Download

1 / 45

460 likes | 893 Vues

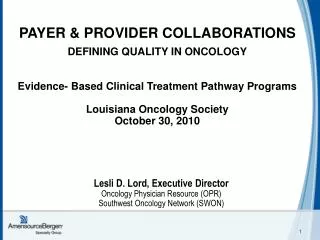

PAYER & PROVIDER COLLABORATIONS DEFINING QUALITY IN ONCOLOGY Evidence- Based Clinical Treatment Pathway Programs Louisiana Oncology Society October 30, 2010. Lesli D. Lord, Executive Director Oncology Physician Resource (OPR) Southwest Oncology Network (SWON).

E N D

PAYER & PROVIDER COLLABORATIONS DEFINING QUALITY IN ONCOLOGY Evidence- Based Clinical Treatment Pathway Programs Louisiana Oncology Society October 30, 2010 Lesli D. Lord, Executive Director Oncology Physician Resource (OPR) Southwest Oncology Network (SWON)

Pathway Programs Making Headlines In Treating Cancer, Insurer Tries New Way to Pay Docs <www.onlinewsj.com>, Marketplace, Oct. 20). Implementation of Pathways: Payers to Share Savings with Compliant Groups (Oncology Business Review, Sept. 2010) Cut Out The Middleman (Community Oncology, July 2010) Controlling The Cost Of Care Through Pathways A look at how two health plans have integrated physician-developed clinical pathways into their networks (BioTechnology Healthcare, April 2009)

Agenda • Introductions • Current Challenges • Pathways MI Case Study • Market Overview • Payer Requirements • Common Objective • Program Highlights • Louisiana Opportunity • Oncology Medical Home • Q & A Additional Case Studies: • CRC & Lung Case Studies • Hydration Model – Quality Initiative

Current Challenges • Physicians • More complex & rapidly evolving diagnostic and therapeutic landscape • Increasing financial stress • More expensive therapeutic options • Federal and private sector reimbursement changes/reductions • Increasing patient numbers • Appropriate reimbursement terms with health plans • Payers • Increase in the utilization and price of cancer drugs and biologics • Cost reduction strategies raise administrative burdens for providers (and payers) without improving quality or patient/provider satisfaction • Need to decrease variability in oncology treatment patterns • Need to define, measure, and report quality of care

Cancer Treatment in Peril Curative “adjuvant” therapy now applies to more disease states and often includes 4-6 months of chemotherapy in addition to surgery Breast, NSCLC, Colon, Bladder Acceleration of expensive new technologies in past 10 years New therapies are much more expensive than previous options Abraxane, Eloxatin Emergence of high-priced biologics (Herceptin, Avastin, Rituxan) Additive, do not replace other therapies Standard of care is increasingly moving to “maintenance therapy” where no definitive length of therapy has been proven Cancer is turning into a chronic disease Patients living with cancer longer allowing for multiple treatments More visits per patient/more infusions per patient Baby Boomers are the final factor: Entering age bracket where prevalence is 10x Living longer due to medical advances increases likelihood that they will eventually be diagnosed with cancer Shortage of oncologists

Chemo Delivery Chain Community based oncology practices have created a highly efficient and patient-centric drug delivery system Contract directly with mfg for best price Order drugs from wholesale distributor Drug inventory MD sees pt, reviews labs, adjusts Pharm / RN admin regimen Nurses educate patients Nurses administer regimen Drugs are billed to payer Same day Same place Same staff

Cancer Costs Growing Rapidly © 2009 The Advisory Board Company

Cancer Care Today Detection and confirmation Imaging Pathology Treatment Surgery Chemotherapy and biologics Radiation Supportive Care White and red cell growth factors Anti-nausea / vomiting Bone health Pain management Adverse Events Hospitalizations/ED visits Palliation Hospice Pain management Survivorship Cost Variability

Provider Trends Permission granted to reproduce for Chicago, IL meeting by Oncology Metrics

0 Question Asked of Payers:Which of the Following Care Management Changes are you Contemplating for Outpatient Oncology in the next 1-2 years? (Select all that apply) How Do We Know Pathways Are Coming? • Population-based / Risk Sharing • Pathway initiative • Reimbursement reduction • Preferred drug formulary • Increase preauthorization requirements • Specialty pharmacy Source: Chicago Meeting – September 24-26, 2010 PROPRIETARY & CONFIDENTIAL

Payer Requirements Decrease Variability & Cost Increase Predictability Better Outcomes Success to a payer means: Addressing outliers Adherence to pathways Decreasing cost trends Limit lines of therapy Prospective data and decision support Regional or state network representing adequate payer specific market share and significant physician participation Evidence-based approach to guidelines and pathways Integrated technology solutions developed for all participating practices

