Download

1 / 94

940 likes | 958 Vues

This article discusses tax consequences and basic analysis of tax-free exchanges, specifically focusing on the transfer of unqualified property and the receipt of unqualified property with cash. It also explains the tax implications when transferring property subject to a liability.

E N D

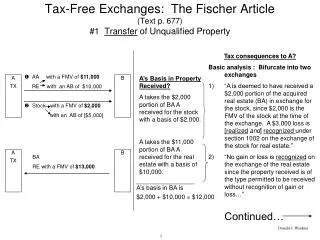

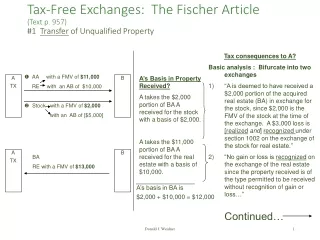

Continued… Tax-Free Exchanges: The Fischer Article(Text p. 957)#1 Transfer of Unqualified Property A’s Basis in Property Received? A takes the $2,000 portion of BA A received for the stock with a basis of $2,000. A takes the $11,000 portion of BA A received for the real estate with a basis of $10,000. • Tax consequences to A? • Basic analysis : Bifurcate into two exchanges • “A is deemed to have received a $2,000 portion of the acquired real estate (BA) in exchange for the stock, since $2,000 is the FMV of the stock at the time of the exchange. A $3,000 loss is [realizedand] recognized under section 1002 on the exchange of the stock for real estate.” • “No gain or loss is recognized on the exchange of the real estate since the property received is of the type permitted to be received without recognition of gain or loss…” • AA with a FMV of $11,000 RE with an AB of $10,000 • Stock with a FMV of $2,000 with an AB of [$5,000] A TX B A TX B BA RE with a FMV of $13,000 A’s basis in BA is $2,000 + $10,000 = $12,000 Donald J. Weidner

A’s basis in BA is $2,000 + $10,000 = $12,000 Total basis in BA First Exchange 2/13ths interest Second Exchange 11/13ths interest A’s total basis in BA is the sum of the bases A received in the two exchanges in which he received an 11/13 interest in BA and a 2/13 interest in BA. If A later sells BA for $13,000, A will realize and recognize the remaining $1,000 gain on that sale. The basis rules postpone the gain: take $13,000 FMV property at $12,000 basis. Full recognition on two exchanges would have been: $1,000 gain + $3,000 loss The loss is recognized Donald J. Weidner

A’s basis in the real property received (see 1031(d)) : • AB in property given up $5,000 • + Gain recognized 2,000 • - cash received 2,000 • any loss recognized n/a • Basis in real property received $5,000 #2 Receipt of Unqualified Property (Recall 1031(b))(taxpayer actually receives cash)The Taxpayer must value the property received A Transfers RE with AB of $5,000 B Transfers: RE [with FMV of $6,000] • Cash of $2,000 A TX B Tax consequences to A? Here, A’s realized gain is computed AR = $8,000 [$6,000 FMV of RE + $2,000 cash] -AB = $5,000 [basis in RE transferred to B] GAIN = $3,000 Gain Realized “The gain [realized] from the transaction is $3,000, but is recognizedonly to the extent of the cash received of $2,000.” Recognition of the remaining gain is deferred under 1031(a). “The receipt of cash in partial consideration for the exchange of property is tantamount to a partial sale of the property and will cause the recognition of any gain accordingly.” A takes 1. $2,000 cash with $2,000 basis; and 2. $6,000 FMV property with $5,000 basis. $1,000 additional gain remains to be recognized Donald J. Weidner

Transfer of Property Subject to a Liability and 1031(taxpayer is deemed to receive cash) • See 1031(d): “For purposes of this section . . . where as part of the consideration to the taxpayer another party to the exchangeassumeda liability of the taxpayer oracquired from the taxpayer propertysubject to a liability, such assumption or acquisition (in the amount of the liability) shall be considered as money received by the taxpayer on the exchange.” • When one transfers property subject to a liability, the shifting of that liability to another is treated as a receipt of “other property or money” by the transferor under 1031(b)—even if the transferee only takes “subject to” the liability. Donald J. Weidner

