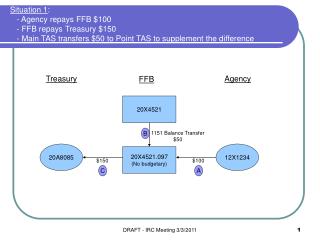

Budgetary management

Budgetary management. Competency units SITXFIN004A manage finances within budgets SITXFIN005A prepare and monitor budgets. objectives. These competency units provide the underpinning knowledge required for competency based assessment of the following elements: Allocate budget resources

Budgetary management

E N D

Presentation Transcript

Budgetary management Competency units SITXFIN004A manage finances within budgets SITXFIN005A prepare and monitor budgets

objectives • These competency units provide the underpinning knowledge required for competency based assessment of the following elements: • Allocate budget resources • Monitor financial activities against budget • Identify and evaluate options for improved budget performance • Complete financial and statistical reports • Prepare budget information • Prepare budget • Finalise budget • Monitor and review budget

Budgetary management According to hotel management consultant Kirby Pane, managing expenses is amongst the most important tings a manager does. • The most central elements of effective expense management are proactive rather than reactive. • The first step in expense management is budgeting

Budgetary management • A manger can look at the many historical expenses, anticipate what they will be in the future and put that in the budget. • Now while that gets the budget done, it does not actually help manage the expense. • A manager needs to look at the historical expense, analayse what the components are , decide how it can be improved and finally implement those changes.

Strategic plans • All business including hospitality business must have a vision and identifiable goals and objectives • The overall plan to achieve this vision is called a strategist plan. • The plan of action to achieve the strategist plan is called the strategy. • All other plans rest beneath this framework.

budgets • A budget is a financial plan with measurable outcomes • The term budget is derived from the French “bougette” which is used to refer to a list of all planned income and expenditure items.

budgets • Budgets are route maps ofr a busienss to reach its destination. • A budget is not much use unless it is monitored and used as a measure of control. • A budget should be realistic and take into consideration all possible variables. • If prepared accurately, it is an excellent diagnostic tool for management.

Budgetary control • Budgets and control go hand in hand, one is not effective without the other. • Budgetary control involves • Checking actual income and expenditure at regular intervals • Including financial commitments in all appropriate documentation to ensure accurate monitoring

Budgetary control continued • Identify and reporting deviations, and all the significance of deviations, according to enterprise policy • Investigating appropriate options for more effective management of deviations • Advising appropriate personnel of budget status in relation to targets within agreed time frames.

What is budgeting? • A budget is a forecast in monetary or quantitative terms, and budgeting is the term used for the process of forecasting. • A budget translates management policies and goals into measurable outcomes • Strategic plans outline the long term goals of an organisation and provide direction. • The allocate limited resources to achieve optimum results in quantifiable terms

All plans cost money • Either directly or indirectly • While the ultimate goal of a business is to make profit. • Even non for profit organisations, costs need to be recovered in order to remain in operation.

What is budgeting? • The process of planning, allocating resources and identifying measurable outcomes is called budgeting.

Hospitality budgeting • Hospitality budgeting requires a good understanding of the hospitality industry and the sectors within it, as well as of external factors which impact upon the hospitality business. • This can include economic conditions, future trends, competition and cost structures.

Budgets allow for the monitoring of deviations, and for management to initiate corrective action if necessary. • This involves variance analysis of both actual results and forecasted figures, and will be discussed in more detail later.

What is budgeting? • Budgets provide organised estimates of revenue, expenditure, staffing levels and equipment needs, with departmental breakdown for different time periods. • They can be used as a communication tol by management to express long term and short term objectives, and to ensure responsibility and accountability.

Budgets can also serve as a menas of control. • Budgets can be seen as “ living documents” as they can be regularly revised and changed to manage both internal and external deviations to ensure operational profit is still achieved.

Information sources for budget preparation may include • Performance data from previous periods • Financial proposals from key stakeholders • Financial information form suppliers • Particular pricing • Customer and supplier research • Competitor research • Industry trend • Planned local events or issues • All which may have an impact on the budget, management policies and procedures, enterprise budget, preparation guidelines, declared commitments in given areas of operation, and grant funding guidelines or limitations.

