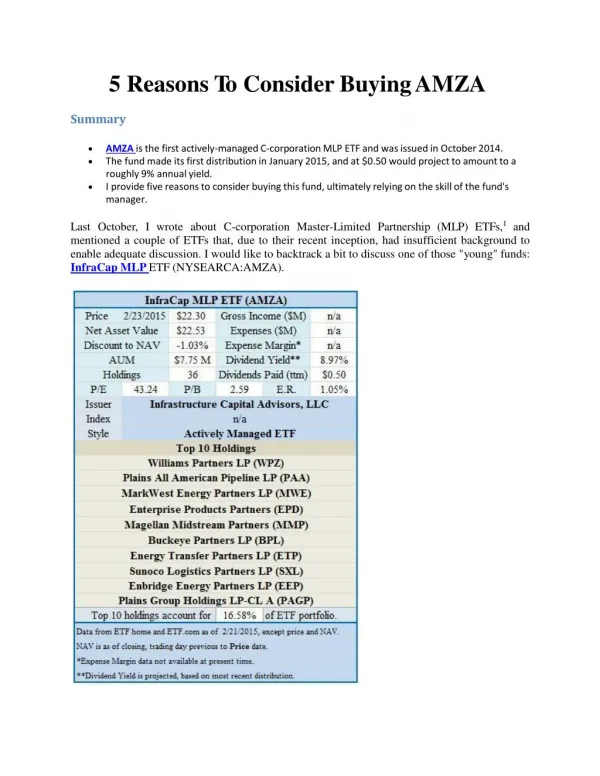

5 ReasonsTo ConsiderBuyingAMZA Summary • AMZAisthe firstactively-managed C-corporationMLPETFandwasissuedinOctober2014. • The fundmade itsfirstdistributionin January2015,andat $0.50 would project toamount toa roughly 9%annualyield. • I providefive reasonstoconsider buyingthis fund, ultimately relyingontheskill of the fund's manager. • Last October, I wrote about C-corporation Master-Limited Partnership (MLP) ETFs,1 and mentionedacoupleofETFsthat,duetotheirrecentinception,hadinsufficientbackgroundto enableadequatediscussion.Iwould liketo backtrackabit to discuss oneof those"young"funds: InfraCap MLPETF(NYSEARCA:AMZA).

AMZA began trading on 2 October, 2014; its start could not have been less propitious. The fund's holdings are all in theoil industry, and inOctober, the industrywas in the midst of amajor declinein oil prices. Thedrop in oil prices has dampened investor expectations. AMZA is a C-corporation ETF focusing on MLPs; it is also one of the approximately 125 actively-managedETFscurrentlyavailable.BothoftheseconsiderationsmeanthatAMZAis goingtohaveasubstantialexpenseburden:C-corporationsmustpaytaxesontheirincome,2and actively-managed fundsgenerallycost moreto operate.3 Thequestionthatconfrontsthepotentialinvestoriswhetheranactively-managedfund-anda tax-burdenedone,atthat-isworththeadditional expenses.Giventhatthe activeETF isgoingto havetopayoutmorethanthepassiveETF,andgiventhatthoseexpensesareultimatelytaken out of the moneys that would normally go to shareholders in the form of distributions, is the active fundgoingto payout betterthan apassivefund? Whileitisuptotheindividualinvestortodecidetheissueofwhatcountsas"better,"andwhile eachactiveETFisdifferent,IhavefiveconsiderationsthatapplytoAMZAthatmaymakeitan attractiveholding.Myresearchin,andunderstandingof,AMZAwasaided(andabetted)bya conversation withfund manager JayD. Hatfield,president andco-founderof Infrastructure Capital Advisors, LLC and co-founder and general partner of NGL Energy PartnersLP (NYSE:NGL).4 Forpurposesofexposition,IwillbecomparingAMZAtoapassiveC-corporationETF:ALPS AlerianMLP (NYSEARCA:AMLP).5

