Uploaded by

sharla

0 SLIDES

157 VUES

0LIKES

Risk and Leverage

DESCRIPTION

Risk and Leverage. John E. Parsons March 22 , 2014 Financing Energy Investments Université Paris Dauphine. Setting Aside Taxes. So you want higher returns? Example of Macbeth Spot Removers. expected outcome. Leverage magnifies expected return on equity.

Download

1 / 0

Télécharger la présentation

Risk and Leverage

An Image/Link below is provided (as is) to download presentation

Download Policy: Content on the Website is provided to you AS IS for your information and personal use and may not be sold / licensed / shared on other websites without getting consent from its author.

Content is provided to you AS IS for your information and personal use only.

Download presentation by click this link.

While downloading, if for some reason you are not able to download a presentation, the publisher may have deleted the file from their server.

During download, if you can't get a presentation, the file might be deleted by the publisher.

E N D

Presentation Transcript

-

Risk and Leverage

John E. Parsons March 22, 2014 Financing Energy Investments Université Paris Dauphine -

Setting Aside Taxes

- So you want higher returns?Example of Macbeth Spot Removers expected outcome

- Leverage magnifies expected return on equity

- The Catch:Leverage also magnifies risk

- Expected Returns on Equity is Derived, Not Given 100% equity financed: 50% debt financed:

- Risk in Equity is Derived, Not Given 100% equity financed: 50% debt financed:

- Leverage and Rates of Return What happens: Asset return is given. Debt rate is given. Equity rate is derived. Different debt/equity ratios imply different equity rates.

- The Wrong Way to Think About It Our earlier return equation can be rewritten as: It’s the same set of relationships, but it invites a mistaken interpretation: The variables on the right hand side are fixed and given The variable on the left-hand-side is derived.

- The Wrong Way to Think About It r rE rA rD D V

- Leverage and Rates of Return What happens: Asset return is given. Debt rate is given. Equity rate is derived. Different debt/equity ratios imply different equity rates. What we observe: Debt rates, equity rates and a debt/equity ratio… we back out an implied asset rate.

- Leverage and Rates of Return What happens: Asset return is given. Debt rate is given. Equity rate is derived. Different debt/equity ratios imply different equity rates. What we observe: Debt rates, equity rates and a debt/equity ratio… we back out an implied asset rate. Mistake we make: (1) Fix the debt and equity rates, then change the leverage ratio.

- Leverage and Rates of Return What happens: Asset return is given. Debt rate is given. Equity rate is derived. Different debt/equity ratios imply different equity rates. What we observe: Debt rates, equity rates and a debt/equity ratio… we back out an implied asset rate. Mistake we make: (1) Fix the debt and equity rates, then change the leverage ratio. Mistake we make: (2) Use book values for the debt/equity ratio.

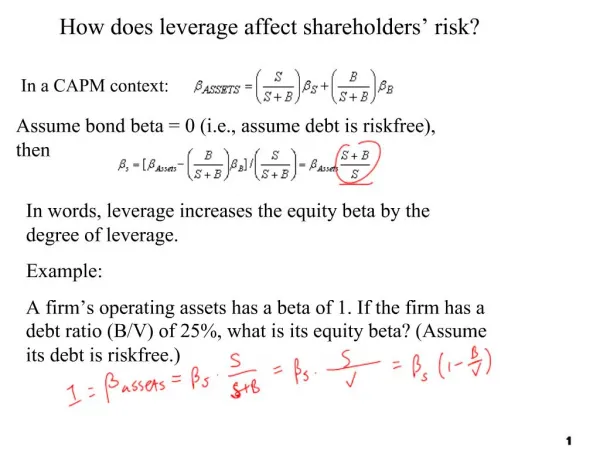

- Higher Measured Equity Beta May Reflect Either:Higher Asset Beta or More Leverage

