Download

1 / 37

370 likes | 568 Vues

Home Finance Programs for First Time Buyers. Group Members Bob Kruse Sheila Kerins Kristen Kenkel Ryan Seifert. Are you Ready? 5 Questions. Do I have a steady source of income? Have I been employed on a regular basis for the last 2-3 years? Is my current income reliable?

E N D

Home Finance Programs for First Time Buyers Group Members Bob Kruse Sheila Kerins Kristen Kenkel Ryan Seifert

Are you Ready? 5 Questions • Do I have a steady source of income? Have I been employed on a regular basis for the last 2-3 years? Is my current income reliable? • Do I have a good record of paying my bills? • Do I have few outstanding long-term debts, like car payments?

Do I have money saved for a down payment? • Do I have the ability to pay a mortgage every month, plus additional cost? • If you answer “Yes” to these questions, you are probably ready to buy or own a home.

Fixed Rate Mortgage 15-YR Fixed 30-YR Fixed Adjustable Rate Mortgages Balloon Two-Step ARMS Types of Loans

Fixed Rate Mortgages • These types have payments that remain the same for the life of the loan • Advantages: • Predictable • Housing cost remain unaffected by interest rate changes and inflation

Why choose 15 or 30 YR Fixed? • 15 YR • Loan usually made at a lower interest rate • Equity is built faster because early payments pay more principal • 30 YR • In the first 23 years of the loan, more interest is paid off than principal meaning larger tax deductions • As inflation and cost of living increase, mortgage payments become smaller part of overall expenses.

Adjustable Rate Mortgage • These types have payment increases or decreases on schedule with changes in interest rates; the increases/decreases subject to limits • Advantages: • Generally offer lower initial interest rates • Monthly payments can be lower • May allow borrower to qualify for a larger loan amount

Why choose an ARM? • An ARM may make sense if : • You are confident that your income will increase steadily over the years • You anticipate a move in the near future and are concerned about potential increases in interest rates.

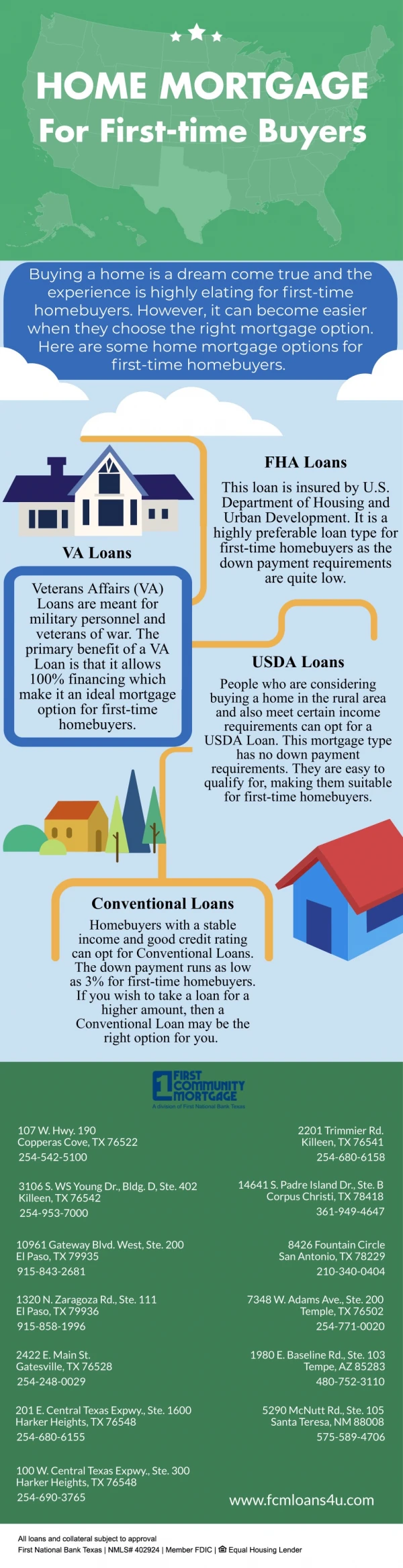

Are there special programs for First-Time Homebuyers? • Yes. Lenders now offer several affordable mortgage options which can help first time homebuyers overcome obstacles that made purchasing a home difficult in the past. Lenders may now be able to help borrowers who don’t have a lot of money save for the down payment and closing cost, have no or poor credit history, have quite a bit of long term debt, or have experienced income irregularities.

