Second Quarter 2000 Highlights: Key Transactions and Progress Reports

The second quarter of 2000 showcased significant completed transactions with notable companies like NSTAR, Duke Energy, and Northern States Power, each contributing millions in revenue. The future looks promising with expected transactions like new Standard Offer Agreements and continued asset management initiatives. Key focuses include achieving budget goals, enhancing deal flow through a robust Mid-Market team, and establishing effective regulatory coverage. The overall aim is to build robust relationships, expand market presence, and execute strategic initiatives for continued growth in energy trading and management.

Second Quarter 2000 Highlights: Key Transactions and Progress Reports

E N D

Presentation Transcript

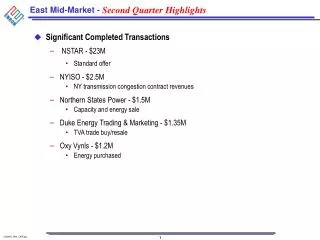

Second Quarter Highlights • Significant Completed Transactions • NSTAR - $23M • Standard offer • NYISO - $2.5M • NY transmission congestion contract revenues • Northern States Power - $1.5M • Capacity and energy sale • Duke Energy Trading & Marketing - $1.35M • TVA trade buy/resale • Oxy Vynls - $1.2M • Energy purchased

Second Quarter Highlights, cont’d. • Future Expected Transactions • New Standard Offer Agreements • NSTAR / CMP / Bangor Hydro • Outsourcing/Asset Management • ERCOT QSE business • Hoosier • Other Full Requirements • City of Columbus • Tolling (Morgan Stanley) • ERCOT Wind Agreement • OPPD Restructure

Hot List Detail Estimated Deal Originator Description Value (000’s) Enron Wind Curry Off-take Agreement $ 8,000 Manitoba Hydro Electric Board Clynes/Sewell Buy Capacity/Energy 250 QSE (EES) Curry Outsourcing 750 Morgan Stanley Swank Gas Tolling 1,500 3Q 00 Total $ 10,500 NSTAR Llodra Standard Offer Agreement $ 5,000 OPPD Clynes/Sewell Restructure Agreement 1,000 Hoosier Dalton Asset Management/Outsourcing 1,000 CMP/Bangor Hydro Wood/Llodra Standard Offer 3,500 4Q 00 Total $ 10,500 Total Deals - 8 $ 21,000

Progress Report - General Initiatives • Establish and meet 2000 budget • Objective: $25 million • YTD status: $30.6 million • Implement complete ongoing account coverage • Monthly, quarterly and annual coverage objectives implemented August 1, 2000 • Increase EOL penetration • Established top 100 customer list (created late June) • Build Deal Flow • YTD status: 26 “significant” transactions • Focus will be on significantly increasing standard product deals • Objective: Build to 150 transactions per quarter by Q1, 2001 • Implement more intensive coverage and transaction orientation throughout group

Progress Report - General Initiatives , cont’d. • Complete Mid-Market team build-out • Build-out complete: see organizational chart • Reviewing business initiatives for additional staffing needs (ERCOT/SPP) • Build strong team dynamics • Empower each team member to build the business - Mid-marketers are closest to the customer and the market • Commercial leads are taking ownership of sub-region by mentoring associates, directing regulatory coverage, focusing on complete account coverage and developing new initiatives • Cross-leveraging expertise of team (e.g., Llodra will be on team with Woody to work standard offer with Bangor Hydro and Central Maine Power - Janelle will be group model for generating deal flow) • Mid-Market will closely coordinate with Origination • Mid-Market is working on several initiatives with originators across all regions • Mid-Market and Origination held joint Northeast strategy session • Strategy sessions are to follow for Southeast and Midwest • Implement complete regulatory coverage • Commercial leads have developed coverage strategies for all key regulatory committees and initiatives (e.g., participating in and influencing development of Midwest - ISO, SPP-RTO, ERCOT-ISO and Florida RTO)

Progress Report - Specific Initiatives • Build up markets where there is currently little activity • New York - Working with trading to develop financial trading • PJM - Working to develop positions in both east and west hub (250 MW tolling with Morgan Stanley) • Florida - Working on Ft. Pierce deal: EPMI receives 170 MW call option • ERCOT - Working to close 135 MW wind position with green credits; Rolling out outsourcing (QSE) business to put Enron’s “hands” on more MW’s • Asset management/outsourcing (control/manage 2,000 MW’s) • Outsourcing (QSE) deal with EES in ERCOT - this deal would give Enron view of hourly ERCOT load • Working QSE deals with Oxychem (Gen - 700 MW; Load - 1,000 MW) and Alcoa (Gen. - 1,000 MW; Load - 700 MW) • Hoosier - Displace Williams as asset manager

Progress Report - Specific Initiatives, cont’d. • Full/Partial requirements transactions - Execute 2-3 new deals for at least 2,000 MW’s • Four year NSTAR with 3,700 MW’s peak and 2,000 MW’s of PPA’s • Bangor Hydro (320 MW’s )and Central Maine Power (1,300 MW’s) standard offer service • Cajun Coop - Four member coops are seeking full requirements supplier • Ohio municipalities - Seeking alternative supply and load management services • Transmission Initiatives • Taking positions in TCC auctions (NY-ISO) • Analyzing transmission availability for generation site development (may need to hire outside consultants) • Reviewing “defensive” transmission plays for existing facilities • Ongoing analysis of transmission out of existing plants • Ongoing analysis of transmission paths to serve difficult positions (OPPD, MSCPA)

Progress Report - Specific Initiatives, cont’d. • Industrial Initiatives • Mid-market is coordinating with industrial services • Making initial calls on ERCOT industrials - initial push will be via QSE play • Leverage business around Enron generation assets • Reliant/Constellation: swap TVA for PJM East and West capacity and energy

Coverage Metrics - 3Q 2000 (Implemented August 1) (Monthly) (Quarterly) (Annual) Number of Sub-regions Accounts Plan Actual Plan Actual Plan Actual Northeast NEPOOL 201 31% 15% 33% 11% 36% 0% NY 123 13% 11% 38% 19% 49% PJM 90 17% 12% 22% 9% 61% 2% Southeast SERC/FRCC 344 11% 7% 20% 4% 69% SPP 494 21% 17% 10% 2% 69% 6% ERCOT 180 36% 29% 17% 4% 47% 5% Midwest MAPP 658 12% 9.0% 28% 2% 60% MAIN 170 15% 9.4% 25% 6% 60% ECAR 451 10% 1.6% 15% 75% Total Accounts 2,711 Performance Metrics, cont’d.

Headcount Headcount 1999 June 2000 Actual Actual 0 1 2 5 1 6 0 1 1 10 4 23 Executive Directors Managers Senior Specialist Analysts, Associates and Other Total Headcount * Janelle Scheuer will focus on “jump starting” trading relationships inside NYPP and industrial business for the entire Northeast Region. John Llodra and George Wood will continue to manage long-term relationships in both NEPOOL and NYPP.

Enron North America East Mid-MarketQuarterly Business Review August 18, 2000