Responsibility forthe Actively-ManagedPortfolio The fund manager is the primary focus for an actively-managed ETF. In passive ETFs, the managementteamfollowsa"roadmap"laidoutforitbythefund'sindex;itmayhavemoreor lessleewayinchoosinghowtofollowthatroadmap,butthebasiccontentsoftheportfolioare set forit. The active managers, on the other hand, have the freedom to structure their fund's portfolio accordingtotheirbestjudgment-andthisisperhapsthemostcrucialelementfor thefund.Ifthe manager is out of step with the target sector/market, or if their skills are not adequately developed, the fund is likely to founder regardless of the manager's best intentions. Skilled managers,on theother hand,areable tobringtheirknowledge experienceto their fund; this maynotguaranteesuccess, but it at least makes successmorelikely. Thefirstconsideration,then,wouldreasonablybeAMZA'smanager:JayD.Hatfield.Alook at Mr. Hatfield's experienceshouldgive us an indication ofhis abilities:6

AsPresidentofICA,hemanagesfourotherfundsbesidesAMZA:InfrastructureMacroIncome Fund, LP; Infrastructure MLP Income Fund, LP; Infrastructure Long/Short Opportunity Fund, LP; andInfraCapReal EstateIncome Fund,LP • Servedas PortfolioManagerforS.A.C. CapitalAdvisors(nowPoint72Asset Management) • Was ManagingDirectorandHead of FixedIncomeResearch, ZimmerLucasPartners • HeadedGlobal UtilityInvestmentBankingatCIBC/Oppenheimer • Was PrincipalintheGlobalPower& UtilitiesInvestment BankingUnitatMorgan Stanley &Co. • Mr. Hatfieldseems to have experienceinportfoliomanagement,theenergy sector, alternative investment instruments, hedge funds; his involvement with NGL (which is included in AMZA'sportfolio)alsogiveshimdirectexperienceintheMLParea.Tomymind,thismakes him singularlyqualified to managethe AMZA portfolio in a hands-on fashion. • Flexibility InherentinActiveManagement • In principle, perhaps the major advantage AMZA (and any actively-managed ETF) has is flexibility - the abilityto be able to develop and modifythe fund's portfolio according to the manager'sperceptionofeconomicconditionsatthetime,ratherthaninaccordancewiththe structural dictates ofan index. • Anymarket-andparticularlytheoil/naturalgasmarket,oflate-isdynamic.Theactivefund makes it possible for the manager to adjust the fund's portfolio on the fly to accommodate changesinmarketconditions.InAMZA'scase,Mr.Hatfieldhasdoneseveralthingswiththe aim of outperformingthe"standard"MLP ETF, Alerian'sAMLP. • Acomparisonofthefunds'performancessinceAMZA'sinceptionispresentedinthefollowing chart:7

Thechart as shown points out two important things: • Both funds have significantly outperformed The United States Oil Fund ETF, LP • (NYSEARCA:USO),whichhas a focuson upstreamoilcompanies;and • AMZA underperforms AMLPby 142bps. • Asforthefirstpoint, whileUSOfocusesonupstreamoil,AMLP'sindex (AMZI) focuseson midstreamcompanieswhichtendtobelesssusceptibletothevolatilityofupstreamcompanies and whose profits are not strictly tied to the price of oil.8 Upstream concerns have been hit hardest bylastyear's drop in oil prices; midstream companies havebeen less affected. • Foritspart,AMZAalsofocusesitsholdingsinthemidstreamoilcompanies;infact,24ofits36 holdings are identical to those in AMLP/AMZI. However, the similarity ends there. AMLP's portfolio is dictated by AMZI, and AMZI weighs its holdings (which are chosen based on distribution) accordingtomarket capitalization. • AMZA,ontheotherhand,isweightedaccordingtoMr.Hatfield'sperceptionofeachholding's value to theportfolioas awhole; this points to thesecondconsideration:Inthe activelymanaged portfolio, assets can be assigned to a holding according to the manager's conception of the portfolioandtheexpectationsforeachparticularholdinginit.Specifically,in AMZA'scase, holdings areweightedaccordingto theirgrowth prospects.9

