Download

1 / 24

240 likes | 319 Vues

Uncertainty Over Bush-Era Tax Cuts. Presented by: Louis Tommasino. Louis Tommasino, CPA A Professional Corporation. Extensive experience in: Tax services Accounting and Business Consulting Trust and business planning Business Management services Start-up companies

E N D

Uncertainty Over Bush-Era Tax Cuts Presented by: Louis Tommasino

Louis Tommasino, CPA A Professional Corporation • Extensive experience in: • Tax services • Accounting and Business Consulting • Trust and business planning • Business Management services • Start-up companies • Trained and Experienced Staff • Please see staff bio in handout material • Own Practice since 1996 • Individuals, trusts and estates • Small businesses • Industries include Entertainment, Medical practices, Biotech, Retail; Restaurants and Marble Wholesalers, and Real estate • Bachelor of Science in Business Administration from Arizona State University – licensed CPA in AZ & CA

Overview • Bush Tax Cuts • Costs of Extending selected tax cuts • Sunsets facing individuals • Impact: Suggested Strategy • Capital Gains / Dividends Sunsets • Impact if current law is not extended • Impact of sunsets illustrations • Other sunset provisions • Compliance and Audit issues

Bush Tax cuts • Tax cuts from the 2001 Economic Growth and Tax Relief Reconciliation Act of 2001 were due to expire in 2010 • Extended for two years rather than made permanent • Had an impact on all taxpayers, individuals, businesses and estates • Reduced individual tax rates, preferred rates for qualified dividends, capital gains etc.

Costs of Extending selected tax cuts • Bush Era tax cuts $2.84 Trillion* • AMT Patch $804 Billion* • Tax extenders $839 Billion* • Payroll tax cuts $117 billion** *Through 2022 **Through 2012

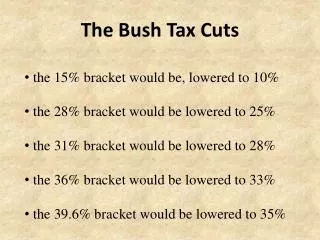

Sunsets facing individuals • Income tax rates for individuals • Current rates are the following: 10, 15, 25, 28, 33, and 35 • Unless extended the rates will increase to 15, 28, 31, 36, and 39.6

Sunsets facing individuals • Unless Congress acts all will effectively experience a tax hike • Top rate will jump from 35 to 39.6 percent • Lowest rate of 10 percent is eliminated • 2% employee side payroll tax cut due to expire in 2012

Sunsets facing individuals • All workers will feel the affect of the increase of the social security wage base increase to $113,700 • President Obama recommends: • Increase 33 and 35 rate schedule to 36 and 39.5 • For taxpayers with income over $200,000, single and $250,000 for married filing joint taxpayers • Individuals that anticipate higher income tax rates after 2012 should explore shifting the timing of income or deductions

Impact: Suggested Strategy • Acceleration techniques include: • Billing earlier • Selling appreciated property • Avoiding installment sales that defer gain • Accelerating bonuses • Fund pension plan 401k to max contribution level • May want to consider Roth conversions in 2012 • Pass-throughs will be hit hard • Profits are passed through to their individual owners • Business owners might consider C-Corporation status • max rate at 35% • probability that corporate rates will decrease in the future • Consider rental real estate investments

Capital Gains/Dividends Sunsets • Reduced tax rates on qualified capital gains and dividends scheduled to sunset after 2012 • 2010 tax relief act reduced max tax rate of 15% on adjusted net capital gains through 2012 • Taxpayers in the 10-15% tax brackets are eligible for a 0% tax rate on qualified capital gains through 2012

Capital Gains / Dividends Sunsets • Capital gain rates scheduled to revert to 20%, (10% for taxpayers in the 15% tax bracket) • The 25% tax rates for collectibles and recaptured Code Sec 1250 gain respectively are scheduled to continue unchanged after 2012 • Ordinary tax rates paid on short-term capital gains are unchanged