In summary • In summary budgeting, • Allows for evaluation of business decisions • Sets targets in quantifiable terms • Provides benchmarks • Is a good means of communication • Serves as a summary sheet for a large amount of information • Allows for controls and checks at various intervals • Ensures accountability by managers and departments

Budgeting techniques • Three budgeting techniques • Zero based budgeting • Rolling budgets • Activity based budgeting

Zero based budgeting technique • This is a technique that sets all the budgets to zero at the beginning of the year or period • All the relevant departments then need to justify all of their expenditures. • Money is allocated to departments based on the merit of their request. • Pros- money could be allocated more realistically • Cons – micro management by operations

Rolling budget technique • Annual budgets typically forecast income and expenditure for 12mths. They remain unchanged and serve as a statistic financial measure. • Whereas rolling budgets in contrast provide updated and adjusted figures. • Quarterly or monthly updates are prepared according to current financials based on actual performance.

Activity based budget technique • This is budgeting based on levels of activity • It shows how costs vary with different rates of output or different levels of sales volumes. • With activity based budgeting costs for each function of an organsiation are established and relationships defined by activities. • This forms a basis for resource allocation. • Information is then used to decide the resources that should be allocated to each activity. • An activity based budget is reliant on historical data nad sales projections and thus not advantageous to new business.

Types of budgets • Budgets are financial management plans with two distinct features • They cover phases of operations and phases of time • They may be classified into different types based on their purpose or their time period. • In hospitality the following budgets based on purpose are commonly found.

Types of budgets • Capital budgets • Operating budgets • Departmental budgets • Cash budget • Master budget

Capital budget • A capital budget relates to items requiring capital expenditure and often requires the allocation of substantial funds to projects. • The measurable outcome is the timely installation of the asset or system within the budget. • A refurbishment, renovation or replacement schedule in a hotel requires the preparation of a capital budget.

Operational budget • An operating budget relates to items of income and expenditure appearing on the operating statement. • For a restaurant , club or hotel the primary income is from sales. • There may also be ancillary sources of income such as interest received, rent received. • Items of expenditure as a result of an ongoing activity represent cost of goods sold, labor and overheads. • The operating budget contains profit projections based on projected income and expenses.

Departmental budget • A departmental budget relates to revenue and expenses of a department for a given period of time, usually one year. • It also projects departmental profit. • Departmental budgets are prepared in larger hospitality establishments where there are several revenue earning departments, eg hotels.

Cash budget • A cash budget is a projection of cash flow in a business. • Payments are made from the cash available. • See figure 16.1 on page 402

Master budget • The master budget is prepared for the entire organization for a one year period and relates to items which appear on the previous four budgets. • It is a comprehensive budget covering all activates of the organization . • It comprises a budgeted operating statement for the ensuring year and a budgeted balance sheet at the end of the year.

The master budget is prepared by the finance department of large hospitality establishments such as hotels or clubs. • It involves collating information relating to the various departments of the operation and provides the general manager and the executive team with a holistic view of the entire operation, as well as with tools for management and decision making.

Strategic plan – long term • A long term budget is a strategic plan • It ranges from 3-5yrs. • Because it contains long term future projections, it needs to be revised and updated annually, so its projections remain realistic. • It provides the business with a planning tool for the future.

Annual budget – operational plan • It is a forecast for a one yr only period.

Performance plan – monthly budget • Incentives for staff can be attached t this type of budget. • Because of its monthly time frame, it provides short term targets which staff can work towards, making corrective action or change possible with little delay. • See figure 16.2 and 16.3 page 404

The budgeting process • The budgeting process is a cyclic process which involves • Assessing market and economic conditions and the strategic plan of the business • Establishing attainable goals in the light of market and economic conditions and the business plan • Allocating resources to reflect enterprise policy • Planning to achieve the established goals • Setting standards, or benchmark, in quantifiable terms and communicating these to all stakeholders • Comparing actual performance with budgeted targets and investigating deviations • Implementing corrective action, if necessary and communicating this information to all stakeholders • Revisiting the budgeting process for continuous improvement

In a large hospitality business with several revenue- earning departments, the formulation of an operating budget requires input from all departmental heads on forecasted revenue and related expenses. • Sales projections need to take into account anticipated trends, competition, market conditions, economic activity and pricing policy, government policy, and historical sales data.