HUD • HUD is the U.S. Department of Housing and Urban Development • Established in 1965 • Mission is to create a suitable environment for all Americans by developing and improving the country’s communities and enforcing fair housing laws

How does HUD help? • HUD helps people by administering a variety of programs that develop and support affordable housing. • HUD plays a large role in homeownership by making loans available for lower- and moderate-income families through its FHA mortgage insurance program and its HUD Homes program. • HUD owns homes in many communities throughout the U.S. and offers them for sale at attractive prices and economical terms.

What is FHA? • An agency within HUD, the Federal Housing Administration • Established in 1934 to advance opportunities for Americans to own homes. • FHA gives Lenders the security they need to lend to first-time buyers who might not be able to qualify for conventional loans. • FHA has helped more than 26 million Americans buy a home. • Their website: • http://www.fha.com

How does FHA assist in Home Buying? • The FHA works to make homeownership a possibility for more Americans. • With the FHA, you don't need perfect credit or a high-paying job to qualify for a loan. • The FHA also makes loans more accessible by requiring smaller down payments than conventional loans. • FHA down payment could be as little as a few months rent. And your monthly payments may not be much more than rent.

How is FHA funded?Who Qualifies? • Lender claims paid by the FHA mortgage insurance program are drawn from the Mutual Mortgage Insurance fund. This fund is made up of premiums paid by FHA-insured loan borrowers. No tax dollars are used to fund the program. • Anyone who: • meets the credit requirements • can afford the mortgage payments and cash investment • plans to use the mortgaged property as a primary residence

FHA Products • 81% of FHA-insured loans went to first-time homebuyers during 2000 • They have • 6 different loan types • Fixed Rate Mortgages, Adjustable Rate Mortgages, Graduated Payment Mortgages, Growing Equity Mortgages, Energy Efficient Mortgages, and Mortgages for Condominium Units • 7 different special programs • Nehemiah, HART, AmeriDream, Partners in Charity, Consumer Debt Solutions, Inc., Officer Next Door, and Teacher Next Door

Fixed Rate Mortgages • Fixed Rate loans are the "vanilla" of the mortgage market. • Fixed Rate is your benchmark for any creative financing package, and by far, the mortgage industry leader. • Fixed rate products with the options of 15, 20, 25, or 30 year terms. • The interest remains fixed for the life of the loan. • Loans are not assumable and may or may not contain a pre-payment penalty.

Adjustable Rate Mortgages • Adjustable rate products with options of 10 / 1- year, 7 / 1-year, 5 / 1-year, 3 /1 -year, and 1-year. • The ARM is tied to an index based on either a weekly average yield on United States treasuries adjusted to a constant maturity of one year and published weekly • The interest rate and payment will adjust annually after the initial fixed period of 1, 3 , 5 or 10 years. • Best for: First-time homeowners looking to move up, yet unsure of how long they'll stay in their new home

Graduated Payment Mortgages • This program helps first-time buyers and others with limited income who expect their income to rise in the next 5-10 years, but may not yet be able to handle all of the upfront and monthly costs involved in homebuying. • It helps them tailor their mortgage payments to their expanding incomes and buy a home sooner than they could with regular financing. • The down payment is 3% or less of the sales price

Growing Equity Mortgages • Similar to the Graduated Payments • Enables a household with a limited income that is expected to rise to buy a home sooner by making mortgage payments that start small and increase gradually over time. • The increased payments are applied to reduce the principal owed on the mortgage and thus shorten the mortgage term. • This reduced term and the faster repayment of principal makes GEMs more attractive to lenders and investors than other fixed-rate investments. • Not used often and considered obsolete

Energy Efficient Mortgages • Helps first time homebuyers save money on utility bills by enabling them to finance the cost of adding energy-efficient features to home mortgage • Helps to achieve national energy efficient goals and reduce pollution • Little understood and marketed program

Mortgages for Condominium Units • This program insures the loan for a person who purchases a unit in a condominium building • Must contain 4 dwelling units • Limits set on the size of the mortgage loan that vary with location and the number of units being purchased

