Download

1 / 38

430 likes | 1.65k Vues

Cash Budget. Budgets. A budget is a short term financial plan CIMA defines a budget as a “plan expressed in money” Budget are prepared in advance They concern what is forecast and planned for the period of the budget

E N D

Budgets • A budget is a short term financial plan • CIMA defines a budget as a “plan expressed in money” • Budget are prepared in advance • They concern what is forecast and planned for the period of the budget • A cash flow forecast is budget dealing with planned inflow and outflow of cash

Cash flow forecast • Cash flow refers to the movement of cash into and out of a business • Cash budgets • Seek to predict the flow of cash into and out of the business • Are forecasts enabling businesses to manage cash flow • Are an essential part of the planning process

Internal and external use • Banks and other lenders will insist on a cash budget before granting a loan • The potential creditor will seek assurance that net cash inflows will be sufficient to repay the loan with interest • But even if the business is not seeking a loan it is still important to construct a cash budget • This is to ensure that the business will be able to meet its obligations as they arise and, equally important, to take advantage of any surplus cash

The purpose of a cash budget • To know in advance what the likely cash balance at the end of each month • To increase management awareness of potential shortages and surpluses of cash • To avoid problems associated with lack of cash to pay debts • To fine tune operations to ensure adequate cash is available • To arrange financing to cover a period of cash shortage • To provide information to make decisions on the use of cash surplus

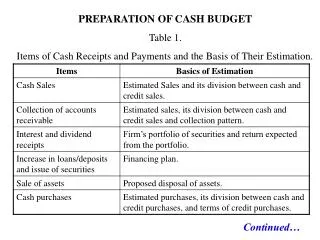

Budget profit and loss account Forecasts sales revenue, associated costs and profit Includes all forecast sales and associated spending for the year- whether or not cash flows Depreciation is a negative item Does not include planned capital expenditure or raising finance Cash budget Forecasts inflow and outflow of cash Only includes transactions where cash flows Depreciation is ignored as a non-cash item Includes everything where cash moves in or out of the business Comparisons of Cash & P&L Budgets

If it moves count it! • Accounting is characterised by rules about how items are treated - the rules behind accounting have their own logic even though outsiders can find them baffling. • Cash budgeting on the other hand is based on a few very simple rules: • If it leads to a cash flow (into or out of the business) count it • If there is no cash flow then ignore it • If cash flows in, it is a positive item • If cash flows out, it is a negative item

Importance of Spreadsheets • Cash budgets are best produced using a spreadsheet • Each column represents a month of the year whereas each row across represents various categories of inflow and outflow • The use of a spreadsheet not only improves presentation and but also makes it easier to make amendments where necessary • The planned inflows and outflows are recorded in the cells of the spreadsheet - so we have a record of not just how much but also when the cash is expected to flow

Cash inflow • Fromsales • Cashfromsales. • Cashfromcreditsales(comesinafteratimelag) • Fromowners • Cashfromashareissue-capitalinvestedinthebusiness • Fromlenders • Bankloan • Cashfromthedisposalofunwantedassets • E.g.disposaloffixedassets

Forecasting cash inflow • This is the greatest problem in constructing the budget • For an established business forecast sales will be based on time series analysis (e.g. moving averages). This involves isolating the trend and extrapolating it into the future • Forecasting is more difficult for start up businesses with no past track record • As well as customer demand, the forecast should take the firm’s capacity into account • As well as forecasting total sales it is also necessary to forecast timing and the likely balance between cash and credit sales • Remember credit sales in January might not result in a cash inflow until February or March

Types of cash outflows • Purchasesofstockpaidforincash • Paymenttocreditors • Paymentofwages • Paymentofrent • Paymentofinsurancepremium • Expenditureonmarketing • Purchaseoffixedassets • Paymentofinterestondebt • Paymentoftax • Anypurchaseoncreditwillshowupincolumnofthemonthinwhichcashflowedout

Purchases of stock • This will be a major ongoing item in the cash budget • Stocks bought on credit will usually be paid for in a subsequent month. As with cash inflow from sales, purchase of stocks in a cash budget will show up in the month in which the cash flowed out • Normally there is a mathematical relationship between sales and purchases. For instance purchases of stock might be one-third of sales revenue • This relationship will be used when constructing a cash budget

Timing of cash flows is all-important • Remember the cash budget does not record when the sale or purchases are expected to be made • Instead it records when cash moved • When the cash from credit sales is expected to flow into the business • When the cash for credit purchases is expected to flow out of the business

Net cash flow • Net cash flow is equal to • Cash inflow for the period (e.g. a month) minus • Cash outflow for the same period • Negative cash flow: outflows exceed the inflows • Positive cash flow: inflows exceed the outflows

Opening balance • This refers to the cash position at the start of the month • Assuming that all money is banked and all payment is made from the firm’s bank account, the opening balance is the state of the firm’s account at the start of the month • This could be positive or it could be negative

Closing balance • This equals the opening balance plus the net cash flow • Remember that it is possible for opening balance to be negative-similarly the net cash flow could be negative • When you add the opening balance and closing balance together be careful about negative and positive values • The closing balance of one month becomes the opening balance of the next

