Download

1 / 49

490 likes | 628 Vues

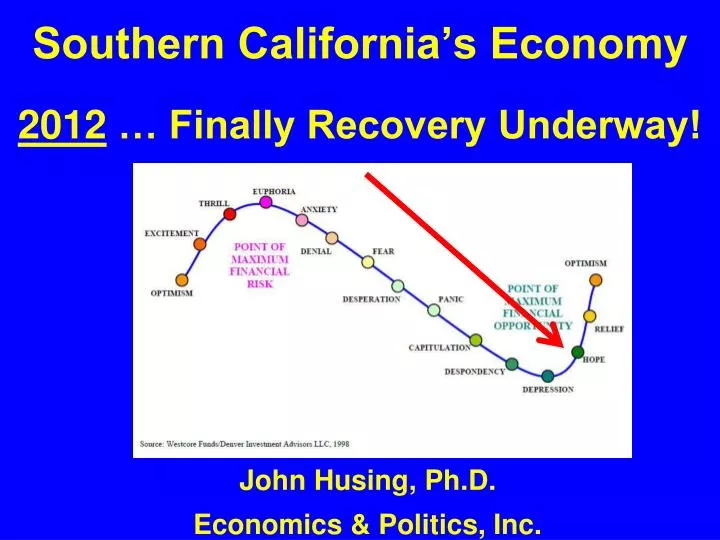

2012 … Finally Recovery Underway!. Southern California’s Economy. John Husing, Ph.D. Economics & Politics, Inc. After Losing 8.74 Million Jobs … U.S. Job Creation Is Crawling Back. 30% of Jobs Regained. Pattern of Likely Recovery. x. x. . U. V. So. California Job Growth/Destruction.

E N D

2012 … Finally Recovery Underway! Southern California’s Economy John Husing, Ph.D. Economics & Politics, Inc.

After Losing 8.74 Million Jobs …U.S. Job Creation Is Crawling Back 30% of Jobs Regained

Pattern of Likely Recovery x x U V

Inland Empire Job Growth/Destruction Wage & Salary Job Creation/Destruction Inland Empire, 2007-2011 30,000 20,000 10,000 0 (10,000) (20,000) (30,000) (40,000) (50,000) (60,000) (70,000) (80,000) (90,000) (100,000) (110,000) 2007 2008 2009 2010 2011 2012 Source: CA Employment Development Department

Job Growth Comparison: November Average Job Change, California Markets California Markets, November, 2010-2011 75,000 26,600 19,500 13,100 12,600 1,800 1,400 San Diego Co. Inland Empire Orange Co. Los Angeles Co. Ventura Co. Imperial Co. So. California Source: CA Employment Development Department

Still Tough Unemployment Rate U.S. Unadjusted 8.2%

Industrial Vacancy Rate Declining Again! 2005/2006 2009 2011 Inland Empire 2.7% 11.9% 6.8% Orange Co. 5.4% 7.0% 5.3% L.A. Co. 2.1% 3.4% 3.1% San Diego 6.0% 12.0% 10.7% 500,000 sq. ft. + Facilities … Inland Empire Vacancy = 0.0%

Quarterly Industrial Absorption, 1991-2011 20 million Sq.Ft.

Change In Container Flows Imported & Exported Container Volume, 2000-2011e Ports of Los Angeles & Long Beach (mil. teus) 8.2 8.0 Import Export 7.2 7.2 6.9 6.9 6.8 15.3% 6.0 6.0 5.7 5.0 4.8 3.3 3.1 3.1 2.8 2.7 2.3 2.1 1.8 1.7 1.6 1.6 1.6 -25.4% 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011e Source: Port Import Export Reporting Service (PIERS), collected from Vessel

2. Ports On West Coast Nearest Asia Los Angeles Long Beach

3. Deep Water Ports As Ships Draw Over 50 feet of Water 8,000-Container Post-Panamax Ships

International Trade Dollar Down: U.S. Goods Cheaper 112.2 -35.1% 84.0 2002 $180 2012 $117 2002 $1,500 2012 $2,027 72.8

Export Container Volume 2011 YTD 6.8% All-TimeRecord

Blue Collar Job Losses Have Ended or Are Close to Ending Blue Collar Employment Change Southern California, 1990-2011e 75,000 Manufacturing LOGISTICS Construction 50,000 25,000 0 (25,000) (50,000) (75,000) (100,000) 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011e Source: CA Employment Development Department

Why Blue Collar Jobs Important Educational Levels, Adults 25 & Over Southern California Counties, 2010 High School or Less Percent Bachelors or Higher 58.4% 48.5% 46.2% 44.6% 41.9% 36.7% 36.5% 34.6% 34.0% 33.7% 30.8% 29.2% 29.0% 20.3% 18.6% 13.2% Imperial San Bernardino Riverside Los Angeles So. California Ventura Orange San Diego Source: 2010 Census

