Balance Sheets

Balance Sheets. Financial Statements. Provide information to: The owner Investors Creditors Three Common Statements Trial Balance Income Statement (Profit & Loss) Balance Sheet. Financial Statements.

Balance Sheets

E N D

Presentation Transcript

Financial Statements • Provide information to: • The owner • Investors • Creditors • Three Common Statements • Trial Balance • Income Statement (Profit & Loss) • Balance Sheet

Financial Statements • Balance Sheet:A statement, as of a particular date, that shows the amount of assets owned by a business as well as the amount of claims (liabilities and owner’s equity) against these assets.

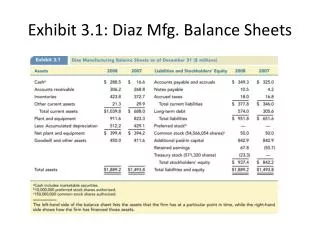

Financial Statements Tom Brown, Business Owner Balance Sheet September 1, 2003 Assets Liabilities Cash…...........…$5,425 Owner’s Equity Tom Brown, Capital…..$5,000 Net Income……………. 425 Total Liabilities & Total Assets…...$5,425 Owner’s Equity……..$5,425

The Balance Sheet includes: • Assets: Properties (resources) of value owned by a business (cash, supplies, equipment, land).

The Balance Sheet includes: • Liabilities: Obligations that come due in the future.

The Balance Sheet includes: • Owner’s equity: Rights or financial claims to the assets of a business (in the accounting equation, assets minus liabilities) by the owner.

The Accounting Equation Assets = Liabilities + Owner’s Equity Assets – Liabilities = Owner’s Equity

The Accounting Equation • The equation must be in balance. • If there is an increase to the left side the right side must increase as well. • Or an increase to the left side could cause a decrease in another account on the left side.

Assets = Liabilities + Owner’s Equity • Shift in assets: A shift that occurs when the composition of the assets has changed, but the total of the assets remains the same. • Example: • Cash is used to purchase inventory. • Both are assets – the composition has changed but the total of assets is still the same.

Assets = Liabilities + Owner’s Equity + Revenue • Revenue: An amount earned by performing services for customers or selling goods to customers; it can be in the form of cash and/or accounts receivable. A subdivision of owner’s equity: as revenue increases, owner’s equity increases.

Assets = Liabilities + Owner’s Equity - Expense • Expense: A cost incurred in running a business by consuming goods or services in producing revenue; a subdivision of owner’s equity. When expenses increase, there is a decrease in owner’s equity.

Assets = Liabilities + Owner’s Equity + Capital – Withdrawals • Capital:The owner’s investment of equity in the company. • Withdrawals:A subdivision of owner’s equity that records money or other assets an owner withdraws from a business for personal use.

Assets + Accounts Receivables = Liabilities + Accounts Payable + Owner’s Equity • Accounts Payable: Amounts owed to creditors that result from the purchase of goods or services onaccount: a liability. • Accounts Receivable: An asset that indicates amounts owed by customers.

Assets = Liabilities + Owner’s Equity & beyond • Review • When you increase your assets • You increase your Owner’s Equity • You have affected two accounts: Assets & Owner’s Equity • The equation is in balance • This is double-entry bookkeeping

Assets – Liabilities = Owner’s Equity • Assets – Owner’s Equity = Liabilities • Owner’s Equity = Assets - Liabilities

Categories of Assets & Liabilities • Assets • Current Assets (Cash, Checking, Inventory) • Non-Current Assets (Equipment, Real Estate) • Liabilities • Current Liabilities (Accounts Payable, Credit Cards) • Non-Current Liabilities (Equipment & Real Estate Loans) • Equity • Capital (contributed by owner) • Draws (withdrawn by owner) • Net Income or Loss (for the current year) • Retained Earnings (from prior years)

Cost vs. Market Value • Cost Basis- The value of an asset at the time it is purchased or acquired. • Market Value-The current value of an asset or what an asset could be sold for at the time a balance sheet is prepared.

Cash vs. Accrual • Cash Accounting-Sometimes called cash basis or cash method accounting, cash accounting records revenue and expense as they are received or paid, and does not included accounts receivable and accounts payable. • Accrual Accounting-Sometimes called accrual basis or accrual method accounting. The method of keeping records so the accounts show expenses incurred and income earned for a given period, although the expenses may not have been paid, or the income received, in the accounting period. They are accounted for as if they have been paid, or the income received.

Balance Sheet • Assets • Business Equipment $15,000 • Less Depreciation (4,500) • Total Assets $10,500