Download

1 / 16

160 likes | 238 Vues

This comprehensive guide covers personal tax rates, business expenses, capital allowances, and tax deduction strategies for the tax year 2014/15. Learn how to claim Plant and Machinery Allowances, Writing Down Allowances, and Annual Investment Allowance to maximize tax savings. Keep accurate records and understand the tax implications of asset sales.

E N D

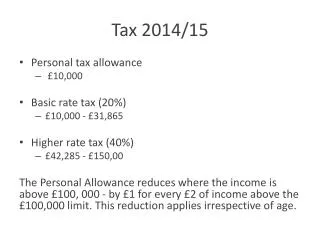

Tax 2014/15 • Personal tax allowance • £10,000 • Basic rate tax (20%) • £10,000 - £31,865 • Higher rate tax (40%) • £42,285 - £150,00 The Personal Allowance reduces where the income is above £100, 000 - by £1 for every £2 of income above the £100,000 limit. This reduction applies irrespective of age.

Tax 2014/15 • The normal tax year runs from April to April • You will need to start keeping records as soon as you start working. • Keep a note of everything you spend which is related to your business • Your mobile phone • Certain types of clothing if you are doing specialist work • Travel costs • Meals • Expenses for shoots • Etc. • Keep a note of all of your income • You should have copies of your invoices

Tax 2014/15 In working out your business profits you should not deduct the cost, that is, the expenditure incurred, of buying or improving items such as a car, equipment or other tools that you use in your business or the depreciation or any other losses which arise when you sell them. Instead, you can claim tax allowances called capital allowances. • Generally, anything you use that has a useful economic life of at least two years may qualify for capital allowances. • Equipment such as cameras, tripods etc are not counted as expenses, they are capital allowances • An adjustment, known as a balancing charge, may arise when you sell an asset, give it away or stop using it in your business. Balancing charges are added to your taxable profits, or are deducted from your losses, in the year they occur.

Tax 2014/15 You can claim allowances, called Plant and Machinery Allowances, for the cost of vans, cars (subject to special rules), machines, equipment, tools, furniture, computers and similar items which you have bought and which you use in your business. You may be eligible to claim one or more different allowances but you cannot claim more than one allowance for the same expenditure. You can choose whether or not to claim and which allowances you wish to claim. You do not have to claim the full amount of the allowance but you must specify the amount you wish to claim on your return. From 6 April 2011 the following type of plant and machinery allowances are available: • Annual Investment Allowance (AIA) of up to £100,000 • Writing down allowances (WDA) – these are annual allowances, normally calculated at 20 per cent a year, which reduce, or ‘write down’ any balance (or ‘pool’) of capital expenditure on equipment (‘plant and machinery’), not already relieved by other allowances, including cars that have CO2 emissions of 160 grams per kilometre driven (g/km) or less

Tax 2014/15 • a special rate WDA of 10 per cent which applies to certain types of plant or machinery, such as electrical systems (for example, lighting), and cars that have CO2 emissions of more than 160g/km • Small Pools Allowance – an alternative to the 20 per cent WDA and 10 per cent special rate WDA, which can be claimed for the whole balance in either the main or special rate pool where this is not more than £1,000 • 100 per cent first year allowances for investments in certain energy saving technologies and new, unused cars that have CO2 emissions of 110g/km or less • balancing adjustments – which can be either an allowance or charge. These can arise in certain circumstances (for example, when your business ceases or you sell an asset for more than the total written down value of the pool).

Tax 2014/15 Annual Investment Allowance • You can claim an Annual Investment Allowance (AIA) if you bought equipment (but not cars) on or after 6 April 2010 up to an annual amount of £100,000. (From 6 April 2012 this amount will be reduced to £25,000.) Add the cost of all the equipment together and, if the total cost is £100,000 or less, you can claim 100 per cent of that whole amount as your AIA. • the total is more than £100,000 you can claim up to £100,000. The balance can be added to the general pool of expenditure. AIA is not available to trustees or to partnerships unless all the members are individuals.

Tax 2014/15 Writing down allowances • Where you have spent more than £100,000 in a year on equipment, or have purchased a car that has CO2 emissions of 160g/km or less, (for more information about cars see pages 9 to 11), add all the expenditure together to make a ‘main pool’ of costs. Deduct any Annual Investment Allowance (AIA) up to £100,000 that you are claiming (exclude cars which are not eligible for AIA). You can then claim a writing down allowance of: • 20 per cent of the remaining pool value • What is left is then carried forward to the next year. (From 6 April 2012 the rate of writing down allowances of the main pool will be reduced to 18 per cent).