Transfer of Property Subject to a Liability and § 1031 (deemed receipt of cash) (cont’d) • Recall Tufts: one who transfers property subject to a mortgage is deemed to receive (“constructively receives”) cash in the amount of the unpaid balance of the mortgage. • The amount of the mortgage is treated either as an “amount realized” or as “discharge of indebtedness income,” depending upon the circumstances. • The following example shows an exchange of property subject to a mortgage and is from Treas. Reg. 1.1031(d)-2, Example (1). Donald J. Weidner

Subject to a 150,000 M AB = $500,000 Continued… Apt. House #1 has a FMV of $800,000 and a net equity of $650,000 [equal to the $650,000 value that Tx. B received]. In a taxable exchange, A’s amount realized would be $800,000 ($650,000 cash and property received plus $150,000 mortgage “relief”), producing a $300,000 gain that is both realized and recognized. B Txpr. Transfers Apt. House #1 with $800,000 FMV C Transfers Apt. House #2: [with a FMV of $600,000] + 50,000 cash Note: because there is a receipt of unqualified property, the properties exchanged must be valued. Tax Consequences to B under 1031? What has B obtained in the exchange? Consideration received by B: $150,000 “relief” 600,000 value 50,000 cash Total Consideration $ 800,000 How much gain did be realize in the exchange? Total Consideration $ 800,000 -AB (unrecovered cost) 500,000 Realized Gain $300,000 If §1031(b) applies: The realized gain is not all recognized. Recognized gain is limited to cashreceived and non-like kind property received. Actual Cash Receipt $ 50,000 +Deemed Cash Receipt 150,000 Total cash received $200,000 **Note there is a twin limitation on recognition: the lesser of the gain realized or the cash received. Donald J. Weidner

Continued… $ 200,000 realized gain that is recognized + 100,000 realized gain not recognized per 1031 $ 300,000 total realized gain Recognition of the realized but unrecognized gain is deferred until the new property is transferred in a subsequent taxable exchange. What is B’s Basis in Apt. House #2? B takes apartment house #2 with a basis that is computed as follows: AB in property transferred (apt. house #1) $500,000 - cash received actual 50,000 constructive 150,000 200,000 - 200,000 + gain recognized on exchange +200,000 B’s Basis in Aptmt House #2 $500,000 • Subsequent sale by B of Apt. House #2: • If that house were sold with no other change in value, it would be sold for $600,000 and gain would be: $600,000 AR -500,000 AB $100,000 The remaining $100,000 of gain that was realized but unrecognized on the exchange is finally recognized on the subsequent sale. Granted that you want to allocate basis to the cash you actually receive (up to its face amount), why do you want to allocate $150,000 basis to the cash you only constructively receive? You must pay back the “advance credit,” the basis, you received in the amount of the mortgage when you acquired the property. Mayerson,Tufts. Donald J. Weidner

Section 1031 Recap • Back to the bigger picture. For §1031 to apply, there must be: 1. an exchange • a “reciprocal transfer of property”; 2. of qualified properties • That is properties held either for: • use in a trade or business; or • investment; 3. that are of like kind (nature or character matters [real property versus personal property], not “mere” grade or quality [developed for undeveloped]). Donald J. Weidner

Starker v. United States (9th Cir. 1979)(Text p. 963) (Starker II) Day 1 April 1, 1967 “Land Exchange A’ment” T.J. Starker, his son and his son’s W (“Starkers”) Crown Zellerbach Starkers agreed to convey all interests in 1,843 acres of timberland in Oregon Crown agreed “to acquire and deed over” real property in Washington and Oregon Within 5 years or Crown will pay the Starkers any outstanding balance in cash Each year, Crown must add a 6% “growth factor” to the outstanding balance of the “exchange value credits” it gave the Starkers Day 1 + 2 months May 31, 1967 [2 mos. later] Crown entered “exchange value credits” on its books Crown Starkers $1.5 million for T.J.’s timberland $73,000 for S, S’s W’s timberland The Starkers Deeded their timberland Received their own “exchange value credit’ of $73,000 for the land they exchanged. Pays $ S, S’s W found 3 suitable parcels, which Crown purchased and conveyed to S, S’s W, pursuant to the contract. The agreed value of the 3 parcels was equal to the exchange value credit. Crown Seller S, S’s W (Bruce & Elizabeth) Within 4 mos. Starker I Conveyed (sold) Donald J. Weidner Txprs. and victors inStarker I

