Download

1 / 3

30 likes | 98 Vues

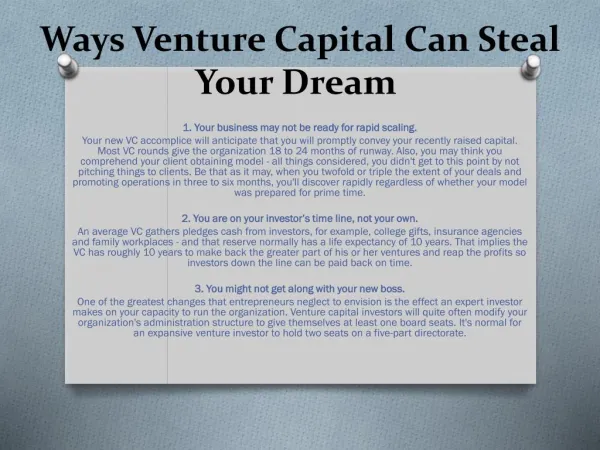

<br><br>1. Your business may not be ready for rapid scaling.<br>Your new VC accomplice will anticipate that you will promptly convey your recently raised capital. Most VC rounds give the organization 18 to 24 months of runway. Also, you may think you comprehend your client obtaining model - all things considered, you didn't get to this point by not pitching things to clients. Be that as it may, when you twofold or triple the extent of your deals and promoting operations in three to six months, you'll discover rapidly regardless of whether your model was prepared for prime time.<br><br>2. You are on your investor’s time line, not your own.<br>An average VC gathers pledges cash from investors, for example, college gifts, insurance agencies and family workplaces - and that reserve normally has a life expectancy of 10 years. That implies the VC has roughly 10 years to make back the greater part of his or her ventures and reap the profits so investors down the line can be paid back on time.<br><br>3. You might not get along with your new boss.<br>One of the greatest changes that entrepreneurs neglect to envision is the effect an expert investor makes on your capacity to run the organization. Venture capital investors will quite often modify your organization's administration structure to give themselves at least one board seats. It's normal for an expansive venture investor to hold two seats on a five-part directorate.<br><br>4. Your VC doesn’t want anything but a grand slam.<br>Being a venture capital investor is intense business. Out of each 10 ventures made, maybe a couple must have a leave sufficiently huge to pay for the other eight or nine speculations that neglect to meet desires. Shikhar Ghosh, a senior teacher at Harvard Business School, has ascertained that an incredible 90 to 95 percent of venture-supported startups neglect to beat their announced projections<br><br>5. You are putting your payout at risk.<br>At the point when VCs put resources into your organization, they structure the speculation with favored stock. This class of stock conveys a wide range of inclinations for the venture investor, including a liquidation inclination. This directs how much cash must be come back to the investor before you, as a typical shareholder, see a solitary penny.<br><br>Ebranding11119swpa<br><br>Contact: - Prof. Prakash Bhosale<br>Phone/WhatsApp: 9892416734<br>Email: - ebrandingswpp@gmail.com<br>Website: - http://dissertationwritingediting.com/<br>Time: - 10 AM TO 7.30 PM IST, Monday to Friday<br><br>

E N D

Ways Venture Capital Can Steal Your Dream 1. Your business may not be ready for rapid scaling. Your new VC accomplice will anticipate that you will promptly convey your recently raised capital. Most VC rounds give the organization 18 to 24 months of runway. Also, you may think you comprehend your client obtaining model - all things considered, you didn't get to this point by not pitching things to clients. Be that as it may, when you twofold or triple the extent of your deals and promoting operations in three to six months, you'll discover rapidly regardless of whether your model was prepared for prime time. 2. You are on your investor’s time line, not your own. An average VC gathers pledges cash from investors, for example, college gifts, insurance agencies and family workplaces - and that reserve normally has a life expectancy of 10 years. That implies the VC has roughly 10 years to make back the greater part of his or her ventures and reap the profits so investors down the line can be paid back on time. 3. You might not get along with your new boss. One of the greatest changes that entrepreneurs neglect to envision is the effect an expert investor makes on your capacity to run the organization. Venture capital investors will quite often modify your organization's administration structure to give themselves at least one board seats. It's normal for an expansive venture investor to hold two seats on a five-part directorate.

4. Your VC doesn’t want anything but a grand slam. Being a venture capital investor is intense business. Out of each 10 ventures made, maybe a couple must have a leave sufficiently huge to pay for the other eight or nine speculations that neglect to meet desires. ShikharGhosh, a senior teacher at Harvard Business School, has ascertained that an incredible 90 to 95 percent of venture-supported startups neglect to beat their announced projections 5. You are putting your payout at risk. At the point when VCs put resources into your organization, they structure the speculation with favored stock. This class of stock conveys a wide range of inclinations for the venture investor, including a liquidation inclination. This directs how much cash must be come back to the investor before you, as a typical shareholder, see a solitary penny. Ebranding11119swpa Contact: - Prof. PrakashBhosale Phone/WhatsApp: 9892416734 Email: - ebrandingswpp@gmail.com Website: - http://dissertationwritingediting.com/ Time: - 10 AM TO 7.30 PM IST, Monday to Friday