MI Case Study Program Objective: To increase quality and cost effectiveness through the implementation of standard, evidence-based, oncology clinical pathways Participation: 190+ Oncologists (community and academic practices) in Michigan Year One Highlights: Clinical pathway compliance required for breast, colon, lung cancer (70%) and supportive care (80%) Up-front participation reward of $5,000 paid per participating physician Adjusted fee schedule for generic products Gain sharing opportunity for participating physicians Quality initiative contract is held by the physician group

Initiative / Payer Negotiations: Jan-July 2009 Steering Committee: August 2009 Program Launch September 2009 Introduced Program to attendees- MSHO Annual Meeting Sept – Oct 2009 Town Hall Meetings Dec 2009 Initial Enrollment Deadline January 2010 Program Implementation – Start Date Feb – March 2010 Workflow / Implementation / Webinars April 2010 Initial check distribution for payment of participation award June 2010 Users Conference & Q1 Compliance Review MI OPR / BCBS Pathway Implementation Timeline

MI Pathway Vision Year 2: Lymphoma Myeloma Renal Ovarian Prostate OPR Vision: Patient-Centered Oncology Medical Home Move focus from drug reimbursement to case management Expand clinical pathways Explore pathways for diagnostics Fund decision support systems Pay for quality QOPI® accreditation Manage end of life care Create RN case management codes

Market Overview • US Oncology / Innovent • Current Programs • Pilots: United, Anthem Wellpoint • Aetna: National Contract • P4 Healthcare (recently acquired in June 2010 by CAH) • Current Programs • Care First (mid Atlantic states) • Capital Blue Cross (PA) • BCBS of TN • OncoMed • White Bagging Specialty Pharmacy • Removes the Buy and Bill Model • Pilot • Medicare Advantage Plans in Massachusetts PROPRIETARY & CONFIDENTIAL

Market Overview (cont.) • New Century Infusion Solutions • Integrated Single Specialty Provider (ISSP) • Medical, Radiation/Technical and Drug Components • Assumes full capitation and global risk management. • Current Programs • Medicare Advantage Plans in Florida • CCE Cancer Clinics of Excellence • Nationwide Pathways Program • Pilot: Anthem Wellpoint • United Healthcare • Testing Pilot “Episode Program” (4-6 practices) with Bundled Payments PROPRIETARY & CONFIDENTIAL

Common Objective Develop a collaborative approach between payers and providers to increase quality and cost effectiveness through the implementation of standard, evidence-based oncology clinical pathways

Patient-Centric Quality Initiative • Provider driven and actionable on a small/regional scale • Customizable, adaptable and simple • Affordable, sustainable and economically mutually beneficial • Sophisticated technology and informatics solutions • Compliance and reconciliation process

Pathway Program Highlights • Stepwise process mapped out for (X) years • Pathways locally developed by physician community • All pathways are supported by clinical evidence • Pathways Guided by: 1st Efficacy 2nd Toxicity 3rd Costs • Clinical trials and hospice are considered on pathway • Pathways are reviewed and modified quarterly (if needed) or PRN • Standard pathways for year 1 could include lung, breast, and colon and additional pathways added in year 2 and beyond • Quality initiative with payer will provide alignment of appropriate incentives • Diagnostics and end of life (EOL care to follow)

Adjuvant Breast Cancer Clinical PathwaysJune 2010 • EP = Emetogenic Potential based on Hesketh Scores (1-5) • FN < 17% = Risk of Febrile Neutropenia is less than 17% with the associated regimen and appropriate management should be considered • FN ≥ 17% = Risk of Febrile Neutropenia is greater than 17% with the associated regimen and appropriate management should be considered • Adjuvant: Low Risk (Node Negative, Her2Neu Negative) • Chemotherapy: • Adriamycin (doxorubicin) Cytoxan (cyclophosphamide) EP=5; FN<17% • Doxorubicin 60mg/m2 IVP D1 • Cyclophosphamide 600mg/m2 IV D1 • Cytoxan (cyclophosphamide); Methotrexate; 5-FU (fluorouracil) EP=5; FN<17% • Taxotere (docetaxel) Cytoxan (cyclophosphamide) EP=5; FN≥17% • Docetaxel 75mg/m2 IV D1 • Cyclophoshamide 600mg/m2 IV D1 Clinical Trial: Screen patient for clinical trial. Check www.clinicaltrials.govfor available clinical trials Best Supportive Care and/or Hospice: Consider supportive care options and Hospice when appropriate.

Cost Savings • Specific Drivers • Conversion to generics (where appropriate) • Taxanes • Anti-emetics • Biologics • Limit lines of therapy to agreed-upon pathways • Standardization • Elimination of outliers • Improve outcomes • Reduce errors • Reduce hospitalization • Validation of Quality Care in Community vs. Inpatient Setting

Community Oncology vs. Hospital Overall Metastatic Breast Cancer Agents Source: Xcenda Consulting, AmerisourceBergen Specialty Group; April 14, 2010 HEADLINE: HIGHMARK PREPARING FOR REIMBURSEMENT CHANGE…. A billing change being considered by the University of Pittsburgh Medical Center will triple the cost of chemotherapy (an increase of $120M when Oncologists begin billing on a hospital outpatient basis instead of a Community office visit basis) without improving the quality of care, Highmark President and CEO Dr. Ken Melani said Friday. Source: Pittsburgh Business Times, August 23rd, 2010.

