Tax Technology Systems

Tax Technology Systems. The Need For Change. Current Systems …. Inadequate for basic tax functions: Provision system (TIS) is unsupported Compliance system not fully implemented Provision/Compliance reporting systems are not integrated

Tax Technology Systems

E N D

Presentation Transcript

The Need For Change Current Systems … • Inadequate for basic tax functions: • Provision system (TIS) is unsupported • Compliance system not fully implemented • Provision/Compliance reporting systems are not integrated • Poor functionality (FIN48, FIN18, TBBS do not exist in current systems) • Do not support Tax Departments Objectives: • More tax resources allocated to tax planning • Single tax system platform supporting: • Global provision and U.S. compliance integration • Tax planning and tax controversy processes • Visibility of global tax attributes to the home office • Possibility of foreign tax compliance in a future state • Potential for integration of transactional taxes • VAT, Sales & Use, Property • Configuration to allow finance ERP systems (SAP, HFM, and Hyperion Planning) to better support tax

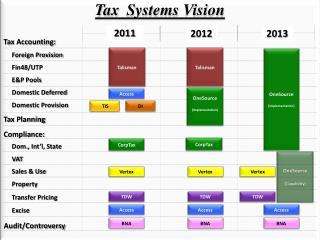

Tax Accounting: Foreign Provision Fin48/UTP E&P Pools Domestic Deferred Domestic Provision Tax Planning Compliance: Dom., Int’l, State VAT Sales & Use Property Transfer Pricing Excise Audit/Controversy Tax Systems Vision – Single Platform 2011 2013 2012 Talisman Talisman OneSource Implementation OneSource Implementation Access TIS DI CorpTax CorpTax OneSource (Capability) Vertex Vertex Vertex TDW TDW TDW Access Access Access BNA BNA BNA

Improve transparency, quality and speed by reforming processes and integrating technology platforms Current situation Potential risks of inaction or delayed action • Key Issues and Challenges • Data and technology gaps exist at each layer of tax calculations which require manual workarounds and take time away from value added work • Manual processes are required to interface data across reporting lines and within reporting functions creating challenges to high quality review • Provision and compliance integration is difficult creating rework and risk of error • Heavy reliance on excel worksheets to support tax calculations results in increase risk of errors, duplication of effort • Significant manual workarounds result in inability to report and communicate real time results • Teams are looking at data a different levels and in different time periods creating increased risk of error • Current manual processes require brute force efforts on a recurring quarterly basis • High cost of developing and maintaining proprietary tools • Progress to improve income tax reporting will be slowed since current technology cannot support desired improvement • Issues will be compounded with continued growth • Continued risk in tax reporting errors, missed deduction, penalties and interest • Challenged in the ability to manage and communicate tax position in real time • Quality suffers due to sub-optimal use of people, process and technology • On-going retention issues and ineffective support Key benefits provided by defined program • Reduced reconciliations through substantial improvement in integration • Cost savings through reductions in manual processes • Significant reduction in income tax reporting cycle time requirements • Higher visibility into tax processes and results at each “layer” increasing awareness of issues and related impacts • Increased accuracy and greater visibility of information through automation • Reduction in low value added manual activities will improve retention • Software maintenance costs decrease by changing to 3rd party “off the shelf” tools

Software Evaluation Process • Conducted including all tax disciplines • Involved evaluation of two leading vendors OneSource Is A Better Fit For Halliburton

How OneSource Supports Tax Direction • Sustained Process Improvements: • Flexible data feeds & adjustment automation enable working with F&A to improve upstream data feeds • Workflow allows us to build standard processes into software, thereby mitigating risk of manual manipulation • Improved functionality means fewer manual workarounds and reformatting of reports to meet custom needs • Single platform enables staff to move between provision & compliance • Improved Data Management: • Enables automation • More flexible data feeds • Higher level of detail available • Less manual process maintenance • Enhanced Reporting Capability: • Uncertain Tax Position Calculations (FIN 48) • Forecasting Functionality (FIN18) • Global Provision – visibility around the world, without manual effort Allows Tax To Focus On Higher Value-Added Activities

Implementation: Ernst & Young • First-hand knowledge of Halliburton’s business and systems • Project Leads are familiar with data warehouse/ODS, SAP, Hyperion, TIS, Talisman and other unique Halliburton tools understanding how each must integrate across tax (gaining efficiencies through minimal time spent “getting up to speed”) • They have worked with Halliburton tax in functions such as provision, compliance, transfer pricing, apportionment and other areas • Global Tax Performance Advisory Team • EY’s Tax Performance Advisory (TPA) team is organized globally and focuses on people, process and technology at large corporate tax departments. • Full time, dedicated TPA resources number above 60 in the U.S. • Approximately 20 in Europe/Middle East/India/Africa (EMEIA) and • Approximately 10 in Asia/Pacific • TPA services in Brazil, Mexico and a Latin America Bus. Center in Miami • Providing objective advice • EY provides objectivity to point out the vision, process and people changes that must occur to reach project goals. Software vendors rarely have the experience outside their tools to provide this type of objective advice.

