Download

1 / 22

250 likes | 623 Vues

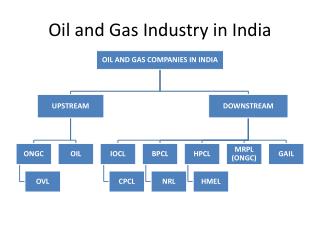

Indian Oil and Gas Industry. Contents. Market Overview. Government regulations & policy. Business opportunities and Advantage India. Indian Oil and Gas Industry - Prime mover of the Indian economy. Oil and Gas Industry Size is estimated at USD 110 bn (about 15% of Indian GDP)

E N D

Contents Market Overview Government regulations & policy Business opportunities and Advantage India

Indian Oil and Gas Industry - Prime mover of the Indian economy • Oil and Gas Industry Size is estimated at USD 110 bn (about 15% of Indian GDP) • Contributes to about 64% of gross revenues of Government (both Central and State together) through Taxes and Duties • Total Contribution to Government exchequer in 2004-05 = USD 27 bn • Contributes to about 45% of India’s primary energy consumption • Constitutes 30.87% of India’s imports in 2005-06 • Accounts for 11.21% of India’s exports in 2005-06 • India is the Sixth largest crude consumer in the world • India is the Ninth largest crude importer in the world • India’s has the sixth largest refining capacity - 2.56 million barrels per day representing 2.99% of world capacity • India is the Fifth largest energy consumer in the world • Primary Energy Consumption (2005) – 387.3 MMTOE • Oil and gas accounts for 44% of India’s primary energy consumption • Compounded Annual Growth rate of Energy Consumption (1996-2005) – 3.62% • Energy-GDP Elasticity = 0.58 India’s GDP would fall by 1.5% for every USD 10 increase in the price of oil per barrel Source: Integrated Energy Policy; BP Statistical Review 2006, Ministry of Commerce, MoP&NG, Stg Comm Report, FICCI Report, ABN AMRO , IMaCS Analysis

Supply has failed to keep pace with demand Source: DGH Presentation • Yawning Demand-Supply Gap : Need to • Intensify exploration efforts to convert the remaining prognosticated hydrocarbon reserves to established reserves • Increase recovery factor of producing fields • Tie up crude oil and gas imports – setting up of LNG Regasification terminals/ laying of transnational pipelines • Scout for equity oil and gas from abroad • Explore new technologies like coal gasification, coal to oil conversion, gas hydrates exploration, coal bed methane extraction etc.

Intensive Exploration & Production a must …. • Sedimentary Area – 3.14 million sq km • Only 19% of the area extensively explored • Domestic Hydrocarbon Scenario (as on 1.04.2006): Source: DGH / MoP&NG

Exploratory measures initiated by Government…. New Exploration Licensing Policy Coal Bed Methane Policy • 110 Production Sharing contracts in 5 New Exploration Licensing Policy (NELP) rounds • 30 discoveries with hydrocarbon in-place reserves of over 600 MMT in last 3-4 years • Investment commitment of about USD 5 bn in exploration phases under NELP • Perception of prospectivity of Indian sedimentary basins reflected in NELP VI response • 16 Blocks already awarded with production potential of 25 MMSCMD under Coal Bed Methane (CBM) I & II rounds • Significant commercial finds in blocks held by RIL and ONGC • First commercial production of CBM by 2007-08 • 54 Bids received for 10 CBM blocks offered in the third round • Award of blocks in near future Exploratory Measures

British Gas GSPC RIL ONGC HOEC OIL Cairn Government’s exploratory measures bearing fruits.. Major Upstream Players Major Discoveries Source: DGH

Oil Refining Capacity … from shortage to surplus Refinery Capacity in MMT Refinery Throughput 127 MMT (2005) • Imported Crude – 78% • Domestic Crude – 22% Refining Capacity more than doubled between 1998 and 2006 Source: MoP&NG, BP Statistical Review 2006

Petroleum product exports - a major Foreign Exchange earner Consumption 2005-06 (MMT) Exports • Sector with vast export potential • Exports increased by about 65% from 2004-05 to 2005-06 Source: MoP&NG, Ministry of Commerce & Industry

Inland Petroleum transportation – gradual shift from railways to pipelines Mode of Transportation • Share of pipeline transportation in India much lower as compared to USA, inspite of its advantages • Total POL pipeline length currently under operation in India – 12,204 kms • POL pipelines under implementation – 5,561 kms (Investment of USD 1.5 bn) Source: MoP&NG, Infraline, IMaCS analysis

Presence of both State and Private players in the Indian oil market… Marketing Infrastructure – Oil Marketing Companies Marketing Infrastructure Others Administered Pricing Market Determined Pricing Controlled Pricing Source: MoP&NG

