Aga Khan Fund for Economic Development

220 likes | 444 Vues

Aga Khan Fund for Economic Development. Small Scale Infrastructure – Presentation overview. AKFED & IPS - overview of global activities IPS Infrastructure portfolio – a brief overview Case Studies – small scale energy projects. January 2006. EXISTING PRESENCE AND NEW REGIONAL INITIATIVES.

Aga Khan Fund for Economic Development

E N D

Presentation Transcript

Aga Khan Fund for Economic Development Small Scale Infrastructure – Presentation overview • AKFED & IPS - overview of global activities • IPS Infrastructure portfolio – a brief overview • Case Studies – small scale energy projects January 2006

EXISTING PRESENCE AND NEW REGIONAL INITIATIVES Canada West Africa Côte d’Ivoire Sénégal Mali Burkina Faso East Africa & Indian Ocean Kenya Uganda Tanzania Rwanda Mozambique Madagascar Central Africa Dem. Rep. of the Congo Middle East Syria South Asia Pakistan Bangladesh Central Asia Tajikistan Afghanistan Kyrgyzstan

Industrial Promotion Services Tourism Promotion Services Media Services Financial Services Aviation Services KEY STATISTICS : AKFED • About AKFED • For-profit agency involved in long-term investments • Difference from typical commercial investor • Over 90 project companies in: • Financial Services • Tourism • Media • Aviation • Industry and Infrastructure • More than 30,000 employees • 16 countries in East, West and Central Africa; South and Central Asia

AKFED’S APPROACH TO DEVELOPMENT • Entrepreneurship promoted with economically sound enterprises in the developing world • Long-term investments with • Strong equity positions • Provision of management expertise • Investments in fragile and complex environments • Prospects of improving the lives of people • Profits entirely reinvested in further development initiatives

INDUSTRIAL PROMOTION SERVICES (IPS) Infrastructure (existing projects) • Power/Water • Azito Energie (Côte d’Ivoire) IPP, 290 MW gas turbines; • Tsavo Power (Kenya) IPP, 75 MW HFO. • Energie du Mali (Mali) water & power concession, 185 MW hydro + diesel; • PamirEnergy(Tajikistan GBAO) power concession, 43 MW hydro. • West Nile Rural Electrification Co (Uganda) 2 MW hydro. • Bujagali Energy (Uganda) 250 MW hydro, $860 million investment. • Telecommunications • Roshan (Afghanistan), 1.6 million subscribers, market leader. • CATD/Indigo/Somoncom (Tajikistan) 500,000 subscribers, market leader. • Seacom – Sub marine cable along Southern African coast to Europe and India • Ports • Mombasa Container Terminal (Kenya) for consolidated cargo.

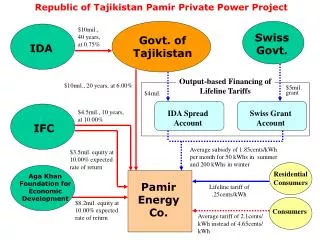

PamirEnergy – Key Facts • Location: Tajikistan • Customer Base: 28,000 (> 95% residential) • Residential Tariff (2007): 0.25 US cents (≤200 kWh) 1.7 US cents • Project costs: US$27 million • Tariff subsidies: US$8.8 million (customer orientated) • Installed capacity: 42 MW • Carbon Credits: 300,000 VERs Khorog receives 24h/7 power in winter (10 hours/day in rest of country)

First Public Private Partnership in the region • GoT willingness and flexibility to support this project • GoT created enabling environment and facilitating the way for private investors • First and only privatization of a state utility in Central Asia • Collaboration of private and public, Government and multilaterals bodies • Creative project financing and innovative use of subsidies for a commercial investment with social orientation • Unique model for replication worldwide (India, Brazil etc.)

