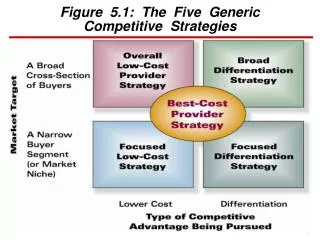

THE FIVE GENERIC COMPETITIVE STRATEGIES

THE FIVE GENERIC COMPETITIVE STRATEGIES. Chapter 5 MGT 4380. Strategic Management Process. What is a competitive strategy?. Competitive Strategy Concerns management’s " game plan " for competing successfully and securing a competitive advantage over rivals (strategy as…PLAN)

THE FIVE GENERIC COMPETITIVE STRATEGIES

E N D

Presentation Transcript

THE FIVE GENERIC COMPETITIVE STRATEGIES Chapter 5 MGT 4380

What is a competitive strategy? • Competitive Strategy • Concerns management’s "game plan"for competing successfully and securing a competitive advantage over rivals (strategy as…PLAN) • Represents the firm’s specific efforts to provide superior value to customers by offering: • An equally good product at a lower price (low cost) • A superior product with unique features perceived as worth paying more for (differentiation) • An attractive overall mix of price, features, quality, service, and other appealing attributes (best cost)

Creating Value…? Customer Value This area represents the value created in each profitable sale and consists of both profit to the firm and surplus to the customer. Consumer Surplus Selling Price KEY Adopting and adapting a strategy or strategies that balance firm costs, profit, and overall value for customers Profit Total Value Total Cost to the Firm This area representsthe firm’s total costs in presenting the product or service for sale. To create new value, the firm must cover its total costs. COGS

Low-Cost Strategies • Firms offer a broader array of products and/or services at a relatively low price • Has a lower cost than rivals—but not necessarily the absolutely lowest possible cost • Includes features and services that buyers consider essential, but little more • Is viewed by consumers as offering equivalent or higher value even if priced lower than competing products (i.e., Great Value v. name-brand products

How do low-cost strategies work? Option 1 • Use lower-cost advantage to under-price competitors and attract price-sensitive buyers • Lower profit margins than competitors mean firms must sell in large volume Option 2 • Maintain present price and current market share and use lower-cost edge to earn higher profit margin • Higher profit margin means that firms can sell less than competitors and earn more

How can firms develop a low-cost strategy? • Perform essential value chain activities more cost-effectively than rivals • E.g., better access to raw materials, more efficient production, cheaper distribution, etc. • Revamp the firm’s overall value chain to eliminate or bypass some cost-producing activities • Eliminate non-essential costs • E.g., reduce input/production quality, concentrate on markets that are easy to access

Other ways to manage the value chain… • Striving to capture all available economies of scale • Taking full advantage of experience and learning curve effects • Trying to operate facilities at full capacity • Pursuing efforts to boost sales volumes and thus spread outlays for R&D, advertising, and general administration over more units • Substituting lower-cost inputs whenever there’s little or no sacrifice in product quality or product performance • Employing advanced production technology and process design to improve overall efficiency • Using communication systems and information technology to achieve operating efficiencies • Pursuing ways to reduce workforce size and lower overall compensation costs • Using the company’s bargaining power vis-à-vis suppliers to gain concessions • Being alert to the cost advantages of outsourcing and vertical integration

When does a low-cost strategy work best? • Price competition among rival sellers is especially vigorous. • The products of rival sellers are essentially identical and are readily available from several sellers. • There are few ways to achieve product differentiation that have value to buyers. • Buyers incur low costs in switching their purchases from one seller to another. • The majority of industry sales are made to a few, large-volume buyers. • Industry newcomers use introductory low prices to attract buyers and build a customer base.

What are the pitfalls to avoid in a low-cost strategy? • Overly aggressive price cutting • Price cutting results in lower margins, no increase in sales volume, and lower profitability • Reliance on easily-imitated cost reductions • Becoming too fixated on cost reduction • Ignoring buyer interest in additional features • Overlooking declining buyer sensitivity to price • Denying technological breakthroughs that will nullify cost advantages

Broad Differentiation Strategies • Firms offer broader array of products and/or services that are unique from others • Useful whenever buyers’ needs and preferences are too diverse to be fully satisfied by a standardized product or service • Involves incorporating differentiating features that cause buyers to prefer one firm’s brand, product, or service over those of its rivals (i.e., branding, market pioneering, etc) • Requires not spending more to achieve differentiation than the price premium that customers are willing to pay for all the differentiating extras

Successful execution of a differentiation strategy allows a firm to: Command a premium price Increase its unit sales Gain buyer loyalty to its brand What are the benefits of a differentiation strategy? Just think about Apple….

What are the different approaches to a differentiation strategy? • Unique taste: Red Bull, Dr. Pepper • Multiple features: Microsoft Office, Apple iPhone • Wide selection and one-stop shopping: Home Depot, Amazon.com • Superior service: Ritz-Carlton, Nordstrom • Spare parts availability: Caterpillar, John Deere • Engineering design and performance: Mercedes-Benz, BMW • Luxury and prestige: Rolex, Gucci, Chanel • Product reliability: Johnson & Johnson • Quality manufacture: Michelin in tires, Honda in automobiles • Technological leadership: 3M Company • Full range of services: Charles Schwab in stock brokerage • Complete line of products: Campbell soups, Frito-Lay snack foods

How does a differentiation strategy create value? • Includesproduct attributes and user features that lower the buyer’s costs • E.g., hybrid cars save gas, professional tax prep may help save money, etc • Incorporatestangible features that improve product performance • E.g., engine turbo, high performance processor, etc • Incorporatesintangible features that enhance buyer satisfaction in noneconomic ways • E.g., supports a certain cause (i.e., Girl Scout cookies)

Manufacturing activities Supply chain activities Activities that Enhance Differentiation Product R&D Distribution and shipping activities Marketing, sales, and customer service activities Production R&D and technology-related activities How can firms develop a differentiation strategy?