Beyondthe MLPs AMZItrackstheperformanceofMLPsonly,and-beingtiedtoitsindex-AMLPcountsamong itsholdings,24 MLPs.Thesemaybeamongthelargestmidstream MLPs,butAMLPholdsonly these, and onlyin proportions consistent with its index. InstructuringAMZA'sportfolio,Mr.Hatfieldaddeddepthtothe24basicMLPs byinvestingin companiesthatweregeneralpartnersinsomeofthoseMLPs(and,inafewcases,puttingmore weight on the general partner than on its MLP). In all, AMZA's portfolio has general-partner holdings in nine ofthe 24 MLPs in its portfolio. Hasthisstrategyworked?AsIpreparedthisarticle,Iconstructedaninformalback-testofthe AMZA portfolio (as weighted) to get an idea of how the portfolio's holdings would have performed over thepast 5years. This chartgivesthe results: Theportfolio,asawhole,wouldseemtohavedonequitewellalthoughthereisnoescapingthe 2014 downturn. IthenthoughttoexamineAMZA'shypotheticalperformanceinadifferentway:Comparethe portfolio as a whole to those holdings identical to AMLP (call this AMZI*), alongside the "extension"ofAMZA'sextra12holdings(callthisNon-AMZI*).Tocapthecomparisonoff,I would add AMLP bywayofcomparingthe five-year performanceof AMZIto AMZI*.10 Theresults:

PerhapsmostnotableisthedifferenceinperformancebetweenAMLP'suseofAMZIandthe differentlyweighted performanceofAMZA'sAMZI*.This could betaken to indicate that-over time-AMZAhasastronglikelihood of outperformingAMLPeven ifbothfunds were limited to the same 24 holdings, just by virtueof different weightings.11 Equallyimportant,however,istheeffectoftheaddedholdings(Non-AMZI*).Overthepastfive years,these12fundshaveshownmarkedvalueimprovement,andthatimprovementhashadthe effect of raising the performance of AMZA, as a whole, over the performance of its AMZI* based holdings. The improvement that only seems moderate compared to the dramatic improvementinNon-AMZI*canbeattributedtothefactthatAMZI*makesupnearly82%of assets compared to Non-AMZI*'s just-over 18%. Our third consideration, then, is that the added depth to AMZA's portfolio - a product of managerJayHatfield'sapproachtothefund-resultsinanimprovementinfundperformance that complements the improvements heintroducedwith his different weightingscheme. The Impacton Distributions WhiletheextendeddepthofAMZA'sholdingsseemstobodewellforitsfutureperformance, one can argue that it represents a setback to the fund's distributable income. The "basic" 24 holdingsaccountforanannualincomeforthefundof$396,289.69(ttm),foraneffectiveyield of4.58%.12 With the 12 added holdings, the income increases to $457,133.01 for an effective yield of 4.32%.13 Thismeansthat,afterprojectedexpenses,AMZAwouldbeofferingitsshareholdersa dividendyield ofapproximately$1.02 peryear forayield of about 4.58%.14

