Reverse Mortgage Misconceptions

Reverse mortgages can be a significant financial tool for seniors, yet many myths surround them. Misconceptions include fears of losing one's home, needing a debt-free property, or affecting Social Security benefits. This article addresses common myths, clarifying that borrowers retain their home’s title, can utilize home equity regardless of existing debt, and that reverse mortgage funds are generally not taxable. Understanding these facts empowers seniors to make informed choices about their financial future.

Reverse Mortgage Misconceptions

E N D

Presentation Transcript

Reverse Mortgage Misconceptions Courtesy of: First Financial Reverse Mortgages 1-800-720-7003 FirstFinancial@firstloans.net Consult your financial advisor and appropriate government agencies for any effect on taxes or government benefits. Consolidating debt may result in higher overall interest cost over the life of the loan. Consult your financial advisor on paying short term debt with your mortgage loan. Make sure you understand the features associated with the loan program you choose and the effect of an adjustable rate to your overall loan cost. Advisor and/or broker/correspondents are independent entities and do not form legal partnership or agency relationships with Financial Freedom.

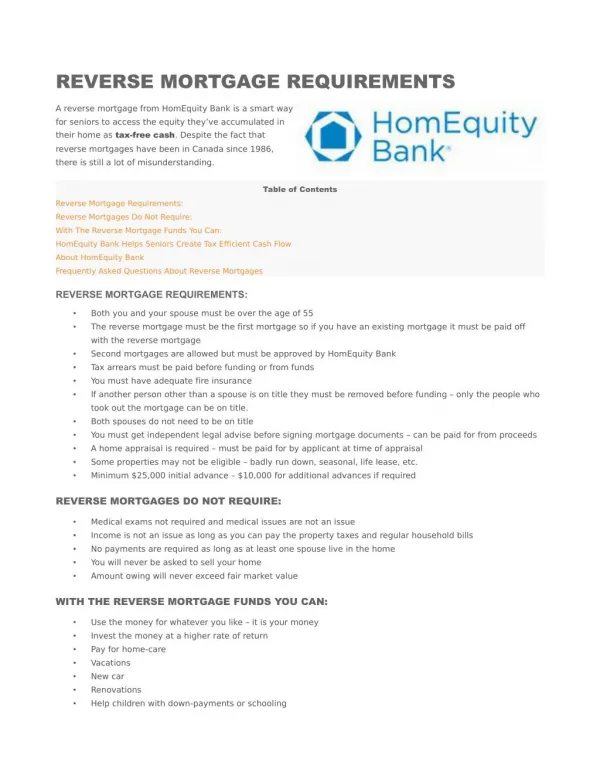

Reverse Mortgage Myths As reverse mortgages continue to grow in popularity, so have a range of myths about these unique loans. Let’s take a look at some of the most common misconceptions and discuss the facts. • The bank takes away OR I will lose my house • The home must be debt free to qualify for a reverse mortgage • The bank sells the home when the reverse mortgage becomes due • My children won’t be comfortable with me obtaining a reverse mortgage • The borrower could end up owing more than the house is worth • Reverse mortgage proceeds will impact Social Security and Medicare benefits • There are restrictions on how the money is used and taxes will have to be paid on it • Reverse mortgages are only for seniors in need, or for the ‘house rich, cash poor’

Myth #1: The bank takes away OR I will lose my house FACT: With a reverse mortgage, the borrower retains title to the home throughout the life of the reverse mortgage: • The borrower cannot, as a result of the reverse mortgage, be forced out of his or her home as long as property taxes and hazard insurance are paid, the home is maintained in reason living condition, and at least one borrower resides the home as their primary residence. • The loan must be repaid once the last borrower permanently moves out of the home.

Myth #2: The home must be debt free to qualify for a reverse mortgage FACT: Reverse mortgages convert home equity into cash. As long as there is sufficient equity in the property, the homeowner may be eligible for a reverse mortgage. In fact, many seniors use a reverse mortgage to pay off an existing mortgage in order to eliminate a required monthly mortgage payment.

Myth #3: The bank sells the home when the reverse mortgage becomes due FACT: The borrower is in control of the home and retains title, not the bank or lender. So while it’s common for the borrower or the heirs to sell the home to repay the loan, it’s a decision the borrower or the heirs make. The borrower or the heirs might also refinance the home in order to repay the loan.

Myth #4: My children won’t be comfortable with me obtaining a reverse mortgage FACT: Seniors are encouraged to talk with their children about reverse mortgages. Many baby boomers are faced with trying to plan for their retirement and pay for their children’s education. Often, the children of many seniors are happy that their parents have a financial solution available to help them live more independently and financially secure.

Myth #5: The borrower could end up owing more than the house is worth FACT: Two of the great built in safeguards of reverse mortgages are that they are structured so that the borrower can never owe more than the fair market value of the home upon repayment*. In addition, HECM products are insured by the Federal Housing Administration, an arm of the U.S. Department of Housing and Urban Development (HUD). *If the borrower or the heirs want to keep the house by refinancing the debt and paying off the reverse mortgage, the borrower or heirs must payoff the balance in full, regardless of the value of the property. If the last borrower has moved out of the property and the property will be sold in an arm’s length transaction, the property may be sold for the fair market value and neither the borrower’s estate nor the heirs will be responsible for a deficiency balance.

Myth #6: Reverse mortgage proceeds will impact Social Security and Medicare benefits FACT: A reverse mortgage will generally not affect regular Social Security payments or Medicare benefits. Depending upon the borrower’s situation, a reverse mortgage may affect benefits one receives, if any, from the Federal Supplemental Security Income (SSI) program, or state-administered programs like Medicaid. It is recommended that the borrower speak with his or her financial advisor and appropriate governmental agencies.

Myth #7: There are restrictions on how the money is used and taxes will have to be paid on it. FACT: Actually there are no restrictions. The cash proceeds from a reverse mortgage can be used for almost any purpose and since it’s already your money, it’s tax-free. Many seniors have used reverse mortgages to travel, pay off debts, help their kids, make a luxury purchase or just live more comfortably.

Myth #8: Reverse mortgages are only for seniors in need, or for the ‘house rich, cash poor.’ FACT:Reverse mortgages are an excellent financial planning tool that has been used by homeowners from all walks of life to enhance their retirement years. In fact, with the new 2009 lending limit, many seniors are benefiting from increased cash benefit from a reverse mortgage.

Come On In…The Process is Easy 1. Contact us at First Financial 1-800-720-7003 2. Discuss and review benefit illustration 3. Set up an appointment with a HUD approved housing counselor 4. Complete application 5. Order FHA appraisal 6. If loan is approved, all outstanding conditions must be cleared 7. Draw loan documents 8. Three day right of rescission 9. Loan funds, documents are recorded and proceeds are disbursed as instructed