Download

1 / 13

270 likes | 1.05k Vues

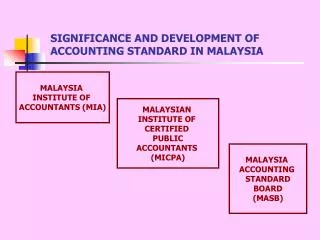

Accounting Standard Setting in Malaysia. Financial Reporting Foundation (FRF). FRF is established under Financial Reporting Act 1997. Representation from all relevant parties in the standard setting process Preparers Users Regulators & accountancy profession.

E N D

Financial Reporting Foundation (FRF) • FRF is established under Financial Reporting Act 1997. • Representation from all relevant parties in the standard setting process • Preparers • Users • Regulators • & accountancy profession

Financial Reporting Foundation (FRF) Functions • To provide its views to the MASB on development & issue of accounting standards & a conceptual framework • To review the performance, financing arrangement and operations of MASB. • To approve MASB budgets & appointment of persons to help FRF and MASB • To administer funds, • To maintain proper accounts & annual statement • appoint auditor • To forward accounts and audit report to the Min. of finance.

FRF: Definition • Accounting standards- a statements of standard accounting practices used for the preparation of financial statements. • Approved accounting standards- accounting standards approved by MASB.

Standard setting process • Identify & review issues • Appoint WG to • undertake investigation & debate the issues • Prepare & present a draft document DP – DSOP - ED to FRF & MASB • issues DSOP & ED for comments by MASB • WG Amend the ED in the light of feedback received • WG Prepare proposed standard • Consider & approve

MASB • Implement an efficient , effective & due process for development of MASB standards, conceptual framework etc. for economic decision. • Include Issue committee, Board membership, group on Islamic accounting and other working group.

MASB Standard • Adopted 24 IAS and MAS by council MIA and MICPA. • By 23 February 2003- 31 new MASB standards. • Include 30 MASB and 1 MASB i-1-Presentation of Financial Statements of Islamic Financial Institutions. • MASB Technical pronouncement-Statement of Principles & Technical Releases- e.g. Share buy back

International Accounting Standard Board (IASB) • Focus on initiatives to increase comparability between national standards and IASs. • International Financial Reporting Committee and Director of Technical Activities will report to IASB. • Malaysia is one of SAC member for IASB. • Concern for efficient allocation of capital flows across boundaries and need for harmonization of reporting standards.

Challenges for MASB • Need to play active role for international standard setting. • Provide technical expertise for high quality input to IASB. • Lack of adequate research e.g. issue of Islamic accounting standards and lack of shariah scholars who are proficient accountant.

Some amendments: • Accountant Acts 1967- MIA play more role as regulator of accounting profession and change in the composition of Council of the Institutes. • MIA members- AG, 9 rep. from BN, CCM, SC, KLSE & corporate, 5 from IHL, 4 from ACCA, CIMA, CPA and MACPA, and elected members in AGM. • Recognition for degree/diploma in accountancy at IHL to be Accountants.

DiscussionAccounting Standard Setting in Malaysia The accounting standards have traditionally been developed in Malaysian national settings • explain the standard setting process in Malaysia • describe MASB functions • what are the majors challenges for MASB • discuss the functions and powers of Financial Reporting Foundation • Discuss the impact of FRS on Malaysia Reporting Standard