Implementation: Ernst & Young (cont….) • Tax accounting technical experience • EY has consulted with the CAO and CFO of Halliburton on technical accounting issues and brings both the accounting technical, in addition to the implementation experience needed. • Considering the full picture • EY has extensive experience in teaming with all groups that are critical to these projects to obtain the right input and insights from multiple groups within Halliburton (Accounting, Tax, IT, etc) and other groups (external auditor). • Working with the external auditor • EY standard methodology includes external auditor at key milestones evaluating changes to the controls, testing plan and approach to provision calculations. • Partneringwith software developer • Ernst & Young is formalizing an agreement with ThomsonReuters to achieve global implementer status, meaning teams are trained consistently in the same exacting standards ThomsonReuters requires, not just domestically, but globally. • Ernst & Young is the only service firm with one practice (TPA) that is organized globally. • Ernst & Young will team with ThomsonReuters, as appropriate, to provide best-practice solutions .

Tax Systems Team – Internal Resourcing • Mark Sumlin – Project Lead • Daniel Garcia – Project Manager • Gary Sella – Process Manager • Kevin Shea – Data Manager • Sara Sykes – Domestic Provision/Consolidation • Darrell Simmons – Foreign Provision • Randy Miller – Compliance Lead • Randy Phillips – Federal Compliance • Noman Mogul – International Compliance • Lyle Maddox – State Compliance

Next Steps – Obtain Internal Approvals • Subsequent to approvals… • Coordinate with stakeholders: • Procurement & Legal • Information Technology • Internal Audit • Finance and Accounting • Define Configuration: • Conduct configuration workshop with Ernst & Young and ThomsonReuters • Finalize detailed workplan and roles • Acquire Software/Services • Begin Implementation

Data Management Group June 14, 2011

Team Members • Kevin Shea • Randy Phillips • Benjamin Huang • Elaine Tang • Daniel Garcia • Jim Anderson • Gary Sella • Sita Chowdhury • Nancy Vu • Stacy Hill • Nekeya Evans • Sharon Streiffert • Noman Mogul • Steve Pipkin

How We Serve / Who We Serve • Combine Technology and Function SMEs as a group • Pool the resource and knowledge, Identify data issues and provide efficient solutions • Assisting in areas such as: • Tax Accounting • Streamline data process and support reporting obligations • Tax Planning • Provide financial reporting assistance for IP structuring • Tax Compliance for supporting regulatory obligation • Assist to optimize data, system, and processes • Tax Controversy for audit support substantiation • Reports to collect audit defense R&D • Tax System Implementation • Increase automation on data sources and processes • Assist system Integration

Automate FIT Data Process Purpose: To enhance and increase process efficiency for foreign provision tool - FIT Business Owner: Darrell Simmons Project Lead: Nancy Vu

Research & Development Process Purpose: To provide documentation, organization, and transparency for R&D Business Owner: Janet Wilson Project Lead: Nancy Vu

Financial Reports for IP Analysis Purpose: Provide financial reports to support IP analysis project Business Owner: Mark Sumlin Project Lead: Benjamin Huang

Withholding Tax Validation Purpose: To increase foreign tax credit accuracy from W/H tax receipts Business Owner: Steve Pipkin Project Lead: Benjamin Huang

E & P Process Purpose: To centralize and streamline E & P study and adjustment process Business Owner: Steve Pipkin Project Lead: Elaine Tang

Global Operation Documents Management Purpose: Provide critical documents to support F&A & Tax global operations Business Owner: Mark Purnell/Glenn Little Project Lead: Sharon Streiffert

Business Objects Reports Purpose: Upgrade Business Objects Platform & Migrate Current Inventory of Reports Into the New Environment Business Owner: Randy Miller Project Lead: Daniel Garcia

Indirect Tax Process & Technology • Purpose:Initiate and successfully complete our short and mid term Sales, Use, Excise & Property Tax process & technology opportunities • Business Owner:Kenny McCorquodale Project Lead: Daniel Garcia