Tax 2014/15 100 per cent first year allowances • You can claim 100 per cent capital allowance for: • designated energy-saving or water efficient equipment used in your business • equipment for refuelling vehicles with natural gas, biogas or hydrogen fuel, even if you have otherwise used up your AIA • new unused cars with low CO2 emissions of not more than 110g/km. • Cars are not eligible for the AIA • new and unused zero-emission goods vehicles

Tax 2014/15 Where you use an item of equipment for both business and private purposes, the allowances you claim should be reduced by the amount of your private use so that only the business use proportion is taken into account. To do this, put each item which has any private use into a separate ‘single asset’ pool and reduce your capital allowances by the private use proportion.

Tax 2014/15 • If you are self employed you will need to fill out a tax return. • If you earn up to £77,000 you will also need to fill out the short self employment form. • If you earn over £77,000 you will also need to fill out the full self employment form. • If you are also employed you may also have to fill out the employment form.

National Insurance If you're self-employed • If you're self-employed you pay Class 2 and Class 4 National Insurance contributions. The rates are: • Class 2 National Insurance contributions are paid at a flat rate of £2.65 a week. • Class 4 National Insurance contributions are paid as a percentage of your annual taxable profits - 12 per cent on profits between £7,956 and £41,860, and a further 2 per cent on profits over that amount. • If your profits are expected to be less than £5,725 (13/14 - 14/15 not yet announced) you may not have to pay Class 2 National Insurance contributions. • Your Class 2 National Insurance contributions payments are due on 31 January and 31 July, the same as a Self Assessment tax bill. You pay Class 2 National Insurance contributions either monthly or six monthly by Direct Debit. • You pay Class 4 National Insurance contributions when you pay your Income Tax. • You pay Class 1 National Insurance contributions when you are an employee on PAYE (pay as you earn) once you earn above the taxable threshold.

VAT If you're a VAT-registered business, in most cases you: • charge VAT on the goods and services you provide • reclaim the VAT you pay when you buy goods and services for your business • If you're not VAT-registered then you can't reclaim the VAT you pay when you purchase goods and services. • UK VAT is currently set at 20%. The government reviews and adjusts the rate in conjunction with HMRC. • VAT has been 12.5%, 15% and 17.5% previously.

VAT When you must register for VAT • If you're a business and the goods or services you provide count as what's known as 'taxable supplies' (see 'What is VAT charged on' in the next slide) you'll have to register for VAT if either: • your turnover for the previous 12 months has gone over a specific limit - called the 'VAT threshold' (currently £79,000) • you think your turnover will soon go over this limit • You can choose to register for VAT if you want, even if you don't have to (Voluntary registration).

VAT What is VAT charged on? • If you're VAT-registered you'll have to charge VAT on any goods and services that you provide in the UK that are VAT taxable. • You charge VAT on the full sale price, even if you accept goods in part exchange or through barter instead of money.

VAT How VAT is charged and accounted for • If you're VAT-registered the VAT you add to the sale price of your goods or services is called your 'output tax'. The VAT you pay when you buy goods and services for your business is called your 'input tax'. Filling in your VAT Return • If you're VAT-registered you'll have to submit a VAT Return at regular intervals - usually quarterly - the return shows: • the VAT you've charged on your sales to your customers in the period - known as output tax • the VAT you've paid on your purchases - known as input tax • If the amount of output tax is more than the input tax, then you send the difference to HM Revenue & Customs (HMRC) with your return. • If the input tax is more than your output tax, you claim the difference back from HMRC. • There are special schemes that some businesses can use to help them work out and pay their VAT.

VAT Online seminars • You can watch online seminars (webinars) that cover VAT awareness and the basics of VAT. There are two types of presentation each lasting 30 minutes. The webinars can be viewed either: • Live - available on set dates and include a further 30 minutes for a live questions and answer session. They'll also be available to view from these pages after the event. • Pre-recorded - available to view at a time to suit you 24 hours a day, seven days a week. http://www.hmrc.gov.uk/vat/start/introduction.htm