Standard Costs

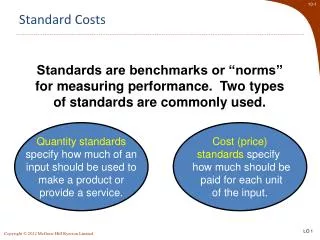

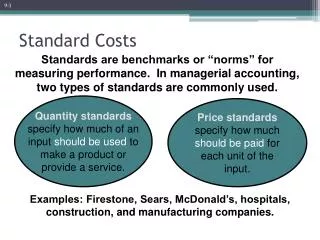

9- 1. Standard Costs. Standards are benchmarks or “norms” for measuring performance. In managerial accounting, two types of standards are commonly used. Quantity standards specify how much of an input should be used to make a product or provide a service.

Standard Costs

E N D

Presentation Transcript

9-1 Standard Costs Standards are benchmarks or “norms” formeasuring performance. In managerial accounting, two types of standards are commonly used. Quantity standardsspecify how much of aninput should be used tomake a product orprovide a service. Price standardsspecify how muchshould be paid foreach unit of theinput. Examples: Firestone, Sears, McDonald’s, hospitals, construction, and manufacturing companies.

Deviations from standards deemed significantare brought to the attention of management, apractice known as management by exception. 9-2 Standard Costs Standard Amount DirectMaterial DirectLabor ManufacturingOverhead Type of Product Cost

Takecorrective actions Identifyquestions Receive explanations Conduct next period’s operations Analyze variances 9-3 Variance Analysis Cycle Prepare standard cost performance report Begin

I recommend using practical standards that are currently attainable with reasonable and efficient effort. Should we useideal standards that require employees towork at 100 percent peak efficiency? 9-4 Setting Standard Costs Engineer Managerial Accountant

9-5 Standard Cost Card A standard cost card for one unit of product might look like this:

Materials price variance • Labor rate variance • VOH rate variance 9-6 Price and Quantity Variances Variance Analysis Price Variance Quantity Variance • Materials quantity variance • Labor efficiency variance • VOH efficiency variance

Actual Quantity Actual Quantity Standard Quantity × × × Actual Price Standard Price Standard Price Price Variance Quantity Variance 9-7 Price and Quantity Variances (AQ × AP) – (AQ × SP) (AQ × SP) – (SQ × SP) AQ = Actual Quantity SP = Standard Price AP = Actual Price SQ = Standard Quantity

I’ll start computingthe price variancewhen material ispurchased rather than when it’s used. I need the price variancesooner so that I can betteridentify purchasing problems. You accountants just don’tunderstand the problems thatpurchasing managers have. 9-8 Direct Materials Variances – Points of Clarification

Purchasing Manager Production Manager 9-9 Direct Materials Variances – Points of Clarification Materials Quantity Variance Materials Price Variance The standard price is used to compute the quantity varianceso that the production manager is not held responsible forthe purchasing manager’s performance.

Mix of skill levelsassigned to work tasks. Level of employee motivation. Quality of production supervision. Production Manager Quality of training provided to employees. 9-10 Direct Labor Variances – Points of Clarification Production managers areusually held accountablefor labor variancesbecause they caninfluence the:

I think it took more time to process the materials because the Maintenance Department has poorly maintained your equipment. I am not responsible for the unfavorable laborefficiency variance! You purchased cheapmaterial, so it took moretime to process it. 9-11 Direct Labor Variances – Points of Clarification

Larger variances, in dollar amount or as a percentage of the standard, are investigated first. 9-12 Variance Analysis and Management by Exception How do I knowwhich variances to investigate?

Advantages 9-13 Advantages of Standard Costs Promotes economy and efficiency Management byexception Enhances responsibilityaccounting Simplifiedbookkeeping

PotentialProblems 9-14 Potential Problems with Standard Costs Emphasizing standardsmay exclude otherimportant objectives. Favorablevariances maybe misinterpreted. Standard costreports maynot be timely. Emphasis onnegative mayimpact morale. Continuous improvement maybe more importantthan meeting standards. Invalid assumptionsabout the relationshipbetween laborcost and output.

9-15 Recording Material Variances

9-16 Recording Direct Labor Variances

9-17 Cost Flows in a Standard Cost System • Inventories are recorded at standard cost. • Variances are recorded as follows: • Favorable variances are credits, representing savings in production costs. • Unfavorable variances are debits, representing excess production costs. • Standard cost variances are usually closed out to cost of goods sold. • Unfavorable variances increase cost of goods sold. • Favorable variances decrease cost of goods sold.