Understanding the ACH Process: From Consumer Transactions to Merchant Payments

The Automated Clearing House (ACH) process streamlines transactions between consumers and merchants through a series of steps. On Day 1, the merchant submits a transaction to ACH Direct, which must be received by 4:30 PM PST for next-day processing. On Day 2, the transaction is presented to the RDFI, starting a 48-hour window for payment denial. By Day 3, all returned items must be sent to the Federal Reserve, and by Day 4, the originator's reporting is updated. Finally, on Day 5, funds become available in the originator's account, completing the transaction cycle.

Understanding the ACH Process: From Consumer Transactions to Merchant Payments

E N D

Presentation Transcript

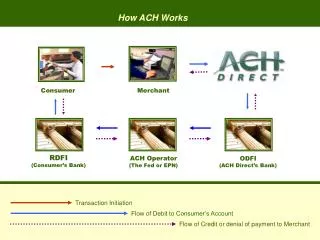

How ACH Works Consumer Merchant RDFI(Consumer’s Bank) ACH Operator (The Fed or EPN) ODFI(ACH Direct’s Bank) Transaction Initiation Flow of Debit to Consumer’s Account Flow of Credit or denial of payment to Merchant

Day 1: Submission Date – originator (merchant) submits transaction to ACH Direct via real-time, batch or items that are scheduled to go out. This is the submit date. To be effective the following day all transactions must be received by 4:30 PM PST. Day 2: Effective Date – early in the morning the transaction is presented to the RDFI (customers bank), the 48-hour period which the banks have to inform the originator that the item did not pay begins. If the account is closed or is invalid, many banks will be able to send out a rejected item notification to the Federal Reserve on this day. Day 3: Deadline for Returns – by the end of this day, all returned items must be sent by the RDFI to the Federal Reserve. Items that rejected in Day 2 are received from the Federal Reserve through the ODFI (ACH Direct’s originating bank). ACH Direct compiles this data and reports it back to the originator. Day 4: Last Day of Returns – the last of the returned items are received and the originators reporting is updated to reflect that. ACH Direct sends a credit to the originator for the items that have cleared. Day 5: Funds Available – originator’s bank receives the credit from ACH Direct and applies it to the originators account. This typically occurs before the bank opens and funds are available immediately that morning.