- Inferring the Asset Beta from information on the Debt and Equity Betas

- Inferring the Asset Beta from information on the Debt and Equity Betas

- Asset Beta Results for US Electric Utilities

- Asset Beta Results for US Electric Utilities

- How Does Leverage Affect Value? The return on assets is not changed. This is the fundamental, underlying source of value. The law of the conservation of value. Equity return and risk increase together. The extra return on equity matches the extra risk. The two move along the Security Market Line, but not above it. The per unit value of equity does not change. The MM Theorems

- Value Additivity V#1 + V#2 + V#3 = VA = VL = VD + VE

- Conservation of Expected Return

- Conservation of Risk (Beta Risk)

- Beta Accounts

- Do It Yourself Finance When a corporation levers itself, it is splitting up the firm’s asset returns into two packages. Debt gets a low risk, low return stream of payments. Equity gets the residual, higher risk, higher return stream of payments. What can investors do for themselves? Let’s start from the unlevered firm, with no debt. Purchase some unlevered equity, on margin, i.e., by borrowing money. Our total return has two parts: The unlevered equity risk and return. The payment of a low risk, low return amount on the debt. Our total return becomes higher risk, higher return. The company’s decision to “lever up” produces an equity risk & return package that an investor could get for itself without assistance from the company.

- Do It Yourself Finance, Version 2 What can investors do for themselves? Let’s start from the levered firm, with debt. Purchase some levered equity, but also lend some money. Our total return has two parts: The levered equity risk and return. The low risk, low return amount earned on the debt. Our total return becomes lower risk, lower return. The company’s decision to “lever up” produces an equity risk & return package that an investor can undo to get itself back to the same risk-return package as the unlevered firm.

- What is the Role of the Firm’s Financing Decision? It repackages the risk-return stream flowing from the assets. But investors can do the same thing themselves. So the value of the total stream flowing from the assets is unchanged by how the company packages it. Hmmmmm?

-

Now Bringing Taxes Into the Account

- Taxes and Value Debt is often tax privileged. The same earnings from assets are taxed less at the corporate level when distributed to investors as payouts on debt than when distributed to investors as payouts on equity. So, … While the pre-tax return on assets is fixed, independent of the company’s capital structure, The post-corporate-tax return on assets is not fixed. More debt means more return, post tax, for the same total risk. Issuing debt can increase the after-corporate-tax return to investors. The levered value of the firm equals the unlevered value, plus the tax benefits of debt.

- Alternative Cash Flow Valuation Methods Equity Cash Flow method Equity after-tax cash flow. Tax shield from debt explicitly adds to the equity cash flows. Apply the equity discount rate, Re. Adjusted Present Value method Project unlevered after-tax cash flow. Ignore the tax shielf from debt. Apply the asset discount rate, Ra. Separately calculate the value of the debt tax shield. Add the value of the unlevered project and the value of the tax shield. WACC Project unlevered after-tax cash flow. No accounting for debt in the cash flows. Apparent tax burden is too large. Apply the Weighted Average Cost of Capital. WACC = Re (E/V) + Rd (D/V) (1-t) The value of the debt tax shields are embedded in setting the discount rate lower by the (1-t) factor.

- Alternative Cash Flow Valuation Methods (cont.) Ideally, All 3 Methods Give the Same Result. The ideal assumptions require that The debt profile through time is the same for all three. WACC assumes a constant debt/equity ratio in market value terms. The other 2 methods usually fix a debt schedule in nominal terms, and the market value of equity is derived, so that the market value ratio may not match what was assumed for the WACC. In reality, debt profiles are seldom fixed, but adjust to contingencies, albeit with frictions. The equity discount rate is consistent with the project discount rate is consistent with the WACC. Since the market value debt/equity ratio is changing through time, the equity discount rate is changing, and it is difficult to assure the value chosen is correct.

-

Beyond Taxes…

- A More Comprehensive View r rE WACC rD D V

-

The End

More Related