AMLPcurrentlyoffersayieldof6.71%.WhileAMZA'sperformancemightlooktobeagood bet, dropping 213bps in yield would seem to constitute a serious blow to the fund's active management. However,in January2015,AMZAdistributed$0.50individendstoshareholders(dividendsare tobepaidquarterly).Suchadistribution,ifannualized,wouldamounttoalmostdoublewhatI was able to identify from dividends paid by holdings and would constitute a yield of approximately9%. WhenIaskedifhethoughtthatkindofdividendwassustainable,Mr.Hatfieldansweredinthe affirmativeandwasquicktobringupanimportantaspectofhismanagement:Hehasinstituted theuseofcoveredcalloptionstoboostfundincome.Becauseofthistactic,AMZAwasableto increasedramaticallythedividenditwasabletooffer.Mr.Hatfieldexpressedconfidencethat theuseofcoveredcallswouldenabletheyieldtoremaininthevicinityof$2.00pershareper year.15 Our fourth consideration, then, is the freedom the active manager has of using various investmentinstrumentstoamplifythegains-and/oroffsetlosses-thefund'sbasicholdingsmay bringabout.Evenifitwereultimatelyabletogeneratehalfasmuchasitdidforthefirst-quarter dividends, AMZAwould still offer ayield larger than that ofAMLP.16 Constructive Use ofLeverage Debtisadouble-edgedsword,asIseeit.Itenablesonetoaccess resourcesonemightnotbe abletoaffordonone'sown;italsobecomesaburden,withinterestpaymentsandrepaymentof principle diminishingone'sultimate return.Debtis oneofthe things thatcan cool myenthusiasm foranyinvestment. Thatsaid,whenusedproperly,itcanhelpboostacompany's(orafund's)flexibility,enablingit to makequick decisions and moves that can enhanceoperations.If used judiciously, leveragecan bedeployed without engenderingthe fear of reduced futureincome. ETFsarerestrictedintheamountofleveragetheycanemploy;theInvestmentCompanyAct of 1940 sets a limit of one-third of its asset value as the most a fund can borrow. AMZA currently has borrowed 20%, the funds being used to implement the strategy and tactics Mr. Hatfielddeemsnecessary.Thisuseofleverage,hecontends,willenableAMZAtooutperform AMLP in thelongrun,17and is thefifth, and finalconsiderationwewill look at. Assessment Atthebeginningofthisdiscussion,Iclaimedthattherewere fivereasonstogiveanactively- managed fund such asAMZAserious consideration as a holding. Those considerations are: Theexperienceandskillofthefundmanager,Mr.JayD.Hatfield,atmakingdecisionsaboutthe fund's portfolioandoperations; the freedomsucha fund has intermsofvaryingtheweightingsof theholdings inits portfolio;

the ability to approach the portfolio's allocation strategy in ways not always accessible to a passivefund; theuseofvariedinstrumentalitiestoenhancetheperformanceofthefundbeyonditsholdings andtheir performance; and the flexibilitytoemploy leverage asdeemed necessary tooptimizeoperations. I cameawayfrom our conversation with thesensethat Mr. Hatfield hasa firm vision ofthe long- termstrategies that willbringaboutthe growth insharevalueand the growthindistributable incomethatcouldmakeAMZAavaluablepartofanyportfolio.Points 2-5aboveconstituteMr. Hatfield'sthreereasonswhyhebelievesAMZAwilloutperformAMLPbyatleast300bps,and as high as 500bps(helumps 2 and 3 together whileIseethemas two different strategies). Interms oftheaddedcosts,bothactivemanagementandoperationasaC-corporationentail,this isajudgmenteachindividualinvestorwillhavetoanswerforthemselves.Iftheuseofcovered callsisabletoconsistentlyboostdistributableincome,andiftheoilmarketmeetsMr.Hatfield's beliefthatoilwillbegoingformorethan$60.00perbarrelinthenextyear,18 bothyieldand performanceshouldgiveasubstantial total return forthe investor. I am not surethat the sharevalueofAMZA will appreciatequickly, as thegeneral oil situation is still somewhat unstable, and instability in price and supplies of oil will keep upstream and midstream stocks down. Further, with the Fed gettingcloser to committingto a rate hike, the impact of such ahike onMLPs, theirgeneral partners, andAMZA itself,will beindeterminate. IdoseeanupsidetoAMZA,andperhapsoneinkeepingwiththeroughly20%increaseMr. Hatfieldseesinthepriceofcrude.ThatAMZAisayoungfundmaymitigateitsperformance somewhat, but a consistentlyhigh distribution would offset anydownside. Longterm, Ithink this fund has excellent potential, that potential contingent on maintaining Mr. Hatfield (or a comparablyskilled replacement) as its manager. Disclaimers Thisarticleisforinformationaluseonly.Itisnotintendedasarecommendationorinducement to purchase or sell any financial instrument issued by or pertaining to any company or fund mentioned ordescribed herein. Alldatacontainedhereinisaccuratetothebestofmyabilitytoascertain,andisdrawnfromthe Company's published documents to the extent possible. All tables, charts and graphs are producedbymeusingdataacquiredfrompertinentfundinformation;historicalpricedatafrom Yahoo!Finance. Data from anyother sources (if used)is cited as such. Allopinionscontainedhereinaremineunlessotherwiseindicated.Theopinionsofothersthat maybeincluded areidentified as such and do notnecessarilyreflect myown views. Beforeinvesting,readersareremindedthattheyareresponsibleforperformingtheirowndue diligence;theyarealsoremindedthatitispossibletolosepartoralloftheirinvestedmoney. Pleaseinvest carefully.