Nehemiah • Private California Non-Profit Organization that offers down payment assistance programs to qualified homebuyers • Gift money of 1% to 6% of the contract sales price or a flat Gift amount (not to exceed 6% of the contract sales price) towards down payment and closing costs • Free money for both first time and repeat homebuyers • Free money for both new and resale homes • No repayment of gift money • No income or asset limit • No geographical restrictions • Their website • http://www.getdownpayment.com/

HART Program • The Housing Action Resource Trust (HART) program is a Non-profit Housing and community development corporation that promotes home ownership by offering down payment assistance programs to qualified low and moderate income homebuyers • HART will gift up to $15,000 of the final sales price on a home • Can use the gift money on: • Down Payment • Closing Costs (recurring and non-recurring) • Pre-paids • Rate buy-downs • Their website • http://www.hartprogram.com/

AmeriDream Charity Program • To expand affordable housing opportunities for underserved groups and promote the value of homeownership as the foundation for building strong communities and individual prosperity. • Gift up to 5% of the purchase price of a home for a down payment or closing costs. • This gift does not have to be repaid. • The seller pays a 2 percent service fee to AmeriDream. • Their Website • http://www.ameridream.org/

Partners in Charity Program • Non-Profit organization that will gift 2%-10% depending on needs • PIC provides a down payment with no repayment and no second mortgage or lien of any type • Their website • http://www.partnersincharity.org/index.html

Consumer Debt Solutions, Inc • Called CDS, it’s a non-profit corporation that promotes homeownership by offering down payment assistance programs to qualified low and moderate income homebuyers • Will gift up to $10,000 of the final sales price on a home • Can be applied to the down payment and/or closing costs • Condominiums, townhouses, modular homes, and multi-family owner occupied properties (up to four units) may all be purchased under the program as well. • Their website • http://www.cdsgrants.com/

Offers single-family houses, townhouses and condominiums for sale to officers at a 50% discount. Reduces down payment to $100 (typically down payments are 3% total home worth) The goal is to encourage Officers to buy homes in low and moderate-income neighborhoods Their Website http://www.fhalibrary.com/other_fha_issues/officer_next_door/default.asp Offers teachers a 50% discount on a HUD owned single family homes in certain designated revitalization areas Reduces down payment to $100 (typically down payments are 3% total home worth) The goal is to encourage teachers to buy homes in low and moderate-income neighborhoods. Their website http://www.fhalibrary.com/other_fha_issues/teacher_next_door/default.asp Officer and Teacher Next Door Programs

Fannie Mae • Work with Lenders to make sure they don’t run out of mortgage funds • Second largest corporation in terms of assets

Fannie Mae • The Nations largest source of financing for home mortgages. • 4,700 employees • 1938 The Federal government established Fannie Mae to expand the flow of mortgage money by creating a secondary market

Fannie Mae • Fannie Mae was authorized to by Federal Housing Administration insured mortgages thereby replenishing the supply of lendable money. • In 1968 they became of private company • Work under a congressional charter that directs them to channel their efforts towards increasing

Fannie Mae • The availability and affordability of homeownership for low, moderate, and middle income Americans • Receive no government funding or backing

Loan Limits for Fannie Mae • One Family Loans: $322,700 • Two Family Loans: $413,100 • Three Family Loans: $ 499,300 • Four Family Loans: $620,500

Freddie Mac • Shareholder owned corporation • Employs 3,900 people • Operates in residential mortgages backed by the equity of millions of American homes across the nation • Has financed homeownership for more than 30 million families since 1970 • In the Secondary Mortgage Market

Freddie Mac • Highest Mortgage Rate of 18.63% in 1981 • Lowest Mortgage Rate of 5.21% in 2003 • Created by Congress in 1970 • Created to create a continuous flow of funds to mortgage lenders in support of home ownership and rental housing

Freddie Mac • How Freddie Mac works for the Secondary Market • Prospective homebuyer applies for a mortgage loan through a mortgage lender, broker, credit union, or on-line. Automated underwriting systems like Loan Prospector can evaluate a prospective homebuyer’s credit, collateral, and capacity to repay the loan. Then respond in minutes.

Freddie Mac • A mortgage lender then packages the loans it has made and sells those packages to the secondary market (Freddie Mac). The lender uses the proceeds from the sale to make new loans to other prospective homebuyers.

Freddie Mac • Freddie Mac then sells notes backed by the mortgage loan it has purchased to securities investors. It uses the funds from the security sales to purchase more mortgage loans from lenders across the country