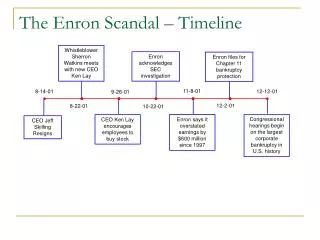

The Enron Scandal – Timeline

390 likes | 5.14k Vues

Enron acknowledges SEC investigation. Enron files for Chapter 11 bankruptcy protection. CEO Ken Lay encourages employees to buy stock. Enron says it overstated earnings by $600 million since 1997. Congressional hearings begin on the largest corporate bankruptcy in U.S. history.

The Enron Scandal – Timeline

E N D

Presentation Transcript

Enron acknowledges SEC investigation Enron files for Chapter 11 bankruptcy protection CEO Ken Lay encourages employees to buy stock Enron says it overstated earnings by $600 million since 1997 Congressional hearings begin on the largest corporate bankruptcy in U.S. history CEO Jeff Skilling Resigns The Enron Scandal – Timeline Whistleblower Sherron Watkins meets with new CEO Ken Lay 11-8-01 8-14-01 12-12-01 9-26-01 12-2-01 8-22-01 10-22-01

Widespread public outcry regarding role of auditing profession in detecting fraud Public Oversight Board announces its dissolutionAICPA issues calls for a new “reporting model” AICPA Board passes a resolution to support a ban on auditors of public companies from providing internal audit and financial systems design and implementation services Questions: Is there need for a new reporting model? If so, what would it look like? Is the AICPA Board’s resolution necessary? Should such services be prohibited? Is such a prohibition designed to address independence in fact or appearance, or both? Should auditors be allowed to perform consulting services for audit clients? How can auditors improve fraud detection? The Enron Scandal - Implications

Enron has underscored the importance of some basic auditing issues: Assessing management integrity and its influence on the control environment Understanding the client’s core business strategy and risks Scrutinizing related party transactions (RPTs) Questions: How do auditors assess integrity? Why do auditors need to understand a client’s business strategies and objectives? How can auditors be certain that they know of all RPTs? The Enron Scandal – Auditing

Other basic auditing issues: Auditing estimates included in the financial statements Corroborating management representations Obtaining a management representation letter Questions: Why is it so important to carefully evaluate estimates included in the financials? To what extent must auditors corroborate management’s representations? What is the value of the management representation letter? The Enron Scandal – Auditing

Created as an autonomous body to oversee and report on the self-regulatory programs of the SEC Practice Section Voted to terminate its existence no later than March 31, 2002 The SEC has proposed an oversight body dominated by public members who are not affiliated with the profession Questions: Who will fulfill the POB’s function? What implications will the Board’s dissolution likely have for the profession’s self-regulating status? Who should have oversight authority over the profession? Dissolution of the POB

The CPA Vision project was the impetus behind the credential The credential had ardent supporters and pundits 40 percent of the AICPA membership voted 62.7 percent against 37.3 percent for Questions: Why do you think that only 40 percent of the members voted? What are the pros and cons of a global credential open to non-CPAs such as the one proposed by the AICPA? The Global Credential Vote

The ASB has recently issued two new standards: SAS No. 95, Generally Accepted Auditing Standards SAS No. 96, Audit Documentation SAS No. 95 – establishes authoritative standing of various publications SAS No. 96 – replaces the term “working papers” with “audit documentation” and provides further guidance on necessary audit documentation New Statements on Auditing Standards

Fraud Task Force The ASB recently voted to issue the task force’s draft of a revision of SAS No. 82 as an exposure draft The proposed SAS provides more guidance related to the detection of material misstatements due to fraud The ED is slated for release in March, 2002 Risk Assessment Task Force The task force is continuing to refine a draft of a revised audit risk model that increases the focus on understanding business risk More emphasis will be placed on understanding the client and its business environment A draft of the new standard is expected soon! “On the Horizon”