Lesson 3 INCOME STATEMENTS

Lesson 3 INCOME STATEMENTS. Li, Jialong 2011-2-26. Income Statement. The Income Statement (Profit and Loss). This formal report shows the income, cost of goods sold, gross profit, expenses by category and net profit for a particular period of time.

Lesson 3 INCOME STATEMENTS

E N D

Presentation Transcript

Lesson 3 INCOME STATEMENTS Li, Jialong 2011-2-26

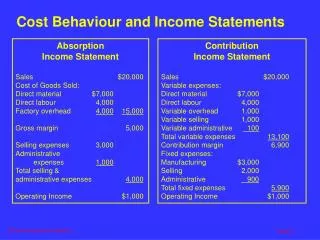

The Income Statement (Profit and Loss) • This formal report shows the income, cost of goods sold, gross profit, expenses by category and net profit for a particular period of time. • The Income Statement categorises income and expenses to present them in a meaningful manner to help with the analysis and control of the business. It has been referred to as the Trading Statement or Profit and Loss Statement.

The Income Statement (Profit and Loss) • GROSS PROFIT is the difference between sales revenue and the cost of the goods sold. • NET PROFIT/LOSS is the Total Revenue less all the expenses. • COST OF GOODS SOLD : The inventory the business starts with plus what it buys gives it the total inventory it could sell during the year. At the end of the financial year the business does a stocktake and finds out exactly what inventory it has at the end and the difference between the total available for sale and the stock on hand at the end must be the amount of stock sold throughout the year. This method is called Periodic Stock method and is used for small businesses.

Formula for Cost of Goods Sold • Inventory at the start of the period • +Purchases • + Freight inwards • + Other inventory costs e.g. wharfage, handling costs, customs duty • Less - (Inventory at the end) • = Cost of Goods Sold

EXPENSE CATEGORIES • Selling and Distribution This is sometimes called Marketing Expenses. These expenses relate to the selling of the goods of the business such as sales salaries and include the costs of delivering, sending, despatching or distributing goods to the customers. • General and Administrative These are general costs incurred in the running of the business. Expenses that do not fit into another category live here. Examples of general expenses are electricity and office salaries. • Financial and Borrowing These expenses relate specifically to the costs of obtaining or borrowing the supply of money to the business e.g. interest paid, discount allowed to customers for early payment of accounts and bad debts.

Review Questions • Definition and format of an Income Statement • Cost of Goods Sold -definition and formula • Expenses – Classification • Completing an Income Statement

Exercises • Exercises 3.1, 3.2 • Exercises 3.3---3.5 • Exercises 3.6---3.8 • For extra homework 3.9,3.10

Reading and Resources • Student Notes and Readings Lesson 3