Policy Conflict: Environment vs. Blue Collar Jobs

Public Health Blue Collar Sectors Bring Rising Asthma & CancerRisk From Airborne Toxics

California Solution Single Issue Regulatory Agencies & Processes CA Air Resources Board South Coast Air Quality Management District CA Environmental Protection Agency CA Water Resources Control Board CEQA & More

Two Results 1. Air Quality Is Improving

2. Downward Pressure On Blue Collar Jobs Blue CollarWork Is Much of Our Workforce’s Best Chance To Reach The Middle Class

Few Training Barriers To Beginning Employment Mining ($65,268) Blue Collar Wholesale Trade ($51,156) Blue Collar Manufacturing ($47,933) Blue Collar Logistics ($45,851) Blue Collar Construction ($41,076) Blue Collar Gaming ($37,827) Retail Trade ($28,824) Agriculture ($24,552) Hotel/Motel ($16,026) Eating & Drinking ($16,026) Alternative Jobs to Blue Collar

Results Of Job Suppression • Unemployment Higher Than It Needs To Be • Underemployment A Constant Difficulty • Lack of Access to Jobs Leading to the Middle Class • Health Issues of Poverty • Divorce • Spousal Abuse • Drug & Alcohol Abuse • Suicide • Lack of Timely Medical Care Public Health Issues!

Public Policy Dilemma Lack of Blue Collar Jobs & Poverty Are Health & Social Justice Issues Clean Air, Asthma & Cancer Are Health & Social Justice Issues

After Years Of Focus onConcentrating Solely On The Environment Blue Collar Job Creation Is Our Forgotten Priority!

Housing Is Still An Issue Economy

Share Underwater Mortgages Exhibit 10.-Share of Mortgages Underwater So. California Markets, 4th 2009 - 3rd 2011 55% 54% Inland Empire San Diego Los Angeles Orange 51% 49% 49% 47% 45% 44% 33% 32% 31% 30% 29% 29% 28% 28% 27% 26% 25% 25% 25% 24% 23% 23% 20% 19% 18% 18% 18% 18% 18% 17% 4Q2009 1Q2010 2Q2010 3Q2010 4Q2010 1Q2011 2Q2011 3Q2011 Source: CoreLogic

How Many Mortgages Underwater? How Much Potential Average Quarterly Competition for New Homes From Underwater Homes? When Will Underwater Homes Reach Zero At Current Rate of Decline?

Home Sales Volumes Lack of Foreclosure Sales Has Been An Issue All Home Sales Trends Southern California, 1988-2011e 160,000 IE 63,497 LA 57,636 SD 25,605 OC 21,600 Los Angeles San Diego 140,000 Orange Inland Empire 120,000 100,000 80,000 60,000 40,000 20,000 0 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011e Source: Dataquick

Is There Any Good Housing News? Last Foreclosure Sold!

Demand > Supply & Price Above Lows Price Trends by County Southern California, 1988-2011ytd $700,000 OC $493,000 SD $363,000 LA $330,700 IE $185,600 Los Angeles San Diego Orange Inland Empire $600,000 $500,000 $400,000 $300,000 $200,000 $100,000 $0 2000 2001 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Source: Dataquick

Soaring Housing AffordabilityEasily Remains At or Near Record Levels Housing Affordability, So. California Share of Families Afford Median Priced Home, 1988-2011 75% 69% 70% 65% 60% 55% 50% 42% 45% 40% 35% 33% 30% 15% 25% 20% 15% 10% 10-11% 5% 0% 2009 2010 2011 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 Source: CA Association of Realtors

Oil Prices Soaring Again Exhibit 6.-West Texas Intermediate Crude Oil Prices Monthly Average. 1985-2012 $135 $120 $105 $90 $75 $60 $45 $30 $15 $0 2011 1991 2001 2006 2007 2008 2009 2010 2012 1985 1986 1987 1988 1989 1990 1992 1993 1994 1995 1996 1997 1998 1999 2000 2002 2003 2004 2005 Source: Federal Reserve Bank of Dallas

Fear Caused Consumers Confidence It Has Recently Begun Rising

Construction Job Depression -42.6% -216,122

Office Market Housing Slowdown Hurts!

Office Vacancy Rates Have Soared! 2006 2011 Inland Empire 7.3% 23.8% Orange Co. 6.9% 18.3% L.A. Co. 9.7% 16.6% San Diego 9.4% 20.2%

Forecast 2012 Better than 2011 Foreclosures A Major Continuing Issue Complete Recovery 2015-2016?? We Need A Housing Solution!