Ceylon Graphite Running the numbers

80 likes | 128 Vues

Ceylon Graphite Running the numbers

Ceylon Graphite Running the numbers

E N D

Presentation Transcript

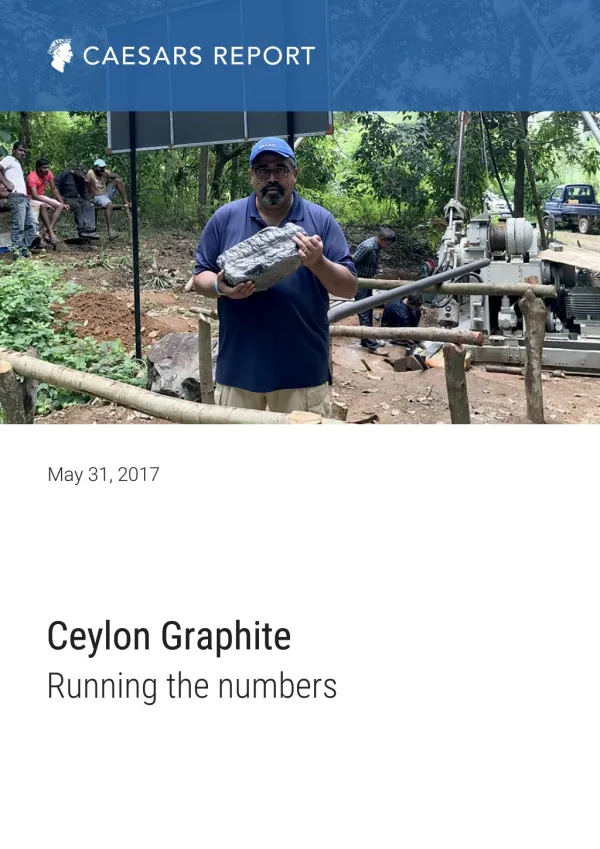

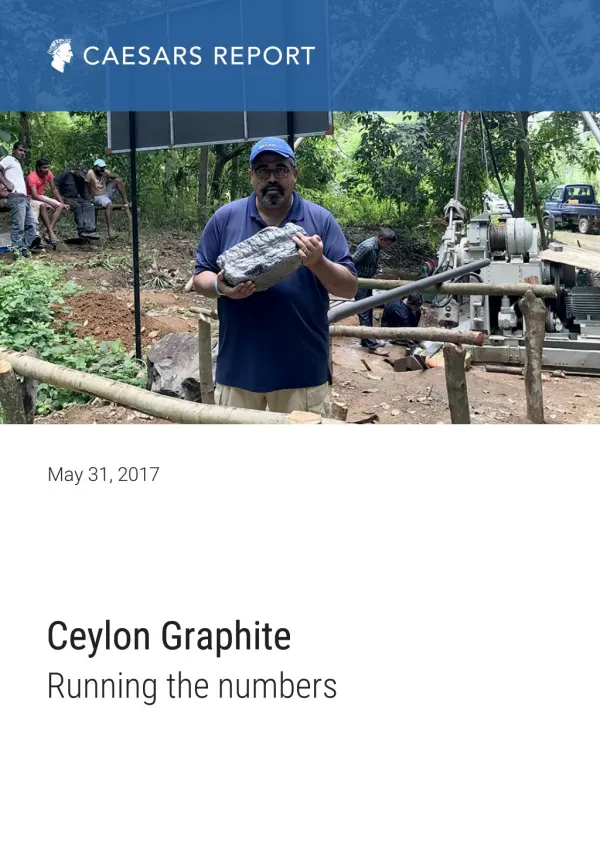

May 31, 2017 Ceylon Graphite Ceylon Graphite Running the numbers

Commodity Graphite Price C$ 0.230 0.500 0.450 Countries Active Sri Lanka Ticker TSXV CYL OTC NWNYF FRA CCY 0.400 Working Capital C$ 2.8M (est.) 0.350 52 week high C$ 0.450 Shares 54.3M 0.300 52 week low C$ 0.165 Market Cap C$ 12.5M 0.250 0.200 www.ceylongraphite.com 0.150 Early Exploration Advanced Exploration Feasibility Financing Development Production Sri Lankan Graphite Project Ceylon Graphite (CYL.V) has kicked off its exploration program in Sri Lanka, where the company is aiming to discover new high purity graphite veins. In this update report we will discuss the company’s exploration plans, and we will try to figure out the economics of a graphite mining operation in the country. A brief recap about graphite in Sri Lanka and Jacob Capital Management’s history Sri Lanka used to be one of the main countries where graphite was sourced from, and the country established a good name on the world market thanks to the high purity of its graphite product. Sri Lanka has been producing and exporting graphite since the second half of the seventeenth century, and thanks to the excellent quality of the export product, the Sri Lanka graphite accounted for approximately 50% of the total world volumes in the first decade of the 1900’s. But things went downhill fast and right now, Sri Lanka only accounts for just 1% of the total volume of graphite on the world markets. This doesn’t mean there’s no more graphite left in the soil, not at all, and the reduced graphite production seems to be caused by a wide array of circumstances. Pretty much the entire island was ‘up for grabs’, and thanks to the excellent long- term relationship of Sasha Jacob (Jacob Capital Management) with the local

business community and lawmakers, Ceylon was able to get its hands on 116 grids, which each consist of one square kilometer. It all boiled down to having personal relationships, and Jacob was the co-founder of what now is the largest hydropower company in the country, which was sold last year. Having in excess of a decade of experience in Sri Lanka is what really has allowed Sasha Jacob and Jacob Capital Management to stand out from the crowd as these 116 grids comprise the majority of the past-producing graphite mines in the country. The excellent relationship was recently highlighted when John Tory, the mayor of Toronto, visited Ceylon Graphite’s operations in Sri Lanka together with Sasha Jacob from JCM. Ceylon Graphite hosted Toronto’s Mayor along with several Canadian Representatives tocelebrate the commencement of mining operations.