Massive Investments planned in gas pipelines… Total Investment required in the proposed projects is about USD 15-20 bn Transnational Gas pipelines planned • Iran-Pakistan-India pipeline • Myanmar-India Pipeline • Turkmenistan-Afghanistan-Pakistan-India pipeline Source: MoP&NG, Infraline, IMaCS Research

Contents Market Overview Government regulations & policy Business opportunities and Advantage India

Government regulations have evolved over time in tune with domestic compulsions and international hydrocarbon scenario…. 1947-1962 1962-1970 1970-1990 1990-2000 Post 2000 Offer of exploration blocks to international oil companies (1979 onwards) Implementation and award of NELP blocks CBM policy Setting up of regulator – DGH (1993) Introduction of NELP Setting up of Public Sector Upstream Oil Companies – ONGC (1956) and OIL (1959) Government, the only player Upstream Free Investment Multinationals like Shell, Caltex, and Esso conducting operations Increasing Government participation Formation of national oil refining companies Coexistence of Public and Private Sectors Delicensing of Refinery sector (MRPL – 1996) Open marketing of many products Selective private participation Nationalization of foreign Companies (1970) Strict Government controls Dismantling of APM (2002) Downstream Passing ofPetroleum and Natural Gas Regulatory Board Act, 2006 Liberalised FDI regime

Policy initiatives to attract Foreign Direct Investment… • Upto 100% FDI through automatic route • Through incorporated/ unincorporated Joint Ventures or directly Exploration & Production • Upto 100% FDI if set up as a private Indian company • Upto 26% in case of state owned companies Refining Marketing • Upto 100% FDI through automatic route Product Pipelines • Upto 100% FDI through automatic route • Upto 100% FDI allowed • Approval required from Foreign Investment Promotion Board. Natural Gas/ LNG pipelines

Contents Market Overview Government regulations & policy Business opportunities and Advantage India

India offers significant advantages for the domestic and global oil and gas majors… • Strategic location • Nearness to the premier crude oil and gas supply market (Middle East) • Geographical Proximity to the major petroleum product importers – China and Japan • Well Developed Maritime infrastructure • Government policies conducive to the growth of the sector – tax holidays, Special Economic Zones for Petroleum products • Availability of experienced manpower at lesser costs –Cost advantage • Existence of hi-tech indigenous EPC Companies – lower construction periods • Large domestic market • Anchor customer of the various petroleum products • Possibility of achieving economies of scale 183 71 Source: IMaCS Research

Significant Business Opportunities exist for foreign players… • NELP rounds and Open acreage system (Opportunities for providers of services – platforms, rigs, Offshore vessels etc.) • Redevelopment of existing fields to improve recovery factor • Offer of CBM blocks through Competitive bidding route. • Natural gas hydrate programme • Underground coal gasification • Coal to oil conversion Upstream • Refining – Expansion of existing capacities, setting up of new refineries, acquiring stakes in these refineries • Ethanol and Biodiesel production – cultivation of Sugarcane and Jatropha • Petroleum marketing – setting up of retail outlets, new product pipelines. • LNG imports • Setting up of LNG Regasification terminals. • Offshore Transshipment (Single Buoy Mooring) • Laying of cross country gas grid and transnational gas pipelines • City Gas Distribution including laying of CGD and CNG networks Midstream/ Downstream

Key Players in the Indian Oil and Gas Sector All the five Indian companies in the Fortune 500 list are from the oil and gas industry

Global majors present in India • 71% stakeholder in Castrol, India’s major lubricant company • Plans to develop a 2.5 MTPA LNG Terminal at Kakinada • Participated in the CBM III and NELP VI bidding rounds – expected to win some blocks • One of the bidders for strategic sale of HPCL • Presence in both upstream and downstream • Stakeholders in Tapti gas fields and Panna/Mukta oil and gas fields, Cambay basin block • Interests in city gas distribution through participation in Gujarat Gas Limited and Mahanagar Gas Limited • Leverages its distribution assets to operate Broadband service, Iqara • Among the top FDI investors in India (Hazira port and LNG terminal project – milestone for FDI in the sector) • Interests in both upstream and downstream (LNG, Lubricants, LPG, Bitumen, retail fuels and even solar energy)

Global majors present in India • Owns 10% stakeholder in Petronet LNG Limited, a JV promoted by Indian public sector companies to set up LNG terminals to import LNG • 5% stakeholder in Reliance Petroleum Limited’s proposed new refinery at Jamnagar • Possibility of increasing the stake to 29% • Wholly owned subsidiary TotalFinaElf, a major player in lubricants market • Another 100% subsidiary ElfGas India Ltd owns and operates LPG Import Terminal at Mangalore • 50% stakeholder in LPG Import terminal at Visakhapatnam