INCOME TAX RATES

This guide provides a comprehensive overview of income tax rates applicable to individuals earning purely compensation income, as well as those engaged in business and professional practice in the Philippines. It also details provisions for non-resident aliens involved in trade or business, alongside relevant revenue issuances and codal references. Understanding these tax obligations is crucial for compliance and financial planning.

INCOME TAX RATES

E N D

Presentation Transcript

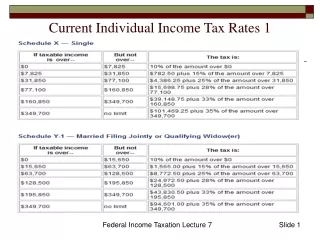

A. For Individuals Earning Purely Compensation Income and Individuals Engaged in Business and Practice of Profession

*Beginning on the 4th year immediately following the year in which such corporation commenced its business operations, when the minimum corporate income tax is greater than the tax computed using the normal income tax.

Related Revenue Issuances RR No. 4-95, RR No. 4-96, RR No. 5-97, RR No. 1-98, RA 9337, RR 14-2002, RR 12-2007 Codal Reference Sections 23-59, 67-73 and 74-77 of the National Internal Revenue Code