Download

1 / 23

230 likes | 387 Vues

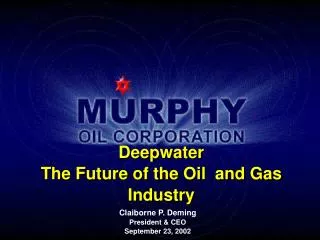

Deepwater The Future of the Oil and Gas Industry. Claiborne P. Deming President & CEO September 23, 2002. Today’s Agenda…. The Demand Story The Supply Challenge The Deepwater’s Role Murphy Oil and the Deepwater. The Stage is Set…. Year 2000. 400. United States .

E N D

Deepwater The Future of the Oil and Gas Industry Claiborne P. Deming President & CEO September 23, 2002

Today’s Agenda… • The Demand Story • The Supply Challenge • The Deepwater’s Role • Murphy Oil and the Deepwater

The Stage is Set…. Year 2000 400 United States Energy Consumption per Capita (Million Btu’s) Australia New Zealand 200 Korea Western Europe /Japan Venezuela Thailand Latin America • China • India 0 $100 $1,000 $10,000 $100,000 GDP per Capita Source: IEA/CIA

Crude Oil Demand will Grow Substantially Crude Oil Demand 100 MBD 90 MBD +1.4 Russia +0.9 Europe +2.3 North America +1.3 M.East 80 MBD +5.4 Asia +0.6 Africa +1.5 South America 70 MBD 60 MBD 1995 1990 2000 2005 2010 Demand is likely unstoppable over the next 20 years Regional Demand Increases (Million BPD 2000 to 2010) Source: PEL/Internal Murphy Analysis

Requiring Tremendous New Production Current Capacity World Crude Capacity 78.8 MBD New Capacity Sources Europe 2.6 Required New Capacity Africa 2.3 S. America/Other 5.3 N. America 5.5 Russia/Caspian 6.6 Other OPEC 7.5 Middle East 16.3 Existing Production after Natural Decline 49.3 2010 World Crude Capacity 95.4 MBD Source: PEL/Internal Murphy Analysis

However, Access to Major Reserves is Limited 676 90 57 21 44 54 Middle East 75 Worldwide Reserves in Billion Barrels Russia/FSU Europe N. America Asia S. America Africa 2000 Total – 1,016 Billion Barrels (Non-OPEC – 214 Billion Barrels) Source: Wood MacKenzie

Middle East – Difficult for Outsiders Projected Capacity Growth of Middle East • Controlled by NOC’s • Marked by War’s, Embargoes, Government Instability • 10% Return Contracts ( when offered) The Middle East will remain world’s largest oil producer and exporter, however it is closed to majority of our industry Source: PEL

Russia/Caspian Region is Growing, but… Russia/Caspian Production Forecast • Investment returns to date are negative • Legal/Contractual System is tenuous • Transport costs can exceed $5.00/Bbl Requires immense capital and regional clout – Only the SuperMajors can operate successfully Source: PEL

North America is Mature North American Production Forecast (Does not include Deepwater) • Most heavily drilled region in the world • Massive capital required just to maintain current production • Remaining high potential areas are off-limits North America will not supply the world’s growing demand Data Source: PEL

Unconventional Sources are not the Answer Full-Cycle Cost Comparison • Reserves are immense (Est. at 3 trillion Barrels) • Full-Cycle costs are high • Processing is energy intensive/produces large quantities of CO2 Source: CERA

The Deepwater Offers a Credible Alternative • Reserves and prospectivity are immense • Full cycle returns are now averaging 20% • Technology is driving development costs downward • Safety/Environmental record is exemplary

Deepwater Reserves are Immense 16.0 5.0 14.0 10.0 60 Billion Barrels Angola Nigeria Brazil Others Total US GOM 2000 Discovered Reserves in Billion Barrels 15.0 Source: Wood Mackenzie

Deepwater Production is Growing Production is set to grow by 4 Million barrels per day by 2008 Source: Wood Mackenzie

Deepwater Technology Continues to Improve • FPSO’s allow production in depths up to 9,000 feet • Sub-sea tiebacks allow profitable development of smaller reservoirs • Deep and extended reach drilling exploit entire reservoir

And is Decreasing Costs Capex/boe Average Field Water Depth • Development costs have decreased by almost 50% since 1990 - even as we go deeper and deeper • Full-Cycle returns now average 20% Source: Wood Mackenzie

Safety Record is Improving • Even though we are producing and drilling more, the actual number of accidents is declining and the incident rate is decreasing rapidly Source: MMS

Oil Spills Have Declined Dramatically • Even with more wells being drilled and more production coming online, the actual spill rate and incident rate are both declining Source: MMS

Future Deepwater Growth Potential Exploration/Growth Potential of Major Deepwater Basins Remaining Exploration Potential Low High • Growing • Nigeria • Gulf of Mexico • Equatorial Guinea • Angola • Emerging • Egypt • Malaysia • Gabon • GOM Ultra-deep • Black Sea/Caspian • Maturing • Congo • Brazil

Current and Projected Deepwater Growth Deepwater Production (Bbl/d) Deepwater Production CAGR 2002-2007 Petrobras 1,100,000 12% Shell 780,000 5% BP 550,000 20% ExxonMobil 220,000 24% ChevronTexaco 150,000 22% TotalFinaElf 100,000 35% ConocoPhillips 25,000 10% Murphy <10,000 35% Source: Deutsche Bank

The Keys to Success in the Deepwater • Build the right skill-set • Encourage and reward exploration • Think globally and move quickly • Exploit niches created NOC’s / SuperMajors

The Deepwater and Murphy – A Perfect Fit MEDUSA Block K HABANERO Block H FRONT RUNNER • Gulf of Mexico Deepwater • 30% success rate • Medusa, Frontrunner are the cornerstones of a growing presence • Production will reach 75,000 bbl/d by 2005 • Deepwater Malaysia • 500 MMbbl potential • Low cost- $6.50/bbl all in • Murphy has 7 Million acres under lease

The Deepwater and Murphy – A Perfect Fit MBOE / D 200 Deepwater GOM Production 150 100 50 0 Jan-98 Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 + Deepwater Malaysia Production

Conclusion • Demand growth is likely unstoppable through 2020 • Most of the remaining reserves are either high-cost or located in unfriendly regions • The deepwater is open and offers tremendous growth and prospectivity • Murphy Oil has the skill-set and vision to become a leader in the Deepwater