When does a differentiation strategy work best? • Buyer needs and uses of the product are diverse. • There are many ways to differentiate the product or service that have value to buyers. • Few rival firms are following a similar differentiation approach. • Technological change is fast-paced and competition revolves around rapidly evolving product features.

What are the pitfalls to avoid in a differentiation strategy? • Pursuing a differentiation strategy keyed to product or service attributes that are easily and quickly copied. • Incorporating product features or attributes in which buyers see little value or are easily copied by rivals. • Overspending on efforts to differentiate. • Over-differentiating so that product quality or service levels exceed buyers’ needs. • Trying to charge too high a price premium. • Not opening up meaningful gaps in quality or service or performance features over the products of rivals.

Focused Strategies • Reflect a concentration on a narrow piece of the total market defined by geographic uniqueness or special product attributes • Can be either (1) low-cost focused or (2) differentiation focused • Appeal to smaller and medium-sized firms that may lack the breadth and depth of resources to tackle going after a whole market customer base

Focused Low-Cost Strategy • A focused strategy based on low cost aims at securing a competitive advantage by serving buyers in the target market niche at a lower cost and a lower price than rival competitors • E.g., Vizio TVs, Acer PCs, etc. • Avenues to achieving cost advantage are the same as for low-cost leadership • out-manage rivals in keeping costs low • bypassing or reducing nonessential activities

Focused Differentiation Strategy • Keyed to offering carefully designed products or services to appeal to the unique preferences and needs of a narrow, well-defined group of buyers • E.g., Kashi, Tesla, Helly Hanson, etc. • As opposed to a broad differentiation strategy aimed at many buyer groups and market segments

When is a focused strategy viable? • The target market niche is big enough to be profitable and offers good growth potential • Industry leaders have chosen not to compete in the niche—focusers can avoid battling head-to-head against the industry’s biggest and strongest competitors • It is costly or difficult for multi-segment competitors to meet the specialized needs of niche buyers and at the same time satisfy the expectations of mainstream customers • The industry has many different niches and segments, thereby allowing a focuser to pick a niche suited to its resource strengths and capabilities • Few, if any, rivals are attempting to specialize in the same target segment

What are the pitfalls of a focused strategy? • If and when competitors find effective ways to match a focuser’s capabilities in serving the target niche • If and when the preferences and needs of niche members shift over time toward the product attributes desired by the majority of buyers (the few join the many) • If and when the segment may become so attractive it is soon inundated with competitors

Best-Cost Strategies • Are a hybrid of low-cost provider and differentiation strategies that: • Involves giving customers more value for money by satisfying buyer expectations on key quality/features/ performance/service attributes and beating customer expectations on price • Is a powerful competitive approach with value-conscious buyers looking for a good-to-very-good product or service at an economical price • Creates a “best-cost” status as the low-cost provider of a product or service with upscale attributes

How can firms develop a best-cost strategy? • Best-cost strategies are contingent on: • A superior value chain configuration that eliminates or minimizes activities that do not add value • Unmatched efficiency in managing essential value chain activities • Core competencies that allow differentiating attributes to be incorporated at a low cost

When does a best-cost strategy work best? • A best-cost provider strategy works best in markets where: • Product differentiation is the norm (e.g., clothing) • The market is comprised of large numbers of value-conscious buyers attracted to economically priced midrange products and services, especially during recessionary times (e.g., food service) • A provider can offer either a medium-quality product at a below-average price or a high-quality product at an average or slightly higher-than-average price (e.g., automobiles)

What are the pitfalls of a best-cost strategy? • Vulnerability to both low-cost providers and high-end differentiators • May not have the core capabilities to manage the value chain such that the firm can produce higher-quality products at a lower price • Difficult to “serve two masters”—quality and price • Often, firms that attempt a best-cost strategy get “stuck in the middle”

Getting “stuck in the middle” • Compromise strategies can result in middle-of-the-pack industry rankings and, at best, average performance due to: • An average cost structure • Minimal product differentiation relative to rivals • An average image and reputation • Limited prospect of industry leadership • Compromise or middle-ground strategies rarely produce sustainable competitive advantage • Examples include: K-Mart, GM, American Airlines

Successful Competitive Strategies Are Resource Based • Low-Cost Providers • Must have the resources and capabilities to keep costs below those of competitors • Must have expertise to cost-effectively manage value chain activities better than rivals • Differentiators • Must have the resources and capabilities to incorporate unique attributes that a broad range of buyers will find appealing and worth paying for

Successful Competitive Strategies Are Resource Based • Narrow Segment Focusers • Must have the capability to do an outstanding job of identifying and satisfying the needs and expectations of niche buyers • Best-Cost Providers • Must have the resources and capabilities to incorporate upscale product or service attributes at a lower cost than rivals