Starker I and Starker II: The Nonsimultaneous Transfers • The son and his wife were the taxpayers in Starker I—they defeated an IRS attempt to deny them 1031 treatment. • Having lost against the son and his wife, the IRS went after the father in Starker II. • The 9th Circuit concluded that Starker I collaterally estopped the IRS from attacking the portion of the exchange dealing with 9 parcels that Crown purchased and conveyed to the father. • Which left with only 3 parcels to discuss in Starker II. • None of the 3 parcels discussed in Starker II was deeded to the father, T.J. (or to his daughter), at or near the time T.J. conveyed his timberland to Crown. • That is, the common issue as to all three parcels is that the reciprocal transfers were not simultaneous. Donald J. Weidner

# 1. Conveyed Timian, Residence, in 1967, to T.J.’s Daugher Held: Nonrecognition is Denied to T.J.– NOT “held for investment” under 1031 because used as a personal residence. Also Held: because TJ never got title, there was no exchange with him.* Starker II (the first two parcels—conveyance to TJ’s daughter)Timian (Residence) & Bi-Mart (Commercial) TJ TJ’s Daughter [Jean Roth] [who was not a party to the “Land Exchange Agreement”] Crown $ Seller Transferred possession of residence Residence $ Paid rent Seller Commercial Property # 2. Conveyed Bi-Mart (commercial building) to T.J.’s Daughter in 1968 [TJ spent substantial time, money, improving and maintaining Bi-Mart in the 3 months before it was conveyed to his daughter. TJ argued he controlled and managed the Bi-Mart property and directed its transfer to her.] Held: Because TJ never got title, there was no exchange with him.* Donald J. Weidner

Starker II— IRS Arguments about the Timian (residence) Property Conveyed to T.J.’s Daughter • First, There was no “exchange” of property with T.J. because there was no transfer to TJ-- title to the Timian property never went to T.J. • Because there was no identity of economic interests between T.J. and his daughter, a transfer to her did not constitute a transfer to him. • The court accepted this argument • Second, even if there were transfers of property to TJ, they were not “reciprocal” because they were not simultaneous (recall, IRS Regs. define an exchange as a “reciprocal transfer of property”) • Instead, there was a sale on credit rather than an exchange. • Note, this is a plausible argument against all three transfers involved in “Starker II” Donald J. Weidner

Starker II: IRS Arguments About the Timian (residence) property conveyed to T.J.’s Daughter (cont’d) • TJ did not receive any 1031 qualified property because he did not receive any “trade or business” or “investment” property. • Rather, he received personal residence property. • And so the personal residence property TJ received was not of “like kind” with the investment property he gave up. Note: The court rejected T.J.’s “substance over form” argument that this was, in economic substance, a transfer of title to him followed by a gift from him to his daughter. The court was similarly formalistic as to the Bi-Mart (commercial) property transferred to T.J.’s daughter: • it concluded that T.J. never received title to the Bi-Mart properties because Crown transferred them to his daughter. Donald J. Weidner

Starker II: Timing of Recognition as to Timian and Bi-Mart • Because the Timian and Bi-Mart transfers did not qualify for nonrecognition under 1031, T.J. was required to recognize the gain he realized on the exchanges. • When? • Court: “treat T.J. Starker’s rights in his contract with Crown, insofar as they resulted in the receipt of the Timian and Bi-Mart properties, as ‘boot,’ received in 1967 when the contract was made.” • Note the problem: how does you report in an initial year (1967) the value of property not identified or transferred to you until a later year (1968) qualifying? Donald J. Weidner

Starker II: Timing of Recognition as to Timian and Bi-Mart (cont’d) • The apparent answer: wait until the later year, say, year 2, to decide whether there was a qualifying LKE. If there was no qualifying LKE, go back to year 1 and treat yourself as having received boot to the extent of the value of the nonqualifying property you received in year 2. • What if the future year is year 5? Does the statute of limitations run on year 1? • “We realize that this decision leaves the treatment of an alleged exchange open until the eventual receipt of consideration by the taxpayer. * * * If our holding today adds a degree of uncertainty to this area, Congress can clarify its meaning.” Donald J. Weidner

Starker II and Section 1031(a)(3) • Congress added § 1031(a)(3) in direct response to Starker II. • The “identification” requirement. Property will not be treated as like kind unless it is “identified as property to be received in the exchange” (unless the taxpayer picks it out) within 45 days after the taxpayer has transferred his property. • The “exchange” requirement. Property will not be treated as like kind unless it is received(by the taxpayer) within 180 days after the transfer • (or after the due date for the tax return for the year of the transfer). • The modified § 1031 also impacts the Starker II holding with respect to the Booth property (the third, commercial parcel) • as to timing, not as to the philosophy that contract rights to acquire real property can be a fee equivalent Donald J. Weidner