Future Data Improvement Focus Areas • Controversy modules • Section 199 Tax Forecast • Pool SME Expertise • Reduced Excel-based manual process • Tax Planning Tracking module • Entity or Stock basis

Tax Accounting Workgroup Process Improvement Initiative June 14, 2011

Tax Accounting Workgroup • Team Members • Gary Sella • Darrell Simmons • Nancy Vu • Rose McNulty-Hurst • Lyle Maddox • Helen Griffiths • Dora Man • Eirik Kindingstad • Mark Sumlin • Randy Miller

Finance Organization Vision and Values • Core Concept • Insight – using our financial expertise to provide Halliburton with the intelligence and flexibility to respond to any opportunity • Quality, Efficiency and Control – consistent delivery of reliable and timely financial information, analysis and properly executed transactions utilizing best-in-class, streamlined processes with a commitment to a strong control environment • Employee Development and Recognition - retaining and attracting the highest-quality finance professionals

Finance Performance Objectives • 2010 & 2011 performance objectives relative to Quality, Efficiency and Control. • Drive Report Standardization – Ensure “one version of the truth” utilizing Hyperion management reporting and implementing a standard project accounting application • Promote Efficiencies – Leverage our applications to reduce manual processing and our business model to maximize output & identify areas for automation and drive reduction in manual processing

Finance Performance Objectives • 2011 performance objectives relative to Insight. • Forecast Accuracy – Monitor and help drive forecast accuracy for both revenue, cost and contribution margins • System and Process Improvements- Plan and implement within budget and timing constraints: • Streamline tax systems

Team Objectives • Promote Efficiencies & Control • Automate routine, recurring manual processes • Decrease time and data manipulation required to compute the global tax provision • Enhance ability to incorporate late accounting entries into the tax provision processes • Expand time devoted to application of internal controls to the reporting process • Utilize standardized processes to insure appropriate application of governing technical guidance • Forecast Accuracy • Increase capability to accurately forecast and monitor effective tax rates globally • Employee Development and Recognition • Empower personnel to engage in more value added planning activities

Obstacles • Systems that are not integrated • Manual processes that are time consuming • Compressed cycle time for reporting requirements • Lack of analytical processes integrated into the calculations • Multiple data sources that require reconciliation • Inability to view global account reconciliations • Timeliness of necessary information from the field • Sufficiency and quality of data required

Targeted Areas of Focus • TIS is outdated (unsupported) and fails to support provision requirements • Cannot generate balance sheet account adjustments • Cannot generate a FIN18 or FIN48 reporting pack • Provision data base (Access) used to compensate for TIS shortfalls gives rise to duplicate maintenance • No OCI or Stock Comp capability • Systems do not fully support SEC auditor requirements • Major processes completed manually with little automation • Existing systems lack flexibility to integrate with ERP systems • TIS only accepts general ledger balances • Poor visibility into near and long-term future • Talisman (month lag) cannot generate the information needed for forecasting • Process for continuous training required • Alignment of tax with the finance organization (data not aligned)

Upstream Solutions • Adoption of HFM as single source of balances for tax provision and compliance purposes • Enhance the Return-to-Accrual process • Automate reconciliations of Pre-tax book income • Provision IBT comes from HFM • Compliance IBT comes from SAP • Increase timeliness of data availability • The Data Warehouse cannot populate the information fast enough to be useful to tax • Integration of Hyperion Planning data directly into provision processes on a real-time basis

Systems Solutions • Obtain system tools compliant with IT and Internal Audit requirements • Use single system platform to house and support global tax provision activities that can be leveraged by compliance, controversy, and planning activities • Thompson Reuters OneSource • Provide for increased system configuration flexibility to capitalize on sub-balance data available from ERP systems • Cost Center • Purchase Order • Document Type, etc… • Provide for increased system reporting flexibility to accommodate cross functional review without manual generation of reports • FIN 18 • FIN 48 • Tax Basis Balance Sheet

Automation of Manual Processes • Support analytical processes with SAP exception-based reports • Use new systems to reduce number of manually prepared PBC schedules • Establish adjustment rules based on sub-balance attributes to accommodate automation of mixed use accounts: • Single reserve accounts containing temporary and permanent transactions (mixed-use accounts) • Contra-balances embedded within asset/liability accounts (foreign currency valuation) • Use systems resources to support local country adjustments from GAAP balances to statutory balances and automate local country tax adjustments

People and Training • Assignment of support responsibility to Tracy Howell to assist F&A field personnel and RTM’s • Completion and rollout of iLearn courses followed by continuous update • Tighter integration with accounting functions to initiate knowledge sharing in areas such as: • Joint venture accounting • Benefits accounting • Fixed asset accounting, etc… • Increase focus on GAAP (ASC 740) technical training for personnel holding tax provision roles