The exploration activities havestarted! Ceylon Graphite has started to drill the K1 zone, which hosted a past producing graphite mine. Exactly because this target was a past-producing mine, Ceylon wanted to prioritize this zone for its first-ever drill program in Sri Lanka as recent ground mapping has confirmed the prospectivity of this area. Ceylon Graphite will drill right around the old mine shaft, and will then move out to continue to test the underground structures up to 300 meters below surface. By putting in some very deep holes, Ceylon Graphite intends to identify and test several graphite veins to see how the veins will relate to each other and perhaps already start to think about putting a first mine plan together. Drilling at the K1 zone is just the start, and Ceylon Graphite plans to drill all 116 grids (which each are one square kilometer) in the next 24 months. This seems to be an aggressive point of view and as the ability to drill off 116 square kilometers is usually directly related to a company’s cash position and access to capital, we do expect Ceylon’s drill cost per meter to be fairly low, considering the company has acquired its own drill rig. Green squares indicate Adits and their direction. Triangles indicate shafts

High-purity material and low-cost labor should result in superioreconomics Ceylon Graphite doesn’t have a resource or a PEA on its 116 km² land package, but the company has provided a basic overview of the economics of a graphite mining operation. These numbers weren’t pulled out of thin air but are based on similar operations in Sri Lanka. The ‘pure’ production cost of a tonne of graphite (on a mine gate basis) is expected to be $175/t, and this number has been confirmed by comparing it to the Kahatagaha (‘Kaha’ for simplicity sake) graphite mine in Sri Lanka, located approximately 30 kilometers to the northeast of Kurunegala (in the middle of the island). Not only does this mine provide a good impression of how the production costs could be estimated, the Kaha mine also shows the potential long mine life of these graphite vein mines. Production at Kaha started approximately 150 years ago, and the total cumulative graphite production up until now is in excess of 300,000 tonnes of graphite, with a current production rate of just a few hundred tonnes per year. The mine is currently government-owned, and we wouldn’t be surprised if the main priority would be to create jobs rather than maximizing profits.