Starker II: The Booth Property (commercial) (the third parcel—contract rights were transferred to TJ) In 1965, Buyer signed a contract to purchase real property from Seller. The contract was subject to a carved-out life estate. In 1968 (a year after the “Land Exchange Agreement”), Crown purchased the Buyer’s rights under the contract and assigned them to TJ. 1965, Third Party Contracts to sell subject to a life estate Assigned Buyer’s contract rights [1968] Buyer, 1968, Sells his contract rights to purchase real property subject to the life estate TJ Crown Buyer • Legal title is not to pass until the life estate expires. • Until legal title passes, the Buyer is entitled to possession, subject to certain restrictions. • For example, the Buyer is • prohibited from removing improvements and • required to keep buildings and fences in good repair. Donald J. Weidner

Starker II: The Booth Property • IRS argued: There was no exchange. • Not only was there a lack of simultaneity to the conveyances between T.J. and Crown; • there was no conveyance at all to T.J. (there was a “total lack of deed transfer”) • Even after the expiration of 10 years • Stated differently, the IRS argued that, because T.J. never received a conveyance of land, he never received property that was of a “like kind” with the land he transferred . Donald J. Weidner

Starker II: The Booth Property • The Court rejected the IRS argument and held instead that T.J. had been transferred the equivalent of a fee: • IRS Regulations say that a lease with 30 years or more to run is the equivalent of a fee; • T.J.’s rights are at least as great as those of a long-term lessee; and • the fact that his interest will ripen into a fee prior to the expiration of 30 years, if the life tenant dies, only makes the equivalence with a fee stronger. • Once the court said that contract rights are of “like kind” with a fee, it was brought to the basic question: is the exchange disqualified because the transfers were not simultaneous (and hence not “reciprocal”). Donald J. Weidner

Nonsimultaneous Transfers • Recall the basic justifications of 1031 • Do non-simultaneous transfers fall within them? • Liquidity rationale. Doesn’t fully explain 1031. • If you sell, then immediately reinvest the proceeds, the benefits of 1031 are not available even though the reinvestment leaves the taxpayer illiquid. • Conversely, the benefits of 1031 seem to be available even if the taxpayer has no liquidity problems. • Valuation rationale. Doesn’t fully explain 1031. • Whenever the taxpayer receives any cash or non-qualifying property in an exchange that otherwise qualifies, the property received must be valued to compute the realized gain, a part of which must be recognized. Donald J. Weidner

Nonsimultaneous Transfers (cont’d) • Three aspects of the case make the IRS position appealing (9th Circuit focused only on the last two): • the “exchange agreement” gave the Starkers the equivalent of a deposit into a checking account, not on a bank but on a major corporation; • it also gave them the possibility that they might ultimately simply receive cash; and • the agreement could remain open for a long time. Donald J. Weidner

Final Thoughts on Starker II • 9th Circuit said: • if the parties intended to effect a swap of property, 1031 treatment is not denied simply because cash was to be transferred if a swap could not be arranged • Recall Rev. Rul. 90-34 (Supp. p. 247) • elsewhere, in an attempt to deny taxpayers a loss, the IRS has argued that 1031 applies even if there is no strict simultaneity. Donald J. Weidner

Final Thoughts on Starker II (cont’d) • IRC 1031(a)(2)(F) says that 1031 does not apply to an exchange of “choses in action.” • As to the argument that these contract rights were mere choses in action and not equal to a fee, the 9th Circuit stated: • “[T]itle to real property is nothing more than a bundle of potential causes of action: for trespass, to quiet title, for interference with quiet enjoyment, and so on;” and • “The bundle of rights associated with ownership is obviously not excluded from section 1031; a contractual right to assume the rights of ownership should not . . . be treated as any different than the ownership rights themselves.” • Analyzing the bundle of rights and liabilities that make up an interest is also done in the analysis of leasing arrangements, including sale/leasebacks. Donald J. Weidner

