Download

1 / 0

0 likes | 117 Vues

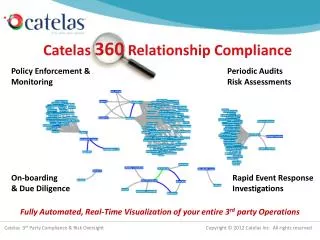

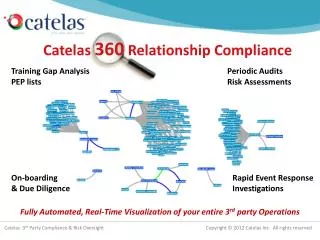

Catelas 360 offers a robust Relationship Compliance Policy Enforcement and Monitoring solution tailored to streamline your compliance processes. Our services include periodic audits and thorough risk assessments to ensure ongoing adherence to regulations. With efficient onboarding and due diligence procedures, as well as rapid event response investigations, we ensure your third-party operations remain compliant. Our fully automated, real-time visualization tool empowers you with complete oversight, enabling proactive management of your compliance risks effectively and efficiently.

E N D