Example-Aligned Incentives Example: J9265 generic 30 mg billed 10 units/cycle • Cost: $80.00 • Current payment: $232.28 • Difference: $152.28 J9264 brand billed 400 units/cycle • Cost: $3,396.00 • Current payment: $3,816.00 • Difference: $420.00 If the same margin can be realized with J9265 as J9264 then practice profitability increases, payer drug spend decreases, and patient out-of-pocket is lowered

alignment of appropriate incentives Models Utilization Management Pathway Program Oversight Prior Auths Diagnostics Management Fees Accountable Care Organization Neutralize Margin Difference E&M Generics v Brand Oncology Medical Home Per Pathway Stipend/Fee Pay For Performance Per Patient Stipend/Fee Annual Participation Fee Gain Share on Savings % of Cost Savings Shared

Example – Gain Share Scenario Example: X% * of Post-Pathway Savings paid to Practice *Based on pathway compliance (100%-X%) of Post-Pathway Savings ultimately saved by Payer Source: Cote, Bryan. Oncology Business Review. September 2010 PROPRIETARY & CONFIDENTIAL

Quality is the Measurement of Success • Implemented clinical pathways supported by evidence for top cancer diagnoses • Developed model for the oncology patient medical home (pathways, diagnostics, technology, quality outcomes and EOL • Prospective economic modeling completed for each pathway • Revised basis for payment of fee schedule (targeted) products or unique model for alignment of incentives to participate • Measurement and reconciliation methodology to validate model • Monitor and report quality outcomes to payers • Increase quality and cost effectiveness utilizing standard, evidence-based oncology clinical pathways • Decrease variability and increase predictability of care

Closer to the Medical Home • Patient-centered oncology medical home • Integration and coordination for patient treatment • Clinical pathways • Diagnostics • Technology • Quality outcomes • End of life care

LOUISIANA MARKET • 25 Community Oncology Practices • Approx. 75 Oncology Physicians

Role of ION Solutions / ABSG Promote payers’ interests of keeping patient in community setting Support: Regional/state collaboration Physician involvement Payer outreach Collaborative pathway decisions Transparency Commitment: Technology Prospective and retrospective measurement tools to validate commitments to payers Consultative experience ABSG companies’ expertise and resources Payer contracting Pathway cost modeling

Benefits of Collaboration Increased participation and adherence with community buy-in Trusted Compliance, Monitoring, Reporting Physicians will be good stewards of their state’s healthcare dollars No external 3rd parties mandating the physician’s cancer care process Savings and gain share remain in the local healthcare system

CASE STUDY: CRC • Background: • 2010 Incidence of ALL Cancers in LA = 20,950 • 2010 Incidence of CRC Cancer in LA = 2,060 • Assume 80% are treated in community setting =1648 Data Evaluated: • EMR data from 19 large community oncology clinics • Over 170 doctors in system • Evaluated all treatments for CRC patients for 2009 • Evaluate number of regimens used in 2009 to number of regimens use if Pathways followed (reduce variability) • Assigned “costs” based on 2010 130% ASP model

CASE STUDY: CRC • Results: • 4412 patents with CRC were treated in 2009 • There were 60 different regimens used to treat 2 or more patients • There were 176 patients (4%) that received some form of a “one off” regimen. This is down from 7.2% in 2008 • 199 (4.5%) patients were treated on a clinical trial

CASE STUDY: CRC Regimens used for 80% of Patients Responsible for 65.1% of costs ** Put into bottom 20% for cost analysis

CRC Regimens used for 20% of Patients Responsible for 34.9% of costs *** Put into Top 80% for cost analysis

Cost Analysis Results: • Results: • 4412 patents with CRC were treated in 2009 • Total “cost” of 1 cycle of chemo for All of the available 60 regimens was $564,178 • Total “cost” for 4412 pts. receiving 3 cycles of the 60 prescribed regimens was $75,527,720

LA Pathways Estimates: • 18 total regimens available (Adj + Metastatic) • Total “cost” of 1 cycle of chemo for the available 18 ION regimens is $151,870

LA Comparison Estimates: Current Practice (60% on Pathway) **Cost of “Off” Pathway is calculated by removing “On” pathway regimens (18); then dividing the total cost of the remaining regimens by 42 (number of remaining regimens)

LA Comparison Estimates: 70% Adherence Estimated Savings: $570,570

LA Comparison Estimates: 80% Adherence Estimated Savings: $1,137,682

Lung Cancer Cost Analyses Results There is a $5,883 per patient savings in treating a patient On Pathway versus Off Pathway