The Sale-Leaseback: Advantages to “Buyer” • Starker’s “bundle of rights” discussion is evocative of Justice Scalia’s observation in Bollinger: “The problem we face here is that two different taxpayers can plausibly be regarded as the owner.” • This is also often the case in the sale-leaseback area. • For years, most life insurance company investments involved sale-leasebacks with creditworthy corporations. • They received statutory authority in the late 1940s to make direct investments in income-producing real property • A life insurance company typically received rent for the property it purchased sufficient to enable it, over the initial term of the lease, • to recover its entire investment, • plus a satisfactory rate of return on that investment. Donald J. Weidner

The Sale-Leaseback: Advantages to “Buyer” (cont’d) • The lease provided that the life insurance company would be made whole by the tenant, even in the event of total condemnation or destruction of the property. • Recall Bolger, in which the tenant’s obligation to pay rent continued even if the property were destroyed • Although the insurance company/buyer must include the rent in income, it gets to take depreciation deductions on its investment in the building • assuming the form of the transaction is respected for federal income tax purposes • As in Leslie(where the seller also claimed a loss on the sale) Donald J. Weidner

The Sale-Leaseback: Benefits and Burdens of “Tenant” • Smith & Lubell, Reflections on the Sale-Leaseback, 7 Real Estate Review 11-13 (Winter 1978) states: “This lease imposes on the lessee virtually all of the obligations, and gives the lessee substantially all of the benefits, of ownership, subject of course to the lessor’s reversionary rights in the fee.” • Recall, for example, Bolger. Allocating virtually all the burdens and benefits of ownership to the tenant during the life of the lease, creates the risk that the lessee might be seen as the substantive owner-mortgagor. Donald J. Weidner

The Sale-Leaseback: Benefits and Burdens of “Tenant” (cont’d) • Smith & Lubell state the burdens that fall on the tenant: As in “any ground lease or other absolutely net lease,” “the lessee is obligated to pay rent without off-set or deduction and also to pay • Real estate taxes; • Fire, liability and other insurance premiums; • All costs of operating, maintaining, repairing, and restoring the premises; and • All other costs relating to the premises that an owner would normally bear.” Donald J. Weidner

The Sale-Leaseback: Other Advantages to “Seller-Tenant” • Some of the tenant benefits under the lease: • Seller-tenant retains the use of the property. • Seller-tenant may minimize its equity investment in a property. • Greater financing may be available to a developer who sells and then leases back than under “conventional mortgage financing.” • Some corporate tenants may obtain 100% financing. Donald J. Weidner

The Sale-Leaseback: Other Advantages to “Seller-Tenant” (cont’d) (and one disadvantage) 3. Seller-tenant may achieve “off-balance sheet” financing • If the Financial Accounting Standards Board (FASB) classifies the lease as an “operating lease” rather than as a “capital lease.” • Until ASU 2016-2 takes effect and every lease for more than year must be capitalized and recorded on the balance sheet as a “lease liability” 4. Seller-tenant gets the right to deduct all rent (while losing the depreciation deduction on its investment in the building) • including the rent for the land, thereby effectively writing off the land cost. • The loss of the property at the end of the lease term is a disadvantage—a benefit that passes to the buyer-lessor • unless there are options to renew or to purchase • but that remote “price” may have a low present value. Donald J. Weidner

Some Recent Developments • Many other institutional and foreign investors have been providing financing through sale-leasebacks. • As other forms of 100% financing became available, such as through real estate subsidiaries, large creditworthy corporations entered into fewer direct sale-leaseback transactions with insurance company investors. • Accounting rules have for years made it much more difficult for sale leasebacks to be used to take debt off balance sheets. • There has been more room in the case of leases of property the tenant did not previously own • After ASU 2016-2, all leases for more than a year must be recorded on the balance sheet as representing both a “right of use” asset and a “lease liability” • The Liability that is listed is the present value of the future lease payments. • Today, many creditworthy corporations obtain financing through special purpose entities that issue securities • Recall Bolger Donald J. Weidner

Sale-Leasebacks as Equitable Mortgages • FASB has long limited the use of the sale-leaseback to take financing off the “tenant’s” balance sheet. • Saying that many leases, especially those arising from sale/leasebacks, are “capital leases” that must be reported as mortgages on the tenant’s books. • The latest FASB rules being phased in require the present value of all lease payments (if the lease is for more than a year) to be recorded on the balance sheet as a “lease liability” • The off-balance sheet issue has most commonly arisen when the seller-lessee is unwilling to give up the reversionary interest in the property. • There can be “significant exposure” because the transaction may be treated, either for state law purposes or for federal income tax purposes, say Smith and Lubell, as “an equitable mortgage, rather than a true conveyance and a true lease.” Donald J. Weidner