Reporting Quality Assurance • Enhance scope of analytical reviews through efficiencies gained in preparation time at closing • Optimize ETR continuous monitoring • Resolve provision impact of tax issues as they arise, minimizing the work effort at quarter end • Formalize continuous connectivity to finance so as to be aware of real time issues impacting tax • Incorporate use of provision reporting checklists to ensure appropriate inter- and intra-period classification of balances

Priorities and Timeline • Implement upstream data solutions in line with needs of system solution (beginning July, 2011 and ending June, 2012) • Support provision system implementation activities (beginning July, 2011 and ending June, 2012) • Address automation of manual processes (beginning July, 2011 through December, 2012) • Initiate people and training objectives (beginning July, 2011 and ongoing thereafter) • Undertake reporting quality assurance measures commensurate with supporting systems/processes availability (beginning July, 2011 and ongoing thereafter)

COMPLIANCE TEAM June 14, 2011

Team Members • Lisa Brown • Annie Liou • Kenny McCorquodale • Noman Mogul • Linda Perritt • Randy Phillips • Pam Smith • Mike Thacker • Jim Weber • Tanya Weisinger • Rob Wilson

Why Review Compliance Processes? • Reduce Inefficiencies & Redundancies • Drive More Accurate Estimates • Accelerate Close-Outs • Accelerate Return Filing Dates • Maximize Use of Technology • Maximize Use of Skill Sets - Best Use of Personnel

Overall Objective • Optimize Workflows, Resources and Technology

Areas Initially Covered • US Domestic (40 Form 1120’s, 1 Consolidated Return) • US Partnership Reporting (2 1065’s, 12 8865’s) • US-International (155 Form 5471’s, 8858’s, 5713) • US-State / Local Income (432 – Returns, Est. Pmts, Extensions) • Indirect Tax (Sales / Use & VAT) – (3,637 US Filings Annually)

Overview – What Have We Done To-Date • Collaborated w/ Tax Team Members At Large To: • Discuss Issues / Opportunities • Evaluate Corp Tax vs. One Source • Regroup • Address Indirect Tax

Data / Processes / Technology • Common Theme From Discussions: • Data Sources • Fragmented Processes / Systems • Manual Effort

Domestic Income Tax Issues / Opportunities • Forms Automation • International Inclusions / Data • Sub F Income • Section 78 Gross Up • Foreign Tax Credit • Foreign Source Income • Topside Entries • Manual Tax Adjustment (process) Automation • Hedging Contracts • Section 162(m) Limitations • Aircraft Usage • Entertainment Facilities • Dual Consolidated Losses • Section 199 • Hybrid Interest and FX

Domestic Income Tax Issues / Opportunities - Continued • Manual Tax Adjustment (data) Automation • Effect of Account Balance Transfers on Rules • Effect of Accounts w/ Mixed Use Timing Difference on Rules • Effect of Foreign Exchange Reval / Re-measure on Rules • Split Companies • Estimate Automation in Compliance Software • Tax Depreciation • Bonus Depreciation Automation • New Acquisition Tax Books Population • Annualized Tax Depreciation in Period Data • Disclosure Automation

US International Issues / Opportunities • Further Automate Forms 1118, 5471, 8858 and 5713 - Set Up Auto Rules For E&P Adjustments - Automate Foreign Sourcing (Tech Fees, Leasing, Export Sales, etc.) - Streamline 861 Processes (Interest Expense Allocation, G&A, Stewardship, etc.) - Automate Form 5471, Sch M • Create “What-If” Planning Scenarios • Drive Automated Calculations For Estimates • Create Repository for E&P Studies • Enhance Communication in Section 956 Process (Monitor Debt Settlement Timeframe)

US State Issues / Opportunities • Maximize utilization of Compliance Software • Automate Transfer of Data Between Compliance Software and Excel • Calculate State Depreciation

US Partnership Rptg. Issues / Opportunities • Consider the Effect of “Process Changes” for Partnership Rptg. • Effect of Auto Adjustment Rules - Partnership Capital Account • Mapping for 1120 may vary from Mapping for 1065 / 8865 • Create Separate “Capital Accounts” for Partnership Rptg. • Partnership Capital Account • Contributions • Distributions • Reconciliation of Inter-company Loans • Currently Netted • Need True Accounting of Total Liabilities • Mapping Opportunities to Achieve Single Source of GL Data. • Automate Process – Foreign Source Income / Deductions • Automate Process – Intercompany transactions