Download

1 / 3

30 likes | 47 Vues

Read this blog if you're having trouble deciding on the best mortgage provider. A number of criteria must be met in order to find the finest mortgage lender, as we've already discussed https://bit.ly/3Kf6ZQs

E N D

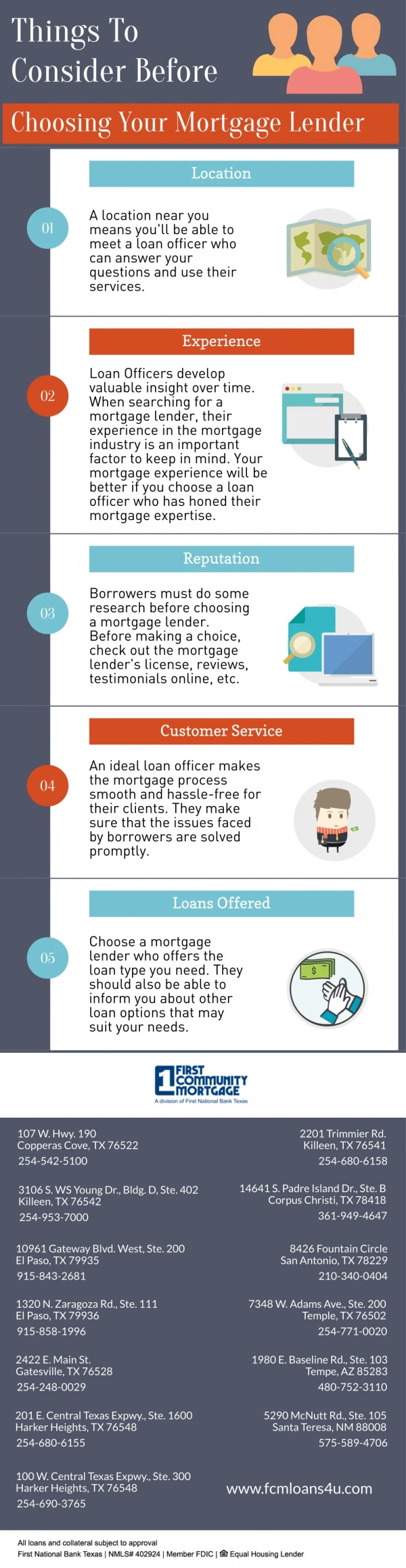

Guide to Choosing the Best Mortgage Lender It’s not always simple to track down a reliable mortgage lender who’s eager to provide you with a good deal on a house loan. Because of historically low mortgage interest rates and a rising number of mortgage lenders, competition for house loans has been strong since the Great Recession of 2008. Finding the bank with the lowest interest rate used to be all you needed to do when shopping around. Mortgage brokers, national banks, and credit unions are no longer the only places to turn when looking for a loan. With so many terms, conditions, and interest rates to choose from, it’s easy to get overwhelmed by the variety offered by each of these options. Finding the best mortgage lenders for jumbo loans and who is prepared to work with you to design the perfect mortgage might be difficult. As a first step, ask individuals you know and trust. Find out who you may talk to who has just purchased a property with a loan from your friends, family, and coworkers. Find out whether they have a preferred lender or a kind of mortgage. Mortgage Lenders: What’s the Difference?

Comparisons across a variety of criteria are necessary for identifying the best mortgage providers. Determine your spending limit Knowing how much property you can afford is an essential component of getting the correct mortgage. Even if a lender may be able to secure you a loan that would leave you with no money for unforeseen needs, it could be a terrible idea to take out such a mortgage. Your gross income, outstanding loans, and revolving debt are all taken into account when a lender preapproves your loan, according to Bates. In contrast, they don’t take into account other monthly costs, such as utility bills or gas. Include these and other costs in your budgeting process to gain a more realistic picture of your financial situation. Calculate your monthly mortgage payment or Utah down payment assistance based on your monthly net income. Find out if you qualify for any financial aid. There may be down payment and closing cost assistance programmes available to first- time homebuyers. Savings of this magnitude can be gained on the purchase of a home. Where you buy a house, and the lender you pick might have a significant impact on the kind of programmes you can access. According to Sean Moss, senior vice president of Down Payment Resource, an online aggregator of homebuyer aid programmes, many lenders engage in down payment programmes, but no one lender offers all of them. As a result, you’ll have a better sense of what options are out there by talking to a few lenders. First-time homebuyers may even be targeted by specific mortgage products and promotions from some lenders. So be careful to take into account the possibility of receiving upfront monetary help when selecting a lender. Charges and Interest Rates: Fees associated with your loan may vary depending on the lender you choose. All mortgage lenders, no matter how good they are, are susceptible to this. Application fees, document preparation fees, assumption fees, loan origination fees, closing fees, credit

report fees, mortgage broker fees, and prepayment penalties are just some of the extra costs you may have to deal with while applying for a loan. You may save money in the long run by comparing interest rates offered by different lenders. You are looking for the best mortgage lenders for first-time buyers or for refinancing. Getting just one more quotation says Freddie Mac, can save you up to $1,500 over the course of your loan. It is possible to save up to $3,000 if you acquire five quotations. People looking for a house loan don’t check rates from several lenders, according to Freddie Mac.