Consequences if Substance Trumps Form • If the form of a sale-leaseback is disregarded and it is treated as, in substance, a mortgage: • The lessee will be seen as having an equity of redemption such that, if the lessee defaults, the lessor will not be permitted to evict by summary proceedings but will be required to foreclose the lessee’s equity of redemption; • If the lessee becomes bankrupt or insolvent, the lessor will have the rights of a secured creditor rather than the rights of a landlord; • A deemed mortgage may be subject to substantial mortgage and intangible taxes that were not anticipated; Donald J. Weidner

Consequences if Substance Trumps Form • The resulting mortgage may be found to be usurious; and • The tax consequences of the transaction will change: • There will be no gain or loss on the sale; • The rent will be treated as debt service (with only interest deductible by the tenant and included by the landord); • The tenant, and not the landlord, will be entitled to depreciation deductions. Donald J. Weidner

Bankruptcy or Insolvency of Tenant • In general, in bankruptcy, a lease is an executory contract and, as such, is subject to special rules. • An executory contract is both an asset and a liability because there is still substantial performance required on both sides of the contract. 1. If the lease characterization is upheld: • In the event of a lessee’s bankruptcy (Ch. 11 reorganization), the Debtor (in the bankruptcy sense) In Possession (“DIP”) has a choice to affirm or reject the lease. • If the lessee’s DIP affirms the lease, it must start making current payments. • If the lessee’s DIP rejects the lease, the rejection will be treated as an anticipatory breach of the lease and the landlord will have an unsecured claim for damages. Donald J. Weidner

Bankruptcy or Insolvency of Tenant (cont’d) 2. If the lease is recharacterized as a mortgage: • The “Lessor’s” claim against the tenant is treated as a secured claim (rather than a landlord’s claim for breach of a lease) and the tenant’s Debtor In Possession will be excused from paying debt service during the bankruptcy proceeding. • Then, if a “plan” is confirmed, debt service payments from the tenant to the lessor will resume (although the plan may restructure the loan agreement). Donald J. Weidner

Bankruptcy or Insolvency of Tenant (cont’d) • G. Nelson and D. Whitman Real Estate Finance Law 73 (5th ed. 2007): • “[I]f the lessee-seller goes into bankruptcy, he or she usually finds it much more advantageous to be a mortgagee than a lessee. • This is because a lessee who files a bankruptcy petition must either assume or reject the lease within a short period of time or the lease will be deemed rejected. In the latter situation, the lessee will be required to surrender the property immediately to the lessor. • On the other hand, if the transaction is characterized as a mortgage, the seller-mortgagor often will be able to retain possession of the real estate and restructure the mortgage obligation as part of a bankruptcy reorganization plan. • Finally, on rare occasions, a lessor-purchaser rather than the lessee-seller will seek to recharacterize a sale-leaseback transaction as an equitable mortgage.” Donald J. Weidner

Frank Lyon Company v. United States(Text p. 981) • Worthen Bank owned a parcel of land and was constructing a building on it. • There was an office building construction race in downtown Little Rock • The Bank wanted to hold title to the building and finance it through a wholly-owned real estate subsidiary. • Bank regulators would not approve this approach, saying the building was too expensive. • Frank Lyon Company (“Lyon”) was a distributor of home appliances. • The Chairman of the Board of Lyon, Frank Lyon, was also on Worthen Bank’s Board of Directors. • The regulators would let Lyon lease the building. • The construction lender and the permanent lender approved Lyon as an acceptable borrower. Donald J. Weidner

Frank Lyon (cont’d) • Worthen Bank: • Retained title to the land; • Net leased the land to Lyon for 76 years; • Sold the building, piece by piece, as it was constructed, to Lyon; and • Leased back the building from Lyon for 66 years. • In short, Worthen conveyed to Lyon the right to possess the land for 10 years longer than Worthen retained the right to possess the building. • Lyon owned the reversion in the building, which would become possessory after Worthen’s 66-year lease ended. That is, during Lyon’s last 10 years as tenant under the ground lease, Worthen no longer had the right to be a tenant of the building. Lyon could occupy the building itself or lease it to someone else. • Presumably, after that 10-year period, Lyon would have to remove its building from Worthen’s land or take out a new lease. • Was this transaction ever expected to go to term? Donald J. Weidner

