Financial Management

This guide from the National Apartment Association Education Institute covers critical aspects of apartment investment and financial management. It details the benefits of investing in apartments, various financing methods including mortgages, and effective budget management strategies. Learn about key financial metrics, investment risks, and how to meet owners' investment goals while maximizing revenues. Ideal for aspiring and current apartment property supervisors seeking to enhance their financial acumen and gain insights into effective property management practices.

Financial Management

E N D

Presentation Transcript

National Apartment Association Education Institute Certified Apartment Property Supervisor Financial Management

Restrooms Breaks Lunch Cellular Phones Smoking Housekeeping

Apartment Investment Basics Mortgages, Financing & Taxes Managing the Budget Process Getting to the Bottom Line Analyzing Monthly Financial Statements Valuing Apartment Investments Maximizing Revenues Learning Outcomes: Financial Management

Introductions • Name • Company • Number of Units • How Many Years In the Business • How long have you been a multi-site supervisor?

Participate fully. Help us stay on track. Be on time Ask questions Offer ideas and opinions as perceptions Have fun. Ground Rules

Let’s Check Our Homework! HOMEWORK REVIEW

Apartments have produced a higher total return, with less variance, than the average of all property types in the portfolios of pension funds and other large investors. Apts. All Prop. 1984-2004 9.3% 7.6% Total annual return National Council of Real Estate Investment Fiduciaries Why invest In Apartments?

Business Risk Financial Risk Liability Risk Inflation Risk Interest Rate Risk Property Damage Risk Obsolescence Risk Apartment Investments and Risk

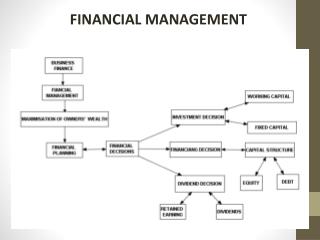

Getting a specific rate of return Generating regular cash flow Refinancing Renovating or retrofitting the property Acquiring new properties Selling existing properties ?????? What are the Owner’s Investment Goals?

Keep the owner well informed Factor the owner's goals into all key financial activities Provide incisive and timely financial analysis Recommend strategies and tactics Take decisive and effective steps Assess portfolio growth Communicate The Financial Strategy

Need for additional funds to purchase or develop an apartment community. Use a loan in order to free money to diversify their investments. Take advantage of the tax benefits that allow mortgage interest deductions and asset depreciation. Enjoy the benefit from financial "leverage" Why investors Choose Mortgages

The use of borrowed funds to increase overall purchasing power • Positive Leverage means borrowing money at a lower interest rate than what the asset yields • Negative Leverage is borrowing money at a higher interest rate than what the asset yields Leverage is a unique element to real estate investments, not present in investments like stocks and bonds What is Leverage?

The document that establishes the existence of debt between a lender and a borrower. Key provisions: • Amount borrowed • Rate of interest • Payment due dates • Loan maturity date (when all remaining amounts are due) • Reference to the real estate providing security for the loan • Specific terms relating to defaults, grace periods, and early payments • Details on how payments will be applied, usually in this order: • (1) to late payments, fees, and penalties; • (2) to interest; and • (3) to principal Mortgage Notes

Pay monthly amounts for property insurance, real estate taxes, and if required, mortgage insurance premiums (PITI) • Pay all other taxes, assessments, charges, and claims that have priority over the mortgage. • Have hazard insurance coverage • Keep the property in good condition • Get the lender's approval for any new owner • Assignment Clause Mortgage Clauses: Protect Lender

Non-Recourse Clause Prepayment Rights Loan Assumption Conditions Mortgage Clauses: Protect BORROWER

Fixed Rate Loans • Variable Rate Loans • Balloon Loans • Bullet Loans • Other Loans • Rollover Loans • Construction and Takeout Loans • Gap Loans • Wrap Loans Types of Mortgage loans

Economic Conditions Inflation Default Risk Interest Rate Risks Legislative or Regulatory Risks Mortgage Financing Risk Factors

Commercial Banks Life Insurance Companies Pension Funds Investment Banks Mortgage Brokers Private Sources Syndications Sources of Mortgage Financing

Government Sponsored Enterprises (GSE’s) • FNMA – Fannie Mae: Federal National Mortgage Association • FHLMC - Freddie Mac: Federal Home Loan Mortgage Corporation • FHA – Federal Housing Administration • LIHTC –Low Income Housing Tax Credit aka Section 42 Government Financing Resources

LTV – Loan to Value: • Expressed as % • Formula: Loan amount/Property Value = LTV • Lenders prefer under 80%, may be 60% • DCR – Debt Coverage Ratio • Expresses the property’s ability to repay the loan • Formula: NOI/ADS (Annual Debt Service)=DCR • The closer the DCR is to 1 the riskier the loan Loan Analysis

Federal, state, and local taxes significantly affect the return on investment available to the owner. • A baseline understanding of the tax laws and practices affecting apartments will increase financial literacy—and gain greater insight into how to help the owner achieve property or portfolio goals. Note: Tax laws are complex, and professional tax advice always needs to come from a tax attorney or tax accountant. Don’t give tax advice! Taxes

Property taxes are one of the two largest expenses for an apartment community. • They provide the major source of funds to provide local government services used by apartment communities. • Property taxes—and sometimes water and sewer fees imposed by local government—usually have a lien priority, even over mortgages. Property Taxes

Depreciation or Cost Recovery • The Capital Gains Tax Rate • 1031 Exchange • The Concept of Basis • Adjusted basis • Recoverable basis • Original basis Tax Benefits and Risk

A budget is an itemized summary of estimated income and expenses for a defined period of time, most often one year. Provides the "window" on property operations Principal source of information relating to a property's financial performance. There are three types of budgets: • Lease-up budgets • Operating budgets • Renovation or modernization budgets What is a Budget?