KEY CHALLENGES • Harsh mountainous environment (logistics, etc.) • Significant investment yet affordable tariffs • High winter energy consumption yet lowest available energy • Scarcity of affordable alternative energy sources • Extensive area but dispersed and small population • Culture transition towards a ‘modern’ utility • Strong support required from authorities to implement change • No prior culture of payment for utilities • Very high levels of losses (both technical and commercial)

UGANDA – West Nile Rural Electrification Co. Ltd • Innovative structure for rural electrification • 20-year concession • Affordable & Sustainable tariffs through 50% upfront grant to offset investment • Impacts to date • Significant reduction in monthly energy costs • Over 600 new connections • Cleaner and safer sources of energy • Improved education and health • Increased commercial/industrialactivities

West Nile – Key facts • Location: North Uganda • Customer Base: 5,000 (mainly residential) • Residential Tariff: 13.1 US cents • Additional Generation: 3.5 MW Hydro • Project cost: $14.75 million • Capital grant: $8.2 million (reduces tariff to affordable level based on IRR of 15%) • Carbon Credits: 443,000 CERs Customers now receive power 18 hrs/day (compared with around 12 hours throughout the rest of Uganda)

Challenges with Small Infrastructure Projects • Lack of critical mass leads to financial imbalance in the following areas: • Tariffs • Operating costs • Development costs

Mitigation Measures • Acceptance of lower hurdle returns. • Utilisation of “soft-funds through grants, donations, etc. • Use of carbon credits where possible.

Use of soft funds • The use of ‘soft’ funds for projects can allow the project to achieve the following objectives: • become financially sustainable for shareholders; • allow affordable tariffs for the customers; • mitigate development risk (development/early stage costs); • Donors often have restrictions in providing grants to private entities eg off grid remote/rural small HPPs at PamirEnergy.

Subsidy Mechanism – linked to consumption • Subsidy delivered at time of consumption (e.g. Pamir Energy) so becomes part of operating revenue: • Customer invoiced net amount (i.e. before subsidies) • Company receives gross amount (customer payment + subsidy)

Subsidy Mechanism – offset initial investment • Reduce initial capex and hence investment cost to allow net effective tariff to the customer to be set at an appropriate level e.g. West Nile. • Tariffs reduced to an affordable level, hence achieves same objective.

Pros and Cons of Different Mechanisms Capex Offset vs Consumption linked delivery mechanisms • Consumption linked subsidy is direct to customers, not to company and is provided only upon delivery to customer. • Consumption linked delivery means that the gross investment cost of the project needs to be financed from “commercial” channels. • Variances in levels of energy consumed compared with projections will inevitably lead to the need for subsequent tariff adjustments (operationally and politically difficult). • Consumption orientated subsidies need to be socially orientated or targeted towards the customers who need it most (i.e. the poorest) and not to all customers.

Use of Carbon Credits • Functions as an effective additional tier of subsidy and/or revenue enhancer. • Possible in both compliance and voluntary markets. • Ensure focus (where possible) on renewable energy.

Pamir Energy – Carbon Credits • Originally incorporated within the Concession Agreement in 2002, so met the “additionality” test. • Originally developed for compliance market as small hydro project, but host country has not yet ratified “Kyoto”. • Strong growth in voluntary market has allowed company to benefit and find counterpart for 2008-2012 delivery.

West Nile - Carbon Credits • One of the early (2002) CDM projects. • World Bank Prototype Carbon Fund – buyer. • Provides valuable (guaranteed) cash flows that can be incorporated into projections => facilitates financing, enhancing returns and achieving financial close.

Small Infrastructure – Way forward • Build on lessons learned in terms of structure and mechanisms. • Apply solutions to non-energy sectors e.g. rural telephony, roads. • Establish a vehicle/structure on a regional basis to enable efficient and accelerated replication of such projects on a “standardised or modular” basis. • Merger of philosophies/skills and closer working practices between donors and non profit agencies as commercial know-how and funding structures are incorporated into projects previously exclusively donor/grant funded.

Conclusions • Success depends on: • patient capital accepting sub-commercial returns • availability of soft / donor money • carbon credits increasingly play a key role • politically receptive host governments • Projects that have historically been funded by state/donors can be financed through introduction of commercial project finance techniques. • With appropriate structure and support, such projects can be sustainable and not a drain on state funds.