On top of the $175/t, Ceylon Graphite thinks it will need an additional $100/t for refining, which would bring the total production cost to $300/t (rounded). This indicates that if the company is indeed correct in its assumption to be in a position to sell its graphite at an average price of $1250/t, the operating margin would be very healthy, at $950/t. That being said, we’d still have to deduct the government royalties which are based on the revenue. This will reduce the operating margin to approximately $850/t (again, rounded down to err on the cautious side). To make your life easier, we have borrowed a table from the corporate presentation of Northern Graphite (NGC.V), to show you how Ceylon’s expected economics compare to the other players in the graphite space. Comparison to the other players in the graphite space Note, the data was sourced from publicly available information based on the official technical reports from those companies, and the production costs and sales prices might have changed since. We are also not discussing the veracity of the claims of the companies in the table, and keep in mind some of these operating margins will be based on outdated graphite prices, whereas Ceylon’s operating margin and sales price are based up-to-date market prices. Assuming a production rate of 150 tonnes per month, each vein will product at a rate of 1,800 tonnes per year. This means that – based on the public estimates – each vein will generate approximately $1.4M in annual operating cash flow (excluding sustaining capex), resulting in a payback period of less than six months per new vein (considering the initial capex to start the graphite production at a vein is estimated to be just $300,000 (the $3M mentioned in the presentation includes the initial capex for the first 10 veins). And with a capital intensity of less than $200 dollar in initial capex per tonne of annual production, Ceylon Graphite is leading the pack.

And there’s one really important additional feature: Ceylon Graphite has been granted a tax holiday by the government of Sri Lanka which means its operating margin also is its post-tax operating margin. That’s huge as it will allow the company to immediately re-deploy its entire cash flow to boost its production rate. These numbers should give you an idea of what you could expect, but keep in mind Ceylon Graphite’s project doesn’t have a NI43-101 compliant resource estimate, and that’s why this year’s drill program is so important. Conclusion Ceylon Graphite has started drilling on its tenements in Sri Lanka and will try to create shareholder value through the drill bit. The first drill location is a very interesting one as it will allow Ceylon to ‘chase’ known veins which have been mined before. Ceylon Graphite is the result of Jacob Capital Management’s involvement in Sri Lanka since 2004, and this gives the company a competitive advantage none of the other graphite hopefuls have.

For enquiries, please post a comment on the article online, contact us at caesarsreport.com/contact or email us at info@caesarsreport.com About Caesars Report Caesars Report is an online mining portal specialized in (junior) mining companies. In the coming years securing resources will be fundamental to sustaining growth so this will remain a key area of investor interest. We provide coverage of companies that offer an attractive risk/reward ratio. Our aim is to inform our readers and to give them an incentive to do further research. We visit interesting companies ourselves and report from the source. We are also present on numerous events all over the world, ranging from the PDAC International Convention in Toronto to smaller roadshows all over Europe. As we are not a registered investment advisor, please always do your own research. Visit us at www.caesarsreport.com Disclaimer Please read our full disclaimer at caesarsreport.com/discl The CaesarsReport.com employees are not Registered as an Investment Advisor in any jurisdiction whatsoever. CaesarsReport.com employees are not analysts and in no way making any projections or target prices. Neither the information presented nor any statementor expression of opinion, or any other matter herein, directly or indirectly constitutes a representation by the publisher nor a solicitation of the purchase or sale of any securities. The information contained herein is based on sources which we believe to be reliable but is not guaranteed by us as being accurate and does not purport to be a complete statement or summary of the available data. The owner, publisher, editor and their associates are not responsible for errors and omissions. They may from time to time have a position in the securities mentioned herein and may increase or decrease. The author owns a long position in Ceylon Graphite, and the company is a sponsor of the website. All images in this document are copyrighted by the concerning companies. The company data was fetched from the according stock exchange of the company or company presentations. Still, the owner, publisher, editor and their associates are not responsible for errors and omissions concerning this data. The Caesars Report logo, and the whole of this document is copyrighted by caesarsreport.com. This document is distributed free of charge, and may in no circumstances be sold, reproduced, retransmitted or distributed, without written consent from caesarsreport.com.