Budgets monitor a property’s performance By regularly comparing actual income and expenses to the budget, income shortfalls and expenses overruns can be spotted and corrective measures taken. May also be used to evaluate the performance of personnel The Importance of A Budget

A budget begins with the owner's operational and financial goals. Does the owner want to: • Receive a specific rate of return? • Generate cash flow? • Renovate or upgrade a property? • Sell a property? Goals must be understood BEFORE beginning to prepare the annual operating budget, Budget Goals

Extrapolation: • Estimating a number based on information you already know. • May be used for income or expense categories • Annualization: • Estimating a number by averaging year to date income or expense and multiplying to make a full year. • Care must be taken to exclude one time or unusual occurrences • Better to use historical data for the same months in the prior year instead. Two Budgeting Techniques

Start early Use property personnel Gather meaningful, specific supporting documentation that must accompany budgets Supply property team with the right budget tools Consider holding a budget workshop Distribute copies of the budget Tips for Supervising the Budget Process

Accounting deals with the entire system for providing financial information—from the design of the systems through its operation to interpretation of the data. Bookkeeping is the routine, day-to-day recordkeeping that’s a necessary part of accounting. Accounting vs. Bookeeping

Accrual basis accounting. • All income and expenses in the period they are earned or incurred, regardless of when they are actually received or paid. • Gives a more realistic and controlled picture of net operating income in the period, and is the most common type of accounting used in multifamily residential management. • Cash basis accounting. • All income and expenses when they are actually received or paid, which causes widely fluctuating numbers. • Cash basis accounting may give a distorted picture of profitability at a given point in time. • Is it more important to know when rent is incurred, or just noting the cash received when it was paid? Accrual vs. Cash Basis Accounting

Gross Operating Income (GOI) - all the money a property records, including rent and other income. Net Operating Income(NOI) gross income less operating expenses. Operating Income

Fixed Expenses Variable Expenses Where should smart managers focus? What are the two largest expense categories as a percent of Gross Potential Rent (GPR)? Operating Expenses

Often called the operating statement or profit and loss statement, Measures performance over a given period of time. Key indicator of a property’s financial position Defines progress, trends, relationship to the competitive market place, and the continuing ownership strategy. The Income Statement

Shows the financial status of a property at a moment in time. • Assets are all the cash on hand, the things the property owns and the accounts receivable. • Liabilities are the debts and obligations owed, such as loans and the accounts payable at the property. • Equity is the sum of Assets less Liabilities The Balance Sheet

Gross Potential Rent, or GPR • Total rent that would be generated from the property if all the units were occupied. • GPR combines the sum of occupied units at current lease rates, plus vacant units at market rates. • All income and expenses are measured and evaluated as a percent of GPR. • Gross Potential Rent is NOT Market Rent • Often called scheduled rent, which is the total annual income you’d receive if 100% of all units were occupied and paying market rents. Gross Potential Rent (GPR)

A variance from Market Rent due to the Lease Rents residents pay at the time of move-in. • As market rents go up, loss to lease increases; as market rents are lowered, the loss to lease is reduced. • There will always be a gap between market rent and gross potential rent. WHY? • Market Rent less Gross Potential Rent) / Market Rent = % Loss to Lease Loss/Gain To Lease (LTL)

Total value of rent loss from vacant units • Cost of concessions given • Collection loss as a result of writing off bad debt • Total amount of rent loss from any non-revenue units. Vacancy, Concessions, and Collection Losses (VAC)

Effective gross income (EGI) is the amount of gross potential rent (GPR) less vacancy, concession, and collection loss (VAC). Effective gross income is also called net rental income or total rental income. It represents only rental income. Formula: GPR - VAC = EGI. Effective Gross Income (EGI)

Other income (OI) is any money collected for items other than rent. • Includes collections from Laundry vending deposit forfeits parking amenity charges late fees pet fees application fees administrative fees cable lease premium fees • Other income can add up to an additional 5% to 10% of the total property income. Other Income

Total amount of all money the property collects. Also known as Total Revenue or Total Income. GOI is the sum of the Effective Gross Income (EGI) and other income (OI). Formula: EGI + OI = GOI. Gross Operating Income (GOI)

All expenses, fixed and variable, that are paid to manage the property. Typical expense categories are: Salary and personnel costs Insurance Taxes Utilities Management fees Administrative costs Marketing Contract services Repairs and maintenance Note: Capital expenses and replacement reserve payments (if required) are not typically considered operating costs. Operating Expenses (OE)

Net operating income (NOI) is gross operating income (GOI) less operating expenses (OE). NOI is the critical number on the operating statement. Income producing properties are valued based on a derivative of NOI Formula: GOI - OE = NOI. Net Operating Income (NOI)

Similar to net operating income except that capital expenses (including replacement reserve payments) and debt service are subtracted. • Usually represents the property’s distributable cash. • A cash flow statement is another measure used to show financial performance. • Statements can include before-tax cash flow (BTCF) or after-tax cash flow. CASH Flow (CF)

Capital expenses or capital expenditures (CE) are large property expenditures. • They include non-recurring major expenses, such as replacing a roof, adding a swimming pool, and otherwise improving the property in ways intended to add to its life. • Capital expenses have a “useful economic life.” • They are depreciated over an "expected" life rather than in a single year. Capital Expenses (CE)