Capital Gains / Dividends Sunsets • Five-year holding period for Capital Assets after 2012 • Lower capital gain rates for property held for more than 5 years. • Long-term capital gain rates for property held for more than 5 years will be taxed at 18% (8% for taxpayers in the 15% bracket) • Special 18% rate applies if • Taxpayer acquired the asset in 2001 or later • Has held the asset for more than five years • Sells the asset after December 31, 2012

Impact if current law is not extended • Working with your financial advisor accelerating the sale of capital assets prior to end of year • Take your capital losses in 2013 to offset capital gains at the higher rate • Taxpayers who have entered into installment sale agreements may want to accelerate their payments in 2012 • Hold vs Sell decisions • Taxpayer may find it advantageous to sell or to Harvest a tax loss

Impact if current law is not extended • Risk of higher tax rates can be mitigated by considering holding assets for 5 years or longer • Taxpayers subject to investment interest limitation may want to elect their capital gains to be treated as investment income using form 4952

Impact if current law is not extended • Aging or severely ill taxpayers should consider holding their assets until they can pass the assets to their beneficiaries • Assets get a step-up in basis from a decedent’s estate • Taxpayers are cautioned not to let the tax-tail wag the economic dog • All of the above tax reduction techniques involve economic risk as well as time value of money • Carefully weigh and evaluate consequences

Impact of Sunsets • #1: Assume a couple, two children eligible for the child tax credit, filing a join return and taking the standard deduction, with $130k wage income, $10,000 net capital gains, and $2,000 dividend income. Their tax liability for 2013 (all figures are estimates and, for illustration, assume no inflation adjustments between 2012 and 2013): • No sunset: ………………. $19,485 tax due for 2013 • Full sunset: …………….. $25,898 tax due for 2013 • Difference: ……………… $6,413

Impact of Sunsets • #2: Assume a couple, no children, filing a joint return and taking the standard deduction, with $300k wage income, $50,000 net capital gains, and $5,000 dividend income. Their tax liability for 2013 (assuming for illustration, no inflation adjustments between 2012 and 2013): • No sunset: …………….. $77,721 tax due for 2013 • Full sunset: …………… $89,934 tax due for 2013 • Difference: ……………. $12,213

Impact of Sunsets • #3: Assume a single filer, no children, taking the standard deduction, with $70k wage income, $5,000 net capital gains, and $1,000 dividend income. The individual’s tax liability for 2011 (assuming for illustration, no inflation adjustments between 2012 and 2013): • No sunset: …………. $11,992.50 tax due for 2013 • Full sunset: ……….. $13,606.50 tax due for 2013 • Difference: ………… $1,614

Other Sunsetting Provisions • EGTRRA and JGTRRA provisions are not the only tax benefits scheduled to expire after 2012 (or that are already expired after 2011). Among these provisions (not an exclusive list) are the following: • Payroll tax cut • 100% bonus depreciation • Enhanced Code Sec. 179 expensing • Research credit • State and local sales tax deduction • Teacher’s classroom expense deduction • Exclusion for charitable contributions of IRA proceeds • Parity for transit benefits • Mortgage insurance premium deduction • Cancellation of mortgage indebtedness exclusion for personal residence • Energy tax incentives

Compliance and Audit issues • New Registration Requirements for Paid Tax Preparers what it means to you and the professional

Compliance and Audit Issues • All preparers of tax returns including Attorneys, CPA’s, EA’s, and licensed tax preparers must: • Register with the IRS • Attain a PTIN number • Pay an annual user Fee of $63 • User fees of approximately $46 Million to be used for funding of new agency of IRS called the Return Preparer Office

Compliance and Audit Issues • IRS office will supervise the preparation of tax return preparers. • IE fraud in the earned income tax credits and tax preparers receiving refunds from erroneous return filings • Example: The AZ Tax Shelter case

Compliance and Audit Issues • Mandate to file returns electronically • Software determines preparers and clients with errors etc. • Tax-preparers determine if client information is valid or requires additional inquiries • Increasing cost to Taxpayer • Role of the preparer has changed • Taxpayer advocate -> Taxpayer compliance officer