Preparation of the sales revenue forecast is the first step in formulating an operating budget, a departmental budget and a master budget. • Costs are expressed as a percentage a percentage of sales in accordance with industry standards or bench marks • Projected costs deducted form forecast sales revenue give profit projects

The budgeting process • Forecasted food and beverage sales are based on the number of seats available, the number of operating days, the average spend per person and the forecast seat turnover. • See figure 16.4

Variance analysis • Variance analysis can be used for both revenue and expenditure variance • Revenue variance may relate to price or volume or both. • Expenditure variance may relate to price , volume , efficiency or a combination of volume and price. • Variance analysis can best be explained by looking at an actual example.

Budgets need to be realistic to make them work. • Actual data should be measured against budgeted data as soon as possible to check for variance and to initiate corrective action. • Corrective action may involve the introduction of time saving methods and improved systems, the use of computerized systems and staff training and development.

Budget cuts and cost cuts should be made to enhance efficiency and not at the cost of customer service. • A budget is a plan for allocating finite resources to obtain optimum results, funding should be allocated in accordance with a companies strategic business plan and business priorities, and this should be communicated to all relevant employees.

The importance of budgetary control cannot be stressed enough. • Appropriate records and systems should be in place to make budgets work. • Though budgeting is a financial function, communication is the key to its success. • All stake holders should be involved in the planning process and the financial goals and targets should be communicated to staff as they are instrumental in making goals reality

Rectifying budget variance • There are a number of tips for rectifying budget variance. • A drop in actual sales could be rectified by anyone of the following actions or a combination of them. • Areas to investigate would also depend on the nature of the business and the size of the business.

Check if the forecast was realistic in the first place. • Review sales and marketing • Revisit pricing strategies • Look at completion • Assess cashiering controls • Audit record keeping • Introduce innovative ideas to boost sales • Review quality standards • Look out for adverse publicity

If actual cost of goods were more than budget, the areas to investigate would be, • Purchasing • Portion sizes and standardized recipes • Receiving , storing and issue of stock • Wastage in preparation • Deterioration of food and storage conditions • Quality and condition of equipment • Stocktaking accuracy • Need for further training

If labor budgets were too high when compared with budget, it would be necessary to consider • Change in occupancy, covers served or volume of business • Mix of casual and full time staff • Award pay fluctuations • Change in efficiency and productivity • Fostering and optimum usage of staff • Motivation levels of staff • Absenteeism and staff turn over • Need for training • Multi skilling of staff • Occupational, health and safety in the workplace

If there were a deficit in the cash budget, management would need to evaluate • Mix of cash and credit sales • Debt collection period • Credit terms from the suppliers • Strategies to increase cash sales • Time frame for the servicing of debt • Overdraft arrangements with the companies financial institution • Inventory levels and stock tied up, especially wine and liquor • Capital expenditure timelines

Budgets are a planning and diagnostic tool, but they do not provide practical corrective action measures. • It is the responsibility of the hospitality manager to use this tool to manage business effectively.

Other financial and statistical reports • Besides standard budgets, hospitality management records needs to prepare other reports of a financial and statistical nature stemming from budgets. • Actual results can be reported against forecasts in the following reports • Daily weekly and monthly transaction and reports • Income and expense breakdown by department • Occupancy/ turnover • Sales performance • Commission earnings • Yield management

Budgetary tips for managers • Monitor actual income and expenditure against budgets at regular intervals and communicate results to staff • Follow process guidelines and include financial commitments in all documentation. This is required for monitoring and auditioning, and will also assist in accurate presentation of final results • Identify and report deviations to senior management according to organizational policy and significance of deviation • Conduct variance analysis on a regular basis as deemed necessary buy the origination • Analyse reasons for variance, take corrective action and monitor its effectiveness • Communicate budget status in terms of time frames to the management team through financial and statistical reports