Download

1 / 26

260 likes | 284 Vues

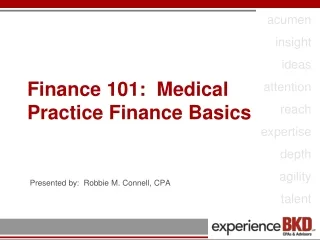

Finance 101: Medical Practice Finance Basics. Presented by: Robbie M. Connell, CPA. Agenda. Standard Practice Management Reports Industry Benchmark Data Basic Financial Overview. Practice Management Reports. Accounts Receivable (A/R) Aging Summary By Payer By Provider Denials Report

E N D

Finance 101: Medical Practice Finance Basics Presented by: Robbie M. Connell, CPA

Agenda • Standard Practice Management Reports • Industry Benchmark Data • Basic Financial Overview

Practice Management Reports • Accounts Receivable (A/R) Aging • Summary • By Payer • By Provider • Denials Report • Activity by Provider & Location • Top CPT Codes

Benchmarks • Days in Accounts Receivable • Entry Lag – Avg number of days from encounter to charge entry – 0-48 hours • Charge Entry to date of bill release to Clearinghouse/Payer – 24-72 hours • Denial Rate – Less than 4% • Industry Overhead Comparison

Distribution of A/R * Texas Specific Data Median %s used Source: MGMA Report, Cost Survey: 2014 Report Based on 2013 Data

Overhead as a % of Total Medical Revenue * Texas Specific Data Median %s Used Source: MGMA Report, Cost Survey: 2014 Report Based on 2013 Data

Staffing per FTE Physician Median FTEs Used Source: MGMA Report, Cost Survey: 2014 Report Based on 2013 Data

Other Useful Benchmarks • Percentage of insurance verified – 98% • Number of patients cleared (demographic & insurance data necessary for claims processing prior to visit – 90% • Error rates due to front-end billing – Less than 2% • Time of Service Collections • Copayments – 100% • All other – 75% • Follow-up notes documented on the account – < 30-45 days • Identification and return of unidentified or overpayment refunds – < 60 days • Date of charge entry to date of claim release – 0-72 hours • Claims Submission – Daily Source: “The Physician Billing Process: 12 Potholes to Avoid in the Road to Getting Paid” by Deborah Walker Keegan, PhD, FACMPE; Elizabeth W. Woodcock, MBA, FACMPE, CPC; and Sara M. Larch, MSHA, FACMPE

Purpose of Accounting • Accounting helps you understand where you have been, so you can decide where you are going • Information systems, which measure, process and communicate information, is useful for decision makers

Definitions • Asset – Something you own • Cash • Accounts Receivable • Charges vs. Net Adjusted Collectible Charges • Property, plant & equipment • Liability – Something you owe • Accounts Payable • Long-term equipment loans • Equity – The difference between the two above. • Assets – Liabilities = Equity

Financial Statements – The Big 3 • Balance Sheet • Income Statement • Cash Flow Statement

Visual summary – Financial Statements Reporting of Business Activity Balance Sheet Financial condition at a point in time Balance Sheet Financial condition at a point in time Income Statement Summary of activity for a period of time Statement of Cash Flows Summary of activity for a period of time End of Year December 31, 2015 Beginning of Year January 1, 2015

Basis of Accounting • Cash Basis • Income is recognized when cash is collected • Expense is recognized when cash ispaid • Accrual Basis • Income is recognized as it is earned • Expense is recognized as it is incurred

Balance Sheet The balance sheet will tell you what the company owns (its assets) and what it owes (its liabilities) and what is left over for the owners (equity) Key Points • Snapshot at a fixed point in time • Not necessarily current market values • Current financial health of the company • Focus on the quality of the assets – e.g. is the company sitting on a pile of cash - or is everything sitting in past due receivables?

Income Statement Shows a company’s performance over a period of time – i.e. how did a company earn its money last year? Key Points • Also referred to as a “Profit and Loss” or “Statement of Operations” • Useful for determining performance before or after an event – e.g. after the addition of a new physician or the opening of a new location

Cash Flow Statement Shows a company’s sources and uses of cash during a period of time Key Points • Quickly tells you how a company is using its cash or funding its day-to-day operations • Rarely does “net cash flow” equal “net income”

Questions? Robbie M. Connell, CPA Manager / BKD, LLP 210-341-9400 rconnell@bkd.com