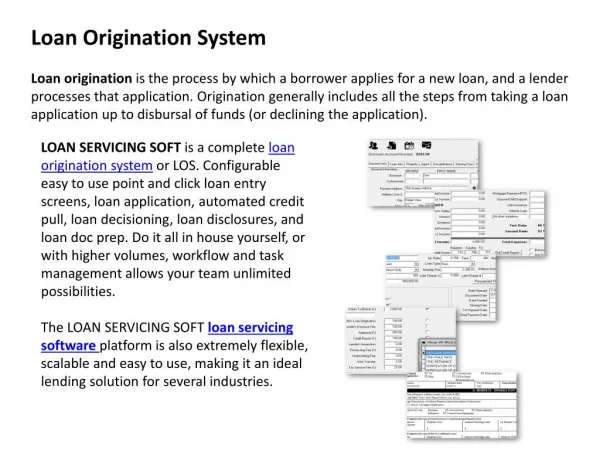

Origination

Origination. The Toughest Side of the Business: As Seen by the Loan Officer or Branch Manager Looking at a New Business Loan Request. The art of sorting through the loan prospects to pick the “deals” that best fit our Credit Union. Deal or No Deal. Too many things to do

Origination

E N D

Presentation Transcript

Origination The Toughest Side of the Business: As Seen by the Loan Officer or Branch Manager Looking at a New Business Loan Request

The art of sorting through the loan prospects to pick the “deals” that best fit our Credit Union Deal or No Deal

Too many things to do Too little time to do them If we spread ourselves too thin we can’t do anything well It’s Always So Busy! Credit Officer’s Credo It is better to spend time developing good business than massaging a loan that will never work.

Pick the best deals Bring them through the door expediently Be competitive Spend more time on the “do-able” deals Spend less time on the decline deals We are always nice people but…No lost causes! Get the Good Deals off the street!! So What Is The Object?

What is in a Loan “Package”? • 3-years business financial statements and tax returns • Personal financial statement • 3-years personal tax returns • Enough info so you can understand the loan request • We use a one-page list

We call it the “Sniff” Test By gaining a quick understanding of the loan request and the nature of the business you will be able to sort loan requests into groups: NEVER!!!! Maybe

Did You Really Say “Sniff”? • Yeah, kinda like sorting through laundry and the refrigerator when you were in college! • With experience you can quickly sort loan requests into groups: • No way • Pretty skinny but worth a look • Hmmm, now that sounds OK

Does the Deal Make Sense? “The bottom line is that business lending is not as mysterious as some think. Either the deal makes sense or it doesn’t. Quote by Credit Officer, Rich Watkins Just dig in there and see what you have—are you going to find the Pony?

Some Things (Almost) Never Work! • Startup Anything (but especially) • Restaurants • Retail • Contractors These deals go into your “No Way” pile… Always double check to see if there is a mitigating factor such as cash collateral, significant cash injection, or ? But don’t spend a lot of time on these.

YIKES! Double No to That!! • Businesses Already in Trouble • “This loan will save my business” • “If you don’t give me this loan I won’t last another month” • No apparent ability to service existing or new debt • Another Lender’s Problem • The Greater Fool Theory • Are you smarter than them? • Credit Unions often see Bank Turn Downs—new kids on the block.

Some Other Warning Signs • Relatively new business • Lack of Profitability • Credit issues/Bankruptcies/Previous business failures • Large unsecured borrowings-Little or no assets as collateral/Backup • Fad businesses or businesses that do not make sense • You do not understand what they do!

But Some of your Deals Will Have Promise As we take a closer look at the “hopefuls” you will find… Skinny deals but …Maybe? The Slam Dunk! Let’s get this deal going!

Skinny But Worth a Look • These loans you will spend a little more time with to see if it is worth looking for the “Pony”. • Maybe some weaknesses but with shoring up could work. These might have: • Strong management • Good trends • Business makes sense So how do we shore these up?

Remember…No lost causes! But… Weaknesses can be mitigated by using: • Government guarantee (SBA 7a and SBDC guarantee) • SBA 504 loans for real estate • Additional good quality collateral • Strong underlying guarantors But remember!!! These tools would only be appropriate if the loan makes sense.

The Nice Deals • Hopefully this is where you will spend your most productive time • Established businesses – At least 3-years • Good management • Adequate Cash Flow • Can Perform a Mini-Cash Flow Analysis • Clean Credit Records • Suitable/Sufficient Collateral • Reasonable guarantor financial strength

The 5 C’s of Credit • Comments on previous slide link back to the basics of Underwriting • Character • Capacity • Collateral • Capital • Conditions • Especially important in Today’s Economy • Bottom Line: Credit Scores are Currently Not Enough

What Kind of Questions? Whatever you need to determine: • Stability of business-Where it is going • Management ability to keep things under control • The sensibility of the loan request and the borrower’s ability to pay the loan back • Does this loan fit your underwriting criteria?

Make Up Your Mind! • Everyone appreciates quick feedback • The longer you “sit” on a deal the greater the expectation of the applicant • Do your basic analysis, formulate your questions and communicate with the applicant promptly • No matter what, your applicant will (usually) appreciate your advice

What’s Next? • When the Full Underwriting will be Performed by a Central Department • Complete Transmittal Document • Complete Business Background Questions • Put Package together and Submit • Samples on Following Slides

Front Back

Front Back

It’s Time to Move Ahead • After the initial “Sniff” the Underwriter will • Spread financial statements to document cash flow, trends, comparison to industry peers • Obtain credit reports-Business and personal • Do preliminary valuation of collateral • Develop a list of questions to fill in the blanks and issue a Letter of Interest

On With The Underwriting • Spreads • Credit • Loan Writeup • Other Stuff • Collateral Analysis (Appraisals, Environmental, etc) • Pricing Considerations • Documentation

Fundamentals, Always! • The temptation to slip away from the basics will always be there. Don’t do it!! • The decisions you make today will impact profits tomorrow and more importantly, the strength of your credit Union • There is plenty of good business out there. Your job is to seek it out. • That’s why…

Origination Really is the Toughest Side of the Business

Tools • This Slide Show and Samples of the: • Transmittal Sheet • Business Profile Sheet • Commercial Real Estate Staking Order • Business Loan Stacking Order • Mini Cash Flow Analysis • Can be found on our Partner’s Page • www.myisland.com/partners