Download

1 / 11

140 likes | 426 Vues

UNDERSTANDING THE FOREIGN TAX CREDIT. JULY 14, 2011. BY MITCHELL SORKIN CPA MBA PFS Smallberg Sorkin & Company LLP Mitchell@smallbergsorkin.com 212 736-1711. Foreign Tax. Not deductible for AMT or States. Does it qualify. NO.

E N D

UNDERSTANDING THE FOREIGN TAX CREDIT JULY 14, 2011 BY MITCHELL SORKIN CPA MBA PFS Smallberg Sorkin & Company LLP Mitchell@smallbergsorkin.com 212 736-1711

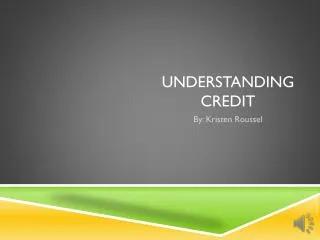

Foreign Tax Not deductible for AMT or States Does it qualify NO Not eligible for credit May be deductible YES Classify into two baskets .Dividends, interest Capital gains CERTAIN DIVIDENDS FROM DISCS DISTRIBUTION FROM FOREIGN FSC FOREIGN TRADE INCOME IRC 923 (B) DIVIDENDS FROM NONCONTROLLED SEC 902 CORPS SHIPPING INCOME FINANCIAL SERVICE INCOME Wages and Business income HIGH W/H TAXES Income PASSIVE GENERAL Calculate Regular and AMT Yes Any Unused Credit Carryback Carryforward Check to see if deduction is better No yes No form 1116 required Is IRC 904(j) Election available for Individuals No Fully deductible Check effect on other credits

SEPARATE INCOME CATEGORIES • Passive income as defined under IRC 945(c) Passive • High withholding taxes Passive or General • Financial service income Passive • Dividends from non controlled Section 902 Corporations (10/50 Corporations) Passive or General • Shipping income General • Certain DISCS dividends Passive • Foreign trade income IRC 923 (b) Passive • Distribution from Foreign Sales Corporations (FSC) Passive • All other income not included above- General Limitations General • Treaty Income – Separate form 1116

RECENT PROVISIONS • Two baskets since 2007 • Unused foreign tax credits get carried back one year and carried forward 10 years. • Multinational corporations that are affiliated can elect to allocate interest on a • worldwide basis as if all members of the group were a single corporation. The effect • would be not to allocate US interest expense to foreign source income unless their debt to • asset ratio is higher in the US than in foreign countries effective 2008. • For limitation purposes, the US tax will be reduced by non refundable personal credits • (other than the adoption credit or child tax credit ) effective 2007. • Foreign taxes are no longer limited to 90% of the AMT tax. • IRC 901(m) provides for the denial of a Foreign tax credit with respect to Foreign income not subject to US Taxation by reason of a covered asset acquisition. • IRC 904(d)6 provides for the separate application of the foreign tax credit rates with respect to certain items resourced under treaties (Separate Foreign 1118). • IRC 960(c) provides for a limitatin with respect to IRC 956 inclusion.

WHAT THE BROKER DOES NOT TELL YOU BUT YOUR ACCOUNTANT SHOULD KNOW • Must hold the dividend paying stock or any other property that produces income, gain or interest • for at least 16 days prior to the taxpayer’s right to receive the income and own the property for 31 days. • Recipients receiving dividends from preferred stock must hold the security for at least 46 days during the • 90 day period beginning 45 days before the dividend date if the dividends paid are based on more than • 366 days. • To the extent the recipient is obligated (under a short sale or otherwise) to make payments regarding • positions in substantially similar or related property, the Foreign Tax Credit “FTC” will not be eligible. • Does not apply to any active conduct of business in a foreign country in that property. • Accrued foreign taxes are translated at exchange rates for the year the taxes relate to. Taxpayers • can elect to use the exchange rate on the date of payment. • Can claim foreign tax credits on amount paid to Puerto Rico and possessions. (similar to Mexican flat tax) • Tax exempt entities do not benefit from paying foreign taxes. • 8. Can still take the deduction even if you do not qualify for the credit.

