Reserving for Title Insurance

2004 Casualty Loss Reserve Seminar Paul J. Struzzieri, FCAS Milliman, Inc. September 14, 2004. Reserving for Title Insurance. Outline. Introduction to Title Insurance Financial Reporting Issues Actuarial Challenges & Methods. I) Introduction to Title Insurance. Types of Policies

Reserving for Title Insurance

E N D

Presentation Transcript

2004 Casualty Loss Reserve Seminar Paul J. Struzzieri, FCAS Milliman, Inc. September 14, 2004 Reserving for Title Insurance

Outline • Introduction to Title Insurance • Financial Reporting Issues • Actuarial Challenges & Methods Milliman

I) Introduction to Title Insurance • Types of Policies • Coverage • Unique Issues • Markets • Distribution • Reinsurance Milliman

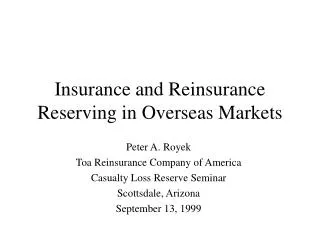

Types of Title Insurance Policies • Purchase Mortgages • Lender Policy – based on $ amount of loan • Owners Policy – based on $ amount of purchase • Refinance Mortgages • Lender requires new policy • Owners keep original policy Milliman

Purchase vs. Refi Mortgages Milliman

Coverage • Lender’s and owner’s interests are protected • Cost to cure the defect; plus defense costs • Common title problems: • Defects, liens, easements – catch during search • Hidden hazards – undisclosed heirs, forged deeds • Unmarketability of title • Defalcations Milliman

Coverage Example #1 • Young couple buys home from widow (whose husband died without a will). • Widow’s son shows up and claims a share of the home. • Title insurance pays the missing heir the value of his share. Milliman

Coverage Example #2 • Just prior to closing, a prior lien is discovered. • For example, a paid but unreleased mortgage. • Purchaser can decide not to close based on this discovery. • Title insurance policy will respond if unmarketable. Milliman

Issues Unique to Title Insurance • Loss is “incurred” prior to policy issuance • No policy expiration date how to earn premium? • Goal of title search & examination = loss elimination • High expense ratios (90%+); low loss ratios (4-10%) Milliman

U.S. Market Share Milliman

International Markets • Canada • Australia • Europe Milliman

Distribution Channels • Agency Business (86%) • Independent Agents – including attorneys (59%) • Owned Agencies (27%) • Direct (14%) Milliman

Reinsurance • Typically excess of loss • Larger title insurers reinsure the others • Assumed and ceded = offset each other Milliman

II) Financial Reporting Issues • Financial Reporting • Form 9 • Statement of Actuarial Opinion • Categories of Statutory Reserves • Reserve Testing Milliman

Financial Reporting • Form 9 = Statutory Annual Statement • Schedule P • By Policy Year • By Report Year • Statement of Actuarial Opinion – since 1996 Annual Statement • Opine on Schedule P reserve, NOT booked reserve Milliman

Categories of Booked Reserves • Known Claims Reserve • Statutory Premium Reserve (SPR) = “Unknown” Claims • SPR Functions as Unearned Premium Reserve • Formula = Amount & Take-down Pattern • Supplemental Reserve Milliman

Reserve Testing • Compare Schedule P Reserve against Known Claims Reserve + SPR • Schedule P includes Known Claims, so really testing SPR vs. IBNR • If SPR > IBNR, book SPR • If IBNR > SPR, book SPR + Supplemental Reserve Milliman

Industry Reserves@ 12/31/03 • Known Claims = $556M • SPR = 3,258M Total = $3,814M • Schedule P = $2,741M Milliman

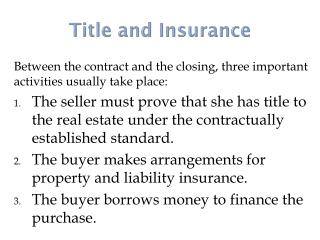

III) Actuarial Challenges • Title insurers do not know the number of policies in-force! • Correlation between calendar year loss emergence and mortgage rates • Refi policies have lower loss ratios than original title policies • Commercial vs. residential policies • New products Milliman

Actuarial Methods – Loss Development • Paid and incurred loss development triangles from Schedule P • Industry composite data available • Historical patterns can be distorted • Drop in interest rates leads to refi’s • When lender policy is refinanced, original policy is extinguished. • Try to adjust pattern Milliman

Actuarial Methods – Expected Loss Ratio • Expected Loss Ratio for refinance policy is lower than original policy • Policy Year with high refinance % expected to have lower loss ratio Milliman

Refi Percentage vs. Title Loss Ratio Milliman

Actuarial Methods – Expected Loss Ratio • Econometric modeling of Expected Loss Ratio – variables could include: • Mortgage rates • Refinance percentage Milliman

Actuarial Methods – Cape Cod or Bornhuetter-Ferguson • Combines Expected Loss Ratio and Development Methods. • To calculate Expected Losses, can use: • Premium • Amount of Insurance • Counts & Averages Milliman