Commentary on the example • We start the year with a bank overdraft of £120K • In January cash payments are expected to exceed cash inflow from sales by £90k • With a net cash outflow, the forecast overdraft at the end of the month shows a rise • The closing balance at the end of January becomes the opening balance for February • Cash inflow is expected to improve in February but a net cash outflow is still expected for the month. As a result the overdraft is forecast to rise • In March there is an expected net cash inflow • A reduction in the overdraft is projected and this is the sum that will be taken into April as the opening balance

The role of a cash budget • Highlights when cash balances are expected to be positive so that surplus cash can be invested appropriately • Identifies when outflows might exceed inflow • Ensures that the firm has sufficient cash to carry out planned activities • Ensures that cash balances are sufficient to meet expected payments • Justify to lenders that any borrowed funds can and will be repaid • Plan when and how to finance significant items of expenditure • Plan for any bank overdraft or loan which may become necessary • Control cash flow by comparing actual events against plans • Optimise the holdings of cash (e.g. invest surplus cash)

What if questions • Cash budgets produced on a spreadsheet are especially useful in answering “what if” questions • What will be the impact on cash flow of • a rise in the cost of stock? • a rise in interest payments or rent? • investment in new fixed assets? • a wage rise? • lower than expected sales? • If we change in one cell of the spreadsheet we can rapidly analyse the new scenario

Cash budgets and new businesses • A cash budget is an essential part of a business plan and loan application • The typical start up business will experience negative net cash flow in the early months or even years • This is because of high start-up costs and slow growth in sales • The cash budget helps owners/ managers to plan finance in order to steer the business through this difficult period

Seasonality • Although we associate seasonality with Easter eggs, firework, tourism and sun tan lotion the fact is that a large proportion of all businesses experience some seasonal fluctuations in sales • Seasonality will be reflected in the cash budget - there will be periods of net cash outflow caused by low seasonal sales and these will be followed by periods of net cash inflow during the peak season • A cash budget enables manager to plan spending to cope with this problem

Monitoring and control • It is usual to subdivide the column for each month into: • the budgeted cash receipts/payments forecast for the month • the actual cash receipts/receipts in the month • There difference between the two figures is known as a variance

Favourable and adverse variances • A favourable variance is one where the actual figure is better than the budget (or forecast) figure: • cash receipts higher than expected • cash payments lower than expected • An adverse variance is unfavourable. The actual figure is worse than the budget figure: • cash receipts lower than expected • cash payments higher than expected

Variances - questions to ask • What was the size of the variance? • What was the variance as a percentage of the budget figure? • Was it favourable or adverse? • Was the variance within normal tolerance? • What is the explanation for the variance? • We did not foresee it but was it foreseeable? • What can we do get back on track?

Some explanations for variances • Incorrect sales forecasts • Change in the environment leading to reduced sales • Suppliers insist on payments more rapidly than expected • Unexpected rise in costs • Production problems leading to reduced output and sales • Discounts offered to boost sales

Cash management • Aim–tohavetherightamountofcashavailableattherighttime • Thereisatradeoffbetweenliquidityandopportunitycosts • liquidityisneededinordertosettledebtsastheyfalldue • buttheopportunitycostofholdingcashisthelossofearningsfromusingcash • Goodcashmanagementrequires: • accuratecashflowforecastingandmonitoring • obtainingshort-termborrowingwhenneeded • investinganysurpluscash

Cash shortages • Shortagesofcashresultsin • creditorsbeingunpaid • legalactionforrecoveryofdebt • inabilitytopurchasestocks • refusaltosupplymorecredit • disruptiontoproduction • resultantlossofsales • labourunrestthroughinabilitytopaywages • businessfailure

Surplus cash • Cashrichbusinessesoftenfailtotakeadvantageofacashsurplus • Surpluscashcanbe • spentonstock • usedtopurchasefixedassets • depositedinaninterestbearingaccount • investedinR&D • usedtofinanceacquisitions • investedinnewproducts • lentintaxefficientways

Causes of cash flow problems • Over-investment in fixed assets • Overtrading - rapid expansion with insufficient working capital • Poor credit control - excessive credit, late payment by debtors, bad debt • Suppliers wanting quick payment • Stock piling - excessive investment in stock • Seasonal variations in sales and cash flow • Over borrowing at high interest rates • Changing tastes - decline in sales • Management error-poor planning

Solution: increase inflow • Sell idle fixed assets • Sale and leaseback • Stimulate sales by price discount • Improve debtor control – chase debtors • Discounts for prompt customer payment • Tighter credit control • Debt factoring • Raise more capital • Arrange overdraft facilities

Solution: reduce outflow • Lengthen supplier credit terms • Postpone investment • Reduce stock holding-adopt lean production techniques (e.g. JIT) • Purchase stock on credit • Ask trade creditors for extended credit • Spread the cost of purchases - lease or hire purchase • Negotiate rescheduling of debt payments • Diversify to avoid seasonal variations in cash flow • Improve planning, monitoring and control