Frank Lyon (cont’d) Maximum Bldg.Price: $ 500,000 Cash 7,140,000 Mortgage $7,640,000 N.Y. Life Note and Mortgage Bank Bldg. Bank Sells Bldg. Then Becomes a Tenant in It Bank “sold” bldg. to Buyer Bldg. Buyer [Lyon Co.] Lyon Bought Building on the land it was leasing Lyon was ground lessee for 76 Years Bank “leased” bldg. back from Buyer for: Total of 66 years [25 year base term + 8, 5-year options to renew] $600,000/yr. rent for the 25-year base term, then, rent cut in half. Bank got options to repurchase bldg. . Ground lease Land Bank Retained Title to Land but Leased It to the Bldg Buyer 76 years [$50/yr. rent for first 26 years, then rent increases] Lease of building gave Bank control of bldg. for 65 years. After that, Lyon had the right to keep the building on the bank’s land for 10 more years. Stated differently, Lyon had a leasehold estate in the land that lasted for only 10 years after Bank’s options to renew the building lease expired. Donald J. Weidner

Frank Lyon (further facts) • Lyon agreed to buy the building from Worthen Bank at price not to exceed $7,640,000 • Payable: $ 500,000 cash 7,140,000 N.Y. Life Mortgage $ 7,640,000 • The “permanent lender” participated by a “Note Purchase Agreement.” • Lyon’s note to New York Life was the promise to pay. • To secure repayment of the note, New York Life received: • Lyon gave New York Life a 1st deed of trust on the building and Bank “joined in the deed of trust as the owner of the fee.” • Bank also gave New York Life a mortgage on an adjoining parking deck. • Lyon assigned to New York Life its rights as Landlord under the building lease with Bank (Bank agreed to the assignment); • Lyon assigned to New York Life its rights as Tenant under the ground lease with Bank. • Actual cost of complex (excluding land) was $10,000,000. • Lyon’s offer to pay lower rent for the first five years was first accepted and later changed into an agreement to pay higher interest to the Bank on a “subsequent unrelated loan.” Donald J. Weidner

Lyon’s Net Cash Flow on its investment in the building (if Bank keeps exercising its options to renew the lease) These are 8 additional 5-year terms available to Bank under building lease. That is, the rent Lyon RECEIVES from the bank does not change once these 5-year lease renewal terms begin. BUT the rent Lyon must PAY the bank for as ground rent keeps going UP. Ground lease from bank 10 years longer than building lease to Bank (Bank did not have an option to lease the bldg. for the last 10 years of its ground lease to Lyon). Donald J. Weidner

Condemnation or Destruction • Bank’s obligation to pay rent to Lyon was not affected by any damage or destruction to the building. • That is, Bank had greater obligations than those of a normal tenant • But not greater obligations than those of tenants in sale-leasebacks. • Any (a) condemnation award, and (b) any insurance proceeds resulting from a total destruction of the building, would be applied in the following order: • to New York Life in an amount sufficient to fully prepay the mortgage; • the next tranche to Lyon up to the amount of Lyon’s $500,000 down payment plus 6%; then • any excess to Bank. • Thus: condemnation awards were allocated as if Bank was the owner and New York Life and Lyon were both lenders. • Bank had the option to either replace the building or to purchase it in the event of a partial condemnation or total destruction on or after December 1, 1980 (after about 12 years). • Here again, Bank had more of the bundle of sticks than is usually in the hands of a “mere” tenant. Donald J. Weidner

Bank Had Four Options to “repurchase” the building • After 11 years for $6,325,169 • in fact, Worthen purchased at this point, when its tax shelter would have collapsed • After 15 years for $5,432,607 • After 20 years for $4,187,328 • After 25 years for $2,145,935 The option price at each date equaled: • The unpaid balance of the N.Y.Life Note; plus • Lyon’s $500,000 down payment plus 6% compound interest Donald J. Weidner

Bank’s options to “repurchase” the building(cont’d) The prices on the options to purchase were the same as if Lyon had a 6% passbook account with the Bank. However, the District Court said that the option price: “also represents the negotiated estimate of [Lyon] and [Bank] as to the fair market value of the building on the option dates, which the court finds to be reasonable. The [IRS] produced no witnesses to contest the reasonableness of the option prices.” Was the District Court too credulous? Donald J. Weidner