1 "C-Corporation MLP ETFs:Why Wait?" 2 For a discussion of the tax burden assumed by the C-corporation ETF refer to the early portion of the article noted in #1, above. 3 Keepinmindthatthepassivefundis"managed"onaquarterlybasis,usually;anactivefund, on the other hand, can engage its management team as often as deemed necessary. Further, rather than following an index, the active fund management develops its own, proprietary, method of portfolio management. This "extra"engagement of managementcomes at a price. 4 JayD. Hatfield and Iengaged in a phone interview on February 18,2015. All references to Mr. Hatfield refer to that interview. I thank Jayfor taking thetimeto talk withme. 5 AMLPwasconsideredthesuperiorfundofthoseconsideredintheearlierarticle(#1,above). The data in this table is updated from that in the earlier article, using data from the Annual ReportofNovember2014.Inparticular,AMLP'sE.R.iscitedasbeing8.56%whileIwasable to calculate an E.R. of 5.09% based on the data provided in the recent AR. Any error in calculationismine,andisregretted.Forreasonsthatwillbeclearasthediscussionprogresses, Mr. Hatfield encouragedthe comparison ofAMZAto AMLP's index, AMZI. 6 Information culled fromInfrastructure Capital Advisors'biography, viewablehere. 7 United States Oil FundLPis included to provide comparison to near-month crudeoil futures. 8 Upstream companies are involved in exploration, drilling and extraction. Midstream companies are focused on the transportation, processing and storageof oil. 9 Per phone conversation, #4 above. 10 Inprinciple,thispitstwoversionsofAMZIagainsteachother.Thedifferencebetweenthetwo would (again, in principle) be the different weighting systems used: AMZI's cap-weighted schemeto AMZI*'s "prospect-weighted"scheme. 11 Of course, the standard disclaimer applies: past performance does not imply future performance. 12That is, the yield it realizes from its holdings. 13 Again,theyieldAMZArealizesfromitsholdings.Bythemselves,the12additionalholdings realizean incomeof $60,843.33, amounting to a yield of 3.16% 14 ThesefiguresarebasedonthestatedE.R.of1.05%subtractedfromprojectedincome,then dividedamong shares outstanding.AMZA currentlyhas 350,000 shares outstanding. Thereadershouldrealizethatthesefiguresrepresentestimatesonmypartbasedonavailable data, and do not claim to berepresentativeof thefund's actual income.

15 Perphoneconversation,#4above.Itisworthnotingthatcoveredcallshavethepotentialto bring about costlylosses, as well as substantial gains. 16 Itshouldbepointedoutthat,asIresearcheddividendpayoutsfortheMLPsheldbyAMZA, nearlyallofthemshowedgradual,consistent,increasesindistributionsasthepast12months played out. 17 Per phone conversation, #4 above. According to Mr. Hatfield, AMLP is leveraged to only 10%. 18 Per phone conversation, #4 above.