Download

1 / 14

200 likes | 396 Vues

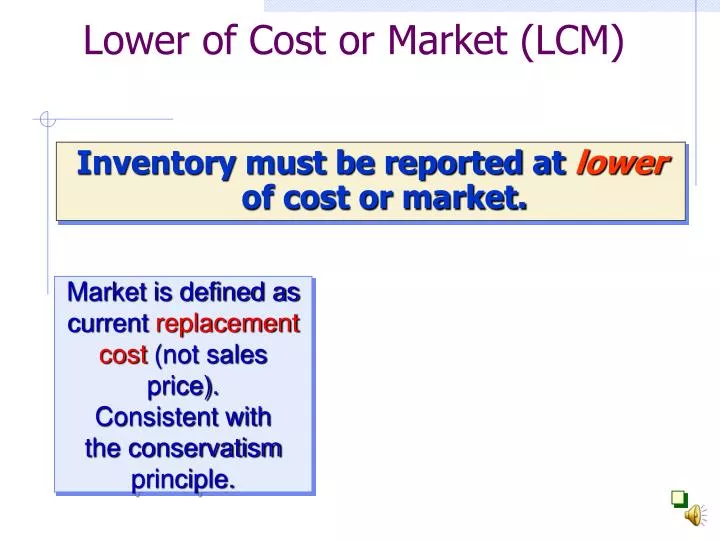

Inventory must be reported at lower of cost or market. Lower of Cost or Market (LCM). Market is defined as current replacement cost (not sales price). Consistent with the conservatism principle. “LOWER OF COST or MARKET” (LCM) VALUATION.

E N D

Inventory must be reported at lowerof cost or market. Lower of Cost or Market (LCM) Market is defined as current replacement cost (not sales price). Consistent withthe conservatismprinciple.

“LOWER OF COST or MARKET” (LCM) VALUATION For illustration -- follow class handout file (Word doc.) and next slide.

Year_1 LCM Write down: Loss on Inventory 20 Inventory 20 (from $100 to $80) Conservative for Year 1?: Income Statement Loss of $20 will lower Net Income Balance Sheet Asset Inventory reduced to $80. Year 2 If Sell for $200 at beginning of Year 2: Accounts Rec. 200 Sales Revenue 200 Cost of Good Sold 80 Inventory 80 Conservative for Year 2?: Income Statement shows ‘income’ of $120. What would the income have been IF the ‘conservative’ LCM had NOT been followed in Year 1? (CAN “CONSERVATISM CONCEPT” Possibly Lead to “BIG BATH” Accounting????) Historical cost = $100. Replacement cost at end of Year 1= $80

Estimating the Ending Inventory Balance Many companies use the gross margin method to estimate the current period’s ending inventory.

Gross Margin Method of Estimating Inventory • Provides an estimate • Not acceptable for GAAP • When to use • for interim (any period less than a year) reporting purposes • when physical inventory not possible (casualty) • a checkon the accuracy of the physical count • do we have a problem with theft?

Calculate the expected gross margin ratio using prior period’s financials. Then subtract from 100% to get the expected Cost of Goods Sold percentage. Multiply the expected cost of goods sold percentage by the current period’s sales to estimate the amount of cost of goods sold expense. Subtract the estimated cost of goods sold expense from the amount of goods available for sale to estimate the ending inventory. The Gross Profit Method

Example Given the following: Beginning Inventory $ 1,000 (cost) Purchases 9,000 (cost) Sales 12,000 (retail) Assume that gross margin has been 40% of sales.Estimate the Cost of Goods Sold for the period. Then you can “plug” the Estimated Cost of the Ending Inventory.

If the Gross Margin rate is 40%, what is the Cost of Goods Sold %? Net Sales 100% Less: Cost of G.S. X% =Gross Margin 40% = 60% Use these %’s and a partial income statement to find the “missing” amounts.

Use given amounts and known %’s Sales $12,000 Less: Cost of Goods Sold: Beg. Inv. $1,000 + Purchases, net 9,000 Goods Avail. $10,000 - End. Inv. (?) “plug” this last Cost of Goods Sold (?) (60% x Net Sales)

Use given amounts and known %’s Sales $12,000 Less: Cost of Goods Sold: Beg. Inv. $1,000 + Purchases, net 9,000 Goods Avail. 10,000 - End. Inv. (?) Cost of Goods Sold(7,200) (60% x Net Sales)

Use given amounts and known %’s Sales $12,000 Less: Cost of Goods Sold: Beg. Inv. $1,000 + Purchases, net 9,000 Goods Avail. 10,000 - End. Inv. (2,800) “plug” ($10,000 - $7,200) Cost of Goods Sold(7,200)(60% x Net Sales)

Fraud Avoidance in Merchandising Businesses Because inventory and cost of goods sold accounts are so significant, they are attractive targets for concealing fraud. Because of this, auditors and financial analysts carefully examine them for signs of fraud.

Errors in Measuring Ending Inventory • Misstatements in inventory may cause errors in the following areas: • Income Statement • Cost of Goods Sold, Gross Profit, Taxes, Net Income • Balance Sheet • Inventory, Payables, Retained Earnings • Because the ending inventory of one period becomes the beginning inventory of the next period, ending inventory errors affecttwoaccounting periods (two Income Statements but only one Balance Sheet).

![[ Lab11] Character LCM](https://cdn1.slideserve.com/2614107/slide1-dt.jpg)