SPECIAL SITUATIONS • 10/50 Corporations: Dividends received from a non controlled company, but one that is owned 10% or more • will report the income category based on Earnings and Profits “E & P” attributed to that category over the • “E & P”. Therefore, can allocate taxes paid by the foreign corporation attributed to the dividend. • Partnerships that own 10% or more of foreign corporations can pass through the deemed paid taxes. • Foreign corporations owned 10% by US corporations are entitled to a deemed paid foreign tax credit. • High taxed income on passive income must be treated as general limitation where the foreign taxes after • deducting expenses exceed the highest US tax rates (does not apply to passive income that is • financial service income). • If you are a less than 10% limited partner or a less than 10% S corporation shareholder who does not actively • participate in the management of the S corporation, you can assign the foreign income exclusively to the • passive income category on your distributive share of foreign source income and deductions. This takes • preference over the instructions on the K-1s Reg. Section 1.904-5(h) 2. Line 16 of Schedule K-1 (form 1065). • If the foreign taxes are more than the income tax at the preferential rate, you may need to reduce the income • to reflect the reduced rates i.e. dividends and capital gains, but there is an exception, otherwise need to • modify foreign source dividends by .4286%. • Adjustment exception for Form 1040 filers: You qualify for the adjustment exception if you meet both of the • following requirements: • a. Line 7 of the Qualified Dividends and Capital Gain Tax Worksheet does not exceed: • i) $209,250 (if married filing jointly or qualifying widower) • ii) $104,625 if married filing separately • iii) $171,800 if single or • iv) $190,550 if head of household. • b. The amount of your foreign source capital gain distributions plus the amount of your foreign source qualified • dividends, is less than $20,000. For this purpose, ignore any capital gain distributions or qualified dividends • you elected to include on Form 4952.

US partners who control a foreign partnership must file for 8865. If not filed but furnishes all the information by the due date need to reduce by 10% all foreign taxes. If failure continues further reductions will be required under IRC 6038 ( c ). • Similar rule for form 5471 as 7 above. • Even if you elect to take the foreign tax credit you may still deduct foreign taxes not eligible for the credit i.e. Boycott countries. • Boycott countries would still prepare the foreign tax form but stop on line 16

EXAMPLES: Example 1- Individual Mr. CPA has earnings of $100,000,mortgage interest of $10,000, charitable contributions of $7,000, real estate taxes of $20,000, NYS income taxes of $5,000, federal tax of $10,000 and employee business expenses of $15,000. He received $29,500 in dividends, of which all were qualifying and $20,000 was from a corporation that withheld $4,000 in UK taxes. He is filing as head of household and has a 12 year son. He also received $2,000 of interest income and paid $2,000 of interest expense from his brokerage account. Example 2 With 904 (j) election Example 3 Same facts as 1 above, but he received a K-1 from partnership that generates $500 of passive income of which all was considered from foreign sources and paid $100 in foreign taxes. Example 4- Corporation Corporation has income of $100,000, expenses of $50,000. In addition, it has dividends from foreign sources of $1,000 of which $200 was withheld.

PLANNING • 904 (j) Election • If taxpayer has less than $300 ($600 jointly) of foreign taxes from qualified passive income and only has • foreign income from passive income sources can elect to be exempt from the “FTC” limitation. • Applies to individuals only. No estates or trusts. Cannot use “FTC” carryovers or carrybacks in election • year. This is a yearly election. • Deduction or Credit • Can switch off every year. Can change election before end of a special 10 year period IRC 6511(d)(2) or • 6511(c). • Paid or Accrued Election • Once elected must accrue taxes for all subsequent periods. If not paid within two years you need to • recalculate the credit. The taxes accrued must be within your taxable period. • Check the Box Election • Income and foreign taxes will pass through to the members. • Treaty Countries • Invest in countries who have reduced foreign tax withholding. • Tax Exempt Entities • Avoid investing in high foreign withholding countries with tax exempt entities i.e. IRA, pension, • charitable entities, because they receive no tax benefits. • Allocation of expenses • Can increase or decrease foreign source income by direct and indirect allocation of expenses. Can • now allocate all of charitable contributions to US source income. Mortgage interest is allocated to foreign • source when total foreign income is $5,000 or more. Can elect to apportion all other interest to US source if • foreign income is $5,000 or less. For corporations see Reg. Section 1.861-8

FTC and AMT • When computing the FTC, you must perform two calculations • a. Using the regular taxable income. • b. Using the alternative taxable income • c. Can have different carryback or carryover amounts for AMT and regular tax purposes. • Section 911 – Earned Income Exclusion • Cannot take the foreign tax credit on income that is excluded as the result of the IRC Section 911 exclusion • which is $91,500 in 2010. If you earned more than $91,500, you can take credit on the excess. • Creditable Taxes • a. Must be on income, war profits and excess profits • b. Not all taxes paid resulting from oil and gas income are creditable. • c. Domestic corporations owning foreign subsidiaries are allowed a deemed paid foreign tax credit based • on qualified taxes paid by other subsidiaries that pays out dividends or deemed to receive dividends from • an affiliate group or a partnership. Must own 10% or more of the stock. The amount of the deemed • credit is added to the taxable income. • d. Limit on taxes paid to boycott countries. • e. Credit is reduced if taxpayer fails to provide information that is required by owning controlled • foreign businesses.

QUESTIONS: • 1. Can a simple trust make a IRC 904 (i) election? • 2. When will foreign taxes on dividends become subject to the general limitation bucket? • Never • When the foreign tax credit rate is more than the regular tax rates. • When the foreign tax credit rate is lower than the regular tax rates. • 3 How many years can a Foreign tax credit carryback go back? • 4 Can you ever take both the foreign tax credit as a credit and as a deduction on the same tax return • 5. If you elect IRC 904 (j) treatment will the prior foreign tax credit carryover be lost?