Bank’s Options to Repurchase the Building (cont’d) • The District Court concluded that the Bank was unlikely to exercise these options to purchase, given: • The Bank’s future capital requirements; • The substantial amount of the option price; and • The reasonableness of the net rent the Bank would pay if it remained a Tenant. • Bank also had a right to purchase the building at fair market value if • Lyon became insolvent or • control of Lyon changed hands • Presumably, the value of Bank’s right to purchase at fair market value was limited by the price of Bank’s Options to Repurchase Donald J. Weidner

Possibilities if Bank Does Not Exercise Its Options • If Bank does not exercise its options to renew the building lease: • Lyon would remain liable for the substantial rents required by the ground lease; and • Lyon would still control the building. • “This possibility brings into very sharp focus the fact that Lyon, in a very practical sense, is at least the ultimate owner of the building. If [Bank] does not extend, the building lease expires and Lyon may do with the building as it chooses.” • That is, in this situation, there is no promise that Lyon will be repaid its $500,000, with or without interest. 2. If Bank extends the building lease by exercising all the lease renewal options: says the IRS, “the net amounts payable . . . would approximate the amount required to repay Lyon’s $500,000 investment at 6% compound interest.” Donald J. Weidner

Basic Possibilities Summarized • Bank Exercises Its Options to Renew Its Lease of Bldg. • Lyon gets a return of its investment, plus approximately 6%, no more • Bank Walks Away at the End of the Base Lease Term • At that point, Lyon has not gotten back any of its investment, much less a 6% return, and could get less or more • Bank Exercises one of its Options to Purchase • Lyon gets a return of its investment plus 6%, no more • Bank Exercises its Right to Purchase if Lyon becomes insolvent or has a change of control • Although formally at fair market value, the price presumably is informed by Bank’s Options to Purchase, in which event Lyon gets a return of its investment plus 6%, no more • The Property Is Condemned • Lyon gets return of investment plus 6%, no more Donald J. Weidner

District Court Permitted Lyon to Claim Depreciation Deductions • District Court rejected the argument that Bank was acquiring an equity through its rental payments • Even though the rent payments reduced the balance owed to N.Y. Life and hence the cost of the Bank’s option to purchase • Concluded that rents were unchallenged and reasonable throughout the period (fair value for possession and not to purchase an equity). • Concluded that the option prices, negotiated at arms-length, represented fair estimates of fair market value on the option exercise dates • rejecting any negative inference from the fact the option prices were the amounts needed to (a) pay off N.Y.Life Loan + (b) pay $500,000 + 6%. • Concluded that Bank would acquire an equity only if it exercised an option to purchase • which it found highly unlikely. • Concluded that Lyon had mixed motives, including the desire for the benefits of a “tax shelter.” Donald J. Weidner

Eighth Circuit Reversed the District Court • Eight Circuit held: Lyon was notthe true owner • Therefore, Lyon was not entitled to depreciation deductions. • Property rights are analogous to a “bundle of sticks,” and “Lyon ‘totes an empty bundle’ of ownership sticks:” • Lyon’s right to profit from its investment was circumscribed by Bank’s option to purchase at a price equal to Lyon’s investment, plus 6% thereon, plus the unpaid balance on the N.Y.Life mortgage; • That is, Bank had the option to get title to the building back by treating Lyon as a second mortgagee @ 6% • The prices of Bank’s options to purchase did not take into account any appreciation in the value of the building, even from inflation; • Hence, Lyon had fewer rights than the normal owner of a commercial building Donald J. Weidner

Eighth Circuit Reversal (cont’d) • Lyon’s “empty bundle” (cont’d) 3. Any amount realized from destruction or condemnation in excess of the NY Life mortgage and return of Lyon’s $500,000 plus 6% would go to Bank rather than to Lyon; and • That is, Bank got all of any equity through amortization and/or appreciation 4. The building rent during the base term was equal to debt service and hence gave Lyon zero cash flow; and 5. Bank retained control over the building through its: • a) options to purchase the building, • b) options to renew its lease of the building, and • c) ownership of the site. • In summary, Bank had virtually all of the benefits and burdens of ownership of the building and Lyon merely got a tax shelter for 11 years. Donald J. Weidner