FASB Update

FASB Update. Rahul Gupta Project Manager Financial Accounting Standards Board. August 14, 2013. The views expressed in this presentation are those of the presenter. Official positions of the FASB and IASB are reached only after extensive due process & deliberations. Topics.

FASB Update

E N D

Presentation Transcript

FASB Update Rahul Gupta Project Manager Financial Accounting Standards Board August 14, 2013 The views expressed in this presentation are those of the presenter. Official positions of the FASB and IASB are reached only after extensive due process & deliberations.

Topics • FASB projects • Recent Standards • Going Concern • Definition of a Public Business Entity • EITF Issues • Private Company Council

Topics • Joint projects with the IASB • Financial Instruments • Classification & Measurement • Impairment • Revenue Recognition • Leases • Insurance

Going Concern - Background • Going Concern (GC) presumption is critical to financial reporting • Today, auditors are responsible for assessing uncertainties about the GC presumption • U.S. GAAP has no guidance on management’s disclosures of GC uncertainties • Proposal intended to reduce diversity, standardize disclosure timing & content • ED issued in June 2013; comment period concludes September 24, 2013

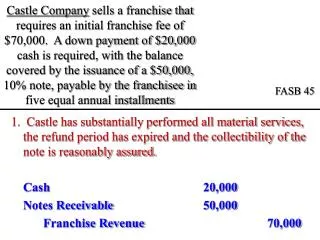

Management’s Assessment of GC Uncertainties • Proposed model: • Management at each reporting period would assess an entity’s potential inability to meet its obligations • Start disclosures if it is more-likely-than-not that an entity will not meet obligations in 12 months, or known/probable that it will not meet obligations in 24 months • Do not consider mitigating impact of plans outside the normal course of business • If likelihood reaches probable (considering all plans), declare substantial doubt (SEC filers only)

Definition of a Public Business Entity • Issue: Multiple definitions of Nonpublic Entity and Public Entity in U.S. GAAP • Objectives • Clarify organizations within the scope of private company decision making framework for potential modifications to U.S. GAAP • Simplify & increase comparability

Public Business Entity Definition A business entity that meets any one of the following criteria: • It is required by the U.S. SEC to file/furnish financial statements, or does file or furnish financial statements, with the U.S. SEC (including entities whose financial statements or financial information are required to be or are included in a filing). • It is required by the Securities Exchange Act of 1934, as amended, or rules and regulations promulgated thereunder, to file/furnish financial statements with a regulatory agency. • It is required to file/furnish financial statements with a regulatory agency for purposes of issuing securities to be traded in a public market.

Public Business Entity Definition A business entity that meets any one of the following criteria: • It has (or is a conduit bond obligor for) unrestricted securities that are traded or can be traded on an exchange or an over-the-counter market. • Its securities are unrestricted, and it is required to provide U.S. GAAP financial statements to be made publicly available on a periodic basis pursuant to a legal or regulatory requirement. • This excludes a not-for-profit entity or an employee benefit plan within the scope of Topics 960 through 965 on plan accounting.

Definition of a Private Company • Next steps • Issuance of an Accounting Standards Update in August 2013 • Would not affect existing requirements. • Comment period ending September 2013

Private Company Council: Projects Next Meeting: September 2013 • Accounting for identifiable intangible assets in a business combination (Issue 13-01A) • Accounting for goodwill subsequent to a business combination (Issue 13-01B) • Applying variable interest entity guidance to common control leasing arrangements (Issue 13-02) • Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps (Issue 13-03)

PCC Issue 13-01A Proposed Changes Accounting for Identifiable Intangible Assets in a Business Combination • Modifies requirement for private companies to separately recognize fewer intangible assets acquired in a business combination • Enables private companies to recognize only those intangible assets arising from noncancelable contractual terms or assets from other legal rights • Other intangible assets would not be recognized separately from goodwill even if separable

PCC Issue 13-01B Proposed Changes Accounting for Goodwill Subsequent to a Business Combination • Goodwill amortized for a period not to exceed 10 years, and tested for impairment only when a triggering event occurs • Goodwill tested for impairment at the company-wide level as compared to the current requirement to test at the reporting unit level • Impairment testing would also involve a one step approach as opposed to two-step approach

PCC Issue 13-01B Proposed Changes Accounting for Goodwill Subsequent to a Business Combination • Step two of the current impairment test, which requires the application of a hypothetical purchase price allocation to calculate the goodwill impairment amount, would be eliminated • Instead, the goodwill impairment amount would represent the excess of the company’s carrying amount over its fair value

PCC Issue 13-02 Proposed Changes Applying Variable Interest Entity Guidance to Common Control Leasing Arrangements (FIN 46(R)/FAS 167) • Exempts private companies from applying the consolidation guidance for variable interest entities under common control leasing arrangements • If substantially all activities between private company and lessor are involved with leasing activities of the lessor • When the arrangement between a private company lessee and a lessor entity meets certain conditions, the private company lessee can elect the alternative

PCC Issue 13-02 Proposed Changes Applying Variable Interest Entity Guidance to Common Control Leasing Arrangements (FIN 46(R)/FAS 167) • Conditions to qualify for alternative • Lessor entity and the private company lessee are under common control • Company lessee has a leasing arrangement with the lessor entity • Substantially all of the activity between the two entities is related to the leasing activity of the lessor entity • Ex: guarantee on the lessor entity’s mortgage on a leased asset

PCC Issue 13-03 Proposed Changes Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps • Gives private companies the option to use two simpler approaches to accounting for certain types of interest rate swaps that are entered into the purposes of economically converting its variable-rate borrowing to a fixed-rate borrowing • Combined instruments approach • Simplified hedge accounting approach

PCC Issue 13-03 Combined Instruments Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps • An accounting alternative to account for a swap and a variable-rate borrowing as one combined financial instrument. I • Swap would not be recorded in the company’s financial statements (except for the period-end accrual relating to the next swap settlement)

PCC Issue 13-03 Combined Instruments Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps • Applied provided certain criteria are met: • Swap term approximates the term of the borrowing and the swap becomes effective at the same time as the borrowing. • Approach would be applicable to all of its swaps, whether entered into on or after the date of adoption or existing at that date, provided that the requirements of applying this approach otherwise are met. • Under this approach the settlement value of the swap would be disclosed in the notes to the financial statements.

PCC Issue 13-03 Simple Hedge Accounting Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps • Practical expedient to qualify for hedge accounting • Criteria to qualify for simplified hedge accounting similar to combined instruments approach criteria • However, term of the swap could be shorter than the term of the borrowing and the swap does not have to become effective at the same time as the borrowing

PCC Issue 13-03 Simple Hedge Accounting Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps • Under approach, swap and the related borrowing would continue to be accounted for as two separate financial instruments • However, no ineffectiveness would be assumed for qualifying swaps designated in a hedging relationship • Designated swap may be recorded at settlement value in the company’s financial statements instead of at fair value

Financial Instruments: Overview • Improve decision usefulness • Reduce complexity • Convergence • Three phases: • Classification & Measurement • Impairment • Hedge Accounting

Classification & Measurement: Background • FASB Exposure Draft (May 2010) • Fair value model • Feedback: • Key aspects opposed • Lack of convergence • Joint Redeliberations (Jan 2012) • FASB’s tentative model • Guidance in IFRS 9 • Converged in principle

Classification & Measurement: Financial Assets Classified in one of three categories: • Amortized cost—financial assets with solely payments of principal and interest that are held for the collection of contractual cash flows • Fair value through other comprehensive income (OCI)—financial assets with solely payments of principal and interest that are both held for the collection of contractual cash flows and for sale • Fair value through net income—financial assets that do not qualify for measurement at either amortized cost or fair value through other comprehensive income. (residual category)

Classification & Measurement: Financial Assets Equity investments • Equity investments measured at fair value through net income • Practicability exception – No readily determinable fair value • Observable price changes in orderly transactions for the identical or similar assets of the same issuer • One-step impairment model • Hybrid Financial Assets • No bifurcation • Apply solely principal & interest test to entire instrument

Classification & Measurement:Financial Liabilities • Generally amortized cost, unless: • Business strategy is to transact at fair value • Short sale • Nonrecourse debt • Hybrid Financial Liabilities • Bifurcation and separate accounting of embedded derivatives based on existing U.S. GAAP

Classification & Measurement:Fair Value Disclosure • Public Companies • Financial assets & financial liabilities measured at amortized cost • Parenthetical presentation of fair value on the face of the balance sheet • Exceptfor receivables/payables due in less than a year and demand deposit liabilities • Private Companies • NOT required to disclose fair value information either parenthetically or in the notes to the financial statements.

Impairment: Project Objectives Timely Recognition of Credit Losses • Address concerns about delayed recognition of losses under incurred loss approach • Present value of cash flows an entity expects to collect consistent with classification & measurement objective for assets held for collection • Single model for loans and debt securities

Impairment: Project Objectives Separate Presentation of Interest Income & Credit Losses • Rate of return includes lender compensation for credit risk inherent in debt instrument • Investors want separate presentation of credit losses from interest income (“decoupled” approach) • Effective rate as discount rate (in a DCF approach) isolates credit loss & does not introduce noise related to market changes

Impairment: Basics of FASB Model • Every reporting period, expected credit losses would be re-estimated • Favorable and unfavorable changes reported in earnings • Current estimate of expected credit losses based on: • current risk ratings of the assets • historical loss experiencefor assets with similar risk ratings and remaining lives adjusted for changesin current circumstances • reasonable & supportable expectations about the future

Impairment: Basics of FASB Model Expected losses are inherent in groups of similar assets; inability to identify which asset will deteriorate should not interfere with timely recognition of losses that are expected in the individual assets held

Impairment: Basics of FASB Model FASB used term “full” rather than “lifetime” to avoid suggesting that projections through the remaining life are necessary. Rather, we expect estimates will start with historical information, and be adjusted using available information that indicates that current expectations differ from past experience

Impairment: Debt Securities and FV-OCI Assets • Same approach as loans • As a practical expedient, entity may elect not to recognize expected credit losses for financial assets classified at FV-OCI when both of the following conditions are met: • FV of financial asset is greater than amortized cost basis • Expected credit losses on financial asset are insignificant • For high-quality assets; cost-benefit consideration

Impairment: Purchased Credit Impaired (PCI) Assets • Common issue for business combinations & portfolio transfers; current U.S. GAAP is complex & confusing • Same approach to estimating expected credit losses as originated and non-PCI assets • Initial estimate of expected credit losses is recognized as an adjustment to the cost basis of the